FinancialCyberAgent

FY2025 Consolidated Financial Results [Japanese GAAP]

1 Nov 202519 pages~34 min full read

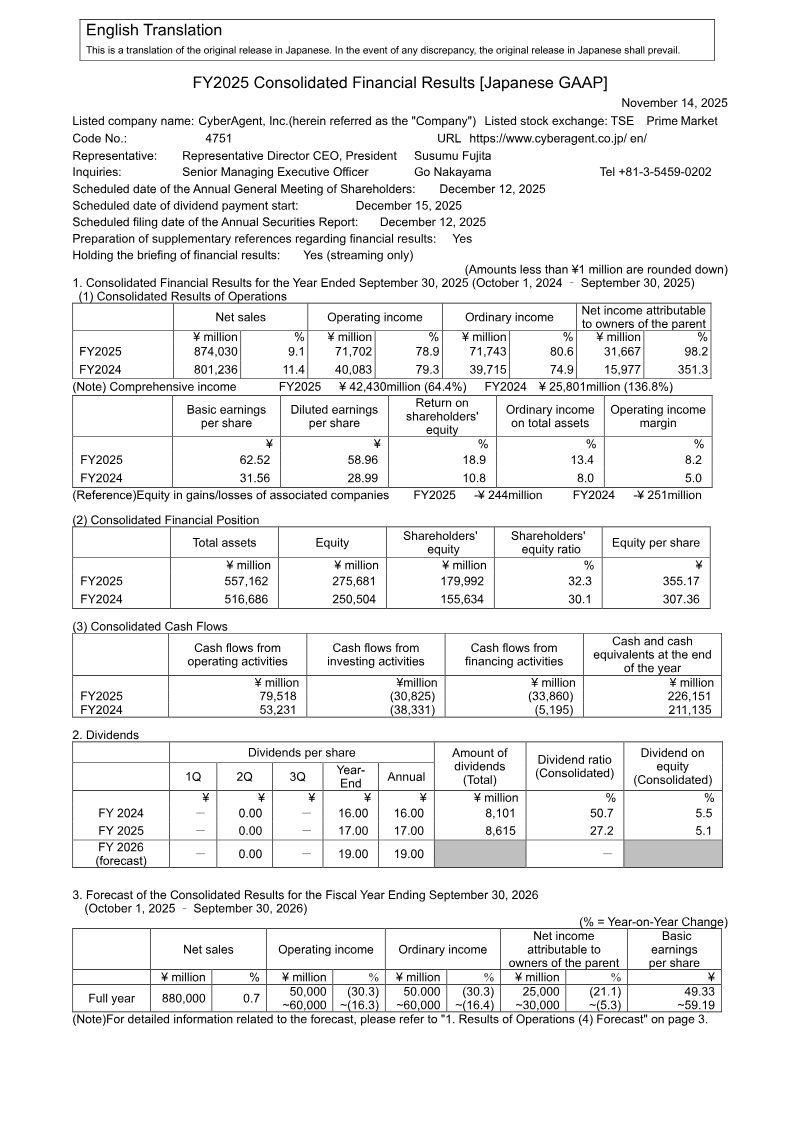

CyberAgent's operating income surged 78.9% to ¥71,702 million in FY2025, driven primarily by the Game Business, which nearly doubled its operating income to ¥60,06 billion.

See it on page 4The Media & IP segment achieved its first annual profit in a decade, contributing ¥7.29 billion in operating income following a corporate reorganization to integrate ABEMA-related operations.

See it on page 4Consolidated net sales grew 9.1% to ¥874,030 million, while net income attributable to the parent doubled to ¥31.67 billion.

See it on page 11Growth in the gaming sector was fueled by aggressive overseas expansion and the adoption of high-margin external payment methods, successfully offsetting a ¥727 million patent infringement settlement between Cygames and Konami Digital Entertainment.

See it on page 14The company strengthened its financial position by generating ¥79,518 million in operating cash flow and executing a ¥20,000 million redemption of convertible bonds.

See it on page 4Management projects a cautious FY2026 outlook, forecasting a decline in operating income to between ¥50,000 and ¥60,000 million despite a modest projected sales increase to ¥880,000 million.

See it on page 5CyberAgent achieved a significant financial recovery during the 2025 fiscal year, characterized by a 9.1% increase in net sales to ¥874,030 million and a 78.9% surge in operating income to ¥71,702 million. This performance was underpinned by the Media & IP segment returning to profitability for the first time in a decade, generating ¥7.29 billion in operating income. The Game Business served as the primary engine for growth, with its operating income nearly doubling to ¥60.06 billion. This success in the gaming sector was attributed to aggressive overseas expansion and the adoption of high-margin external payment methods, which more than offset a ¥727 million extraordinary loss related to a patent infringement settlement between subsidiary Cygames and Konami Digital Entertainment.

The company’s financial position strengthened considerably over the period, with net income attributable to the parent doubling to ¥31.67 billion and cash flows from operating activities rising to ¥79,518 million. Strategic capital management included a ¥20,000 million redemption of convertible bonds and the acquisition of subsidiary shares. To better leverage synergies surrounding the ABEMA platform, the corporate structure was reorganized to integrate secondary operations into the newly designated Media & IP Business segment.

Looking toward the 2026 fiscal year, the outlook remains cautious despite the recent momentum. While consolidated net sales are projected to grow modestly to ¥880,000 million, operating income is expected to contract to a range between ¥50,000 and ¥60,000 million. This forecast suggests a period of reinvestment or market stabilization following the exceptional gains realized in the gaming and media sectors during the previous year. The results reflect a consolidated Japanese market focus with increasing international contributions from the gaming portfolio.