FinancialNEXON Co.

Consolidated Financial Results for the Fiscal Year Ended December 31, 2025 [IFRS]

1 Feb 202632 pages~61 min full read

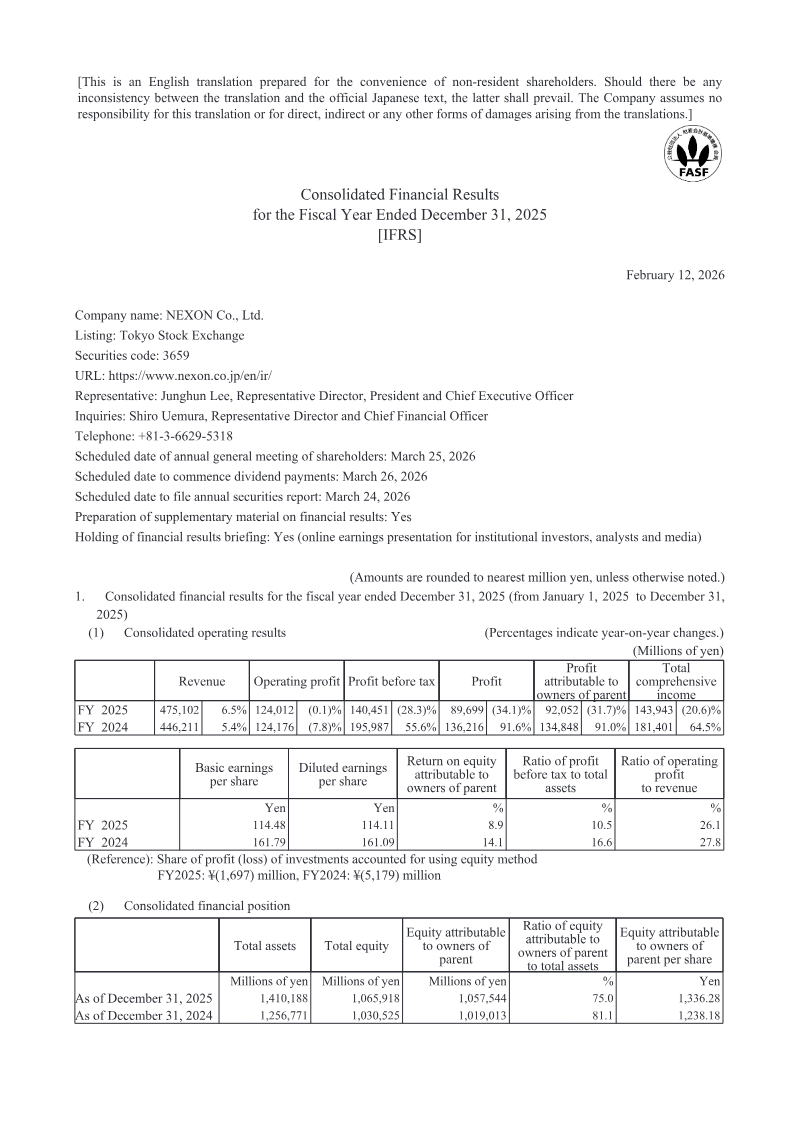

Nexon achieved record-breaking consolidated revenue of ¥475.1 billion for the fiscal year ended December 31, 2025, a 6.5% year-on-year increase driven by the Korea segment and PC online titles like Dungeon&Fighter and MapleStory.

See it on page 27Profit attributable to owners declined 31.7% to ¥92.1 billion, impacted by foreign exchange losses, higher marketing and royalty expenses, and an ¥8.6 billion impairment loss on equity method investments.

See it on page 19Nexon projects aggressive Q1 2026 growth, forecasting revenue between ¥139.7 billion and ¥164.0 billion, representing a 32.1% to 44.0% year-on-year increase.

See it on page 10The company significantly increased shareholder returns by doubling the annual dividend to ¥45.00 per share and approving the cancellation of 36.5 million treasury shares following ¥96.9 billion in share repurchases.

See it on page 21The financial position remains robust with ¥498.9 billion in cash reserves and total assets of ¥1.41 trillion, supported by a significant rise in net cash from operating activities to ¥171.9 billion.

See it on page 8Future growth strategy focuses on leveraging the free-to-play microtransaction model across PC and mobile platforms to expand market share in North America and Europe, supported by new releases like Mabinogi Mobile.

See it on page 14Nexon Group achieved record-breaking consolidated revenue of ¥475.1 billion for the fiscal year ended December 31, 2025, representing a 6.5% year-on-year increase. This growth was primarily driven by the Korea segment, which contributed ¥400.7 billion, and a robust performance in the PC online market. Key intellectual properties, including Dungeon&Fighter and MapleStory, alongside the successful launch of ARC Raiders, underpinned this expansion. Despite the revenue gains, profit attributable to owners fell 31.7% to ¥92.1 billion. This decline was largely influenced by foreign exchange losses, increased marketing and royalty expenses, and an ¥8.6 billion impairment loss on equity method investments.

The financial position remains strong, characterized by a cash reserve of ¥498.9 billion and total assets reaching ¥1.41 trillion. Net cash from operating activities rose significantly to ¥171.9 billion, while investing activities turned positive due to ¥197.6 billion in proceeds from the sale and redemption of securities. To enhance shareholder value and capital efficiency, the annual dividend was doubled to ¥45.00 per share, and the board approved the cancellation of approximately 36.5 million treasury shares. These actions followed a substantial ¥96.9 billion allocation toward treasury share purchases during the fiscal year.

Looking forward to the first quarter of 2026, revenue is projected to grow between 32.1% and 44.0% year-on-year, reaching up to ¥164.0 billion. This optimistic outlook is supported by the continued momentum of the MapleStory franchise and the integration of recent releases like Mabinogi Mobile. While the Dungeon&Fighter franchise may face a temporary revenue decline, the overall trajectory suggests a pivot toward aggressive growth. The company continues to leverage its free-to-play microtransaction model across PC and mobile platforms to maintain its dominant market position in Korea and expand its footprint in North American and European markets.