Report

Value Creation in the Metaverse: The Real Business of the Virtual World

The analysis evaluates the emerging economic significance of immersive digital environments, arguing that the metaverse will become a major engine of growth and societal transformation by 2030. It positions the metaverse as the next immersive iteration of the internet, driven by real‑time interactivity, user agency and eventual cross‑platform interoperability, and stresses that firms must define clear objectives, pilot test use cases, and build talent and technology capabilities now to capture value while managing ethical, security and workforce‑reskilling risks. Investment activity surged in early 2022, with more than $120 billion flowing into the ecosystem across venture capital, private‑equity, mergers and acquisitions and corporate spend. The influx was amplified by Microsoft’s $69 billion acquisition of Activision, and corporate budgets such as Meta’s $10 billion annual allocation underscore the scale of commitment. Survey data from over 3,400 consumers and executives reveal that roughly 60 % of early‑adopter users are eager to shift daily activities—socializing, entertainment, shopping and travel—into virtual spaces, while 95 % of senior leaders anticipate a positive industry impact and project up to $5 trillion in economic value by 2030, comparable to the size of Japan’s economy. Gaming remains the primary catalyst, supporting more than three billion users and a $200 billion market, and early adopters report higher profit margins. Across 19 industry sectors—including fashion and luxury, consumer‑packaged goods, retail, finance, utilities, manufacturing, education and government—XR‑enabled experiences are unlocking new revenue streams, with virtual‑goods sales already at roughly $40 billion and fashion brands leading digital‑identity initiatives. Executives rank cryptocurrency, artificial intelligence and AR/VR as the most important enabling technologies, yet cite uncertain ROI, lack of viable business models and insufficient managerial capability as chief barriers, while data‑privacy and cybersecurity concerns appear for over 85 % of leaders. Geographically, the findings draw on global surveys conducted in 11 countries, encompassing 3,104 consumer respondents and 448 C‑level executives, and reflect investment trends and use‑case experimentation worldwide. The outlook projects that by 2030 more than half of live events and over 80 % of commerce could occur in virtual environments, with users spending up to six hours daily in immersive experiences. Realizing this potential will require coordinated governance, inclusive design and robust regulatory frameworks to

McKinsey & CompanyJun 2022

Report

Turkey Game Market 2022 Report

The Turkish gaming market in 2022 serves as a critical case study of a high-growth production hub navigating significant domestic economic volatility. While the player base expanded to over 44 million users—with 81% of adults engaging in mobile gaming—total market revenue saw a sharp correction, falling from $1.2 billion in 2021 to approximately $625 million. This decline was primarily driven by the depreciation of the Turkish Lira and weakened consumer purchasing power, which has accelerated a shift toward free-to-play titles, subscription services, and a demand for high-quality localization to reach a population with generally low English proficiency. Despite these fiscal challenges, Türkiye has solidified its position as a global leader in gaming investment and development. Istanbul ranks second in Europe and fifth globally for gaming transactions, securing over $424 million in investments across dozens of deals. The domestic ecosystem is maturing beyond its historical focus on hyper-casual mobile titles, with over 2,943 publishers on Google Play and a strategic pivot toward indie, PC, console, and hybrid-casual development. This evolution is supported by a robust infrastructure of 25 entrepreneurship centers and 19 university programs, though a deficit in qualified instructional talent remains a hurdle for long-term sustainability. The region has also emerged as a premier esports destination, evidenced by hosting the VALORANT Champions Tour and the formal legal recognition of the Turkish Esports Federation, which oversees more than 15,000 licensed players. While traditional segments like internet cafes have declined due to rising operational costs, the integration of gamification into e-commerce and corporate sectors is expanding. Moving forward, the industry is expected to maintain a compound annual growth rate of 24.1% through 2026, driven by blockchain integration, AI technologies, and a transition toward more complex, mid-core gaming experiences.

Gaming in TurkeyApr 2023

Report

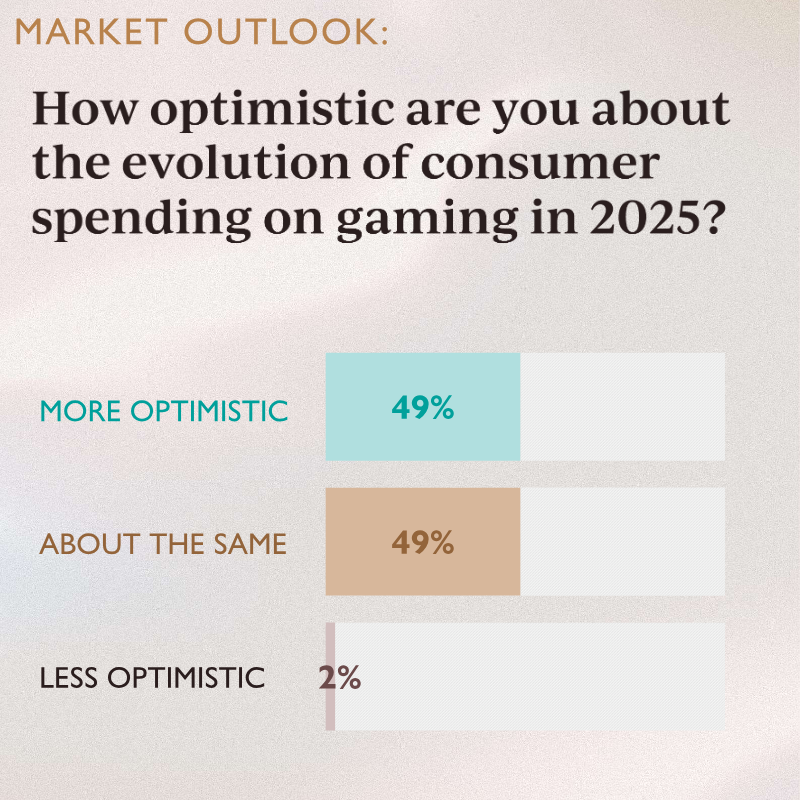

Gaming CEO Survey: 2024 in Review

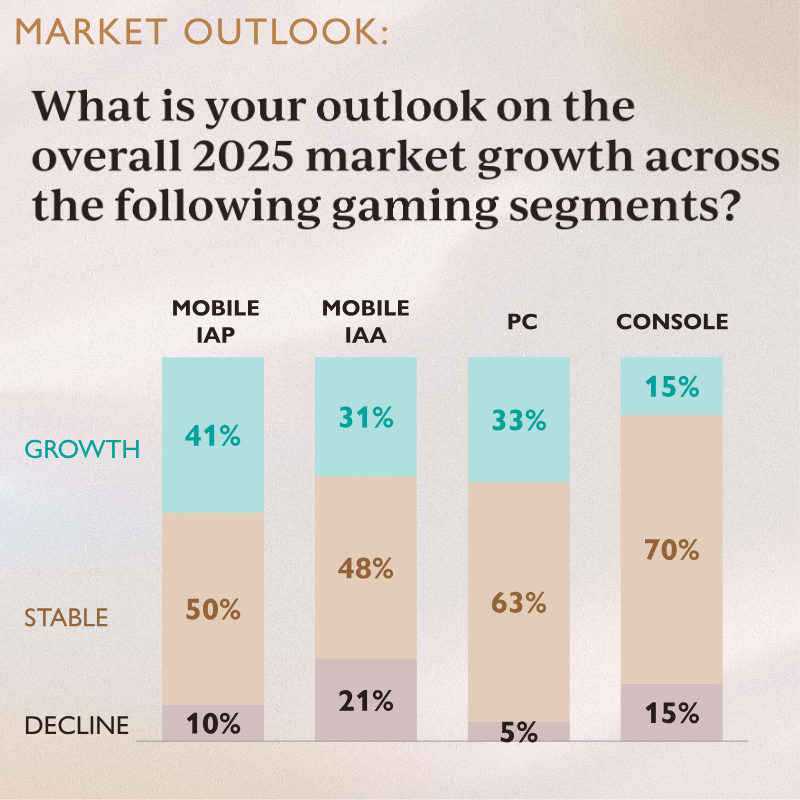

Industry leadership maintains a cautiously optimistic outlook for 2025, with 98% of executives expecting consumer spending to either increase or remain stable. Growth expectations are strongest in the mobile sector, where 41% of leaders anticipate expansion in in-app purchases and 31% expect growth in advertising revenue. While the PC segment remains relatively healthy with a 33% growth projection, the console market appears more stagnant, as 70% of respondents forecast stable performance and only 15% predict growth. This outlook is tempered by concerns regarding content saturation and a challenging user acquisition environment, which are cited as the primary hurdles facing the industry. Operational strategies for the coming year signal a shift toward expansion and increased investment. A majority of companies plan to initiate more game development projects in 2025 compared to the previous year, supported by higher or stable budgets and increased marketing spend. Talent acquisition remains a priority, particularly in game development and engineering roles. Furthermore, the mergers and acquisitions landscape is expected to intensify, with 71% of executives anticipating more opportunities in 2025 and none predicting a decrease in activity. Artificial intelligence has reached a significant level of penetration within the sector, with 84% of companies reporting either limited implementation or advanced integration across multiple functions. Executives identify art, game design, and engineering as the areas where AI will provide the most significant value. These findings, compiled by a leading global investment bank specializing in gaming, reflect a sector transitioning from a period of consolidation toward a renewed focus on production, technological integration, and strategic deal-making.

Aream & CoJan 2025

Report

Blockchain Game Alliance: State of the Industry 2024

The blockchain gaming sector is entering a phase of maturation characterized by a strategic pivot from speculative financial models toward high-quality, "fun-first" development. Player asset ownership remains the industry’s primary value proposition, cited by over 71% of professionals for four consecutive years. This shift is bolstered by the entry of traditional gaming giants such as Sony and Ubisoft, which provides necessary credibility to a field where 66.3% of practitioners still identify public misconceptions of scams as a major hurdle. While the industry faces a 42.7% decline in new hiring due to market uncertainty, professional sentiment remains resilient, with over 82% of workers intending to remain in the sector long-term. Geographically, the industry is expanding its footprint into the Middle East and South America, while Asia and Latin America lead in the adoption of player-reward mechanics. Despite this global reach, the sector continues to struggle with demographic challenges, including a lack of gender diversity and a decline in younger talent entering the workforce. Operationally, the most significant barriers to mainstream adoption are onboarding complexities and poor user experience, though the severity of these concerns has decreased significantly since 2023. Companies currently identify lack of funding and high user acquisition costs as their most pressing internal obstacles. Looking toward 2025, the industry is moving toward "invisible" Web3 infrastructure to prioritize seamless gameplay over technical complexity. Emerging trends include the rise of fully onchain games, the integration of artificial intelligence for personalized experiences, and the use of social platforms like Telegram to simplify user acquisition. As environmental concerns continue to fade, the focus has shifted toward sustainable "play-and-earn" economies and the consolidation of fragmented infrastructure. This evolution suggests a transition toward a more integrated gaming ecosystem where blockchain serves as a foundational layer for digital property rights rather than a standalone marketing feature.

Blockchain Game AllianceJan 2024

Report

State of Web3 in Saudi Arabia

Saudi Arabia has emerged as the dominant hub for Web3 investment in the Middle East and North Africa, capturing 51 % of Q1 2024 venture‑capital funding with $429 million across 163 deals. This concentration reflects a supportive ecosystem that blends proactive government initiatives, a growing pool of local founders, and active participation from international investors. The market is presently skewed toward consumer‑facing applications such as DeFi, GameFi and SocialFi, while foundational protocol development remains limited, highlighting a clear opening for infrastructure builders. Founders of Saudi‑based Web3 ventures underscore the rapid maturation of the sector, citing high‑profile partnerships—including Animoca Brands with NEOM, collaborations with Hedera, and alignment with Vision 2030—as catalysts for growth. Yet they identify three persistent barriers: inadequate user‑friendly interfaces, insufficient public and investor education, and ambiguous regulatory frameworks that impede both builder activity and funding cycles. Sector‑specific use cases—blockchain‑enabled freelance payments, Sharia‑compliant insurance, and localized NFT platforms—are viewed as primary drivers of mass adoption. Government commitment reinforces this trajectory, with $37.7 billion earmarked for esports and $13.3 billion for gaming, complemented by sizable venture funds such as Wa’ed’s $500 million vehicle and 500 Global’s $2.4 billion under management. Notable projects illustrate tangible impact: Tharawat Green Exchange aims to plant ten million trees by 2030, while Ticket Souq has generated $3.3 million in gross merchandise value, serving 36 k users across 55 events in ten countries. Stakeholders agree that clear, supportive regulation, robust education, and targeted technology investment are essential to translate this momentum into sustainable, high‑pay‑off outcomes for the kingdom’s burgeoning gaming, fintech, e‑commerce and proptech sectors.

AdaverseJul 2024

Report

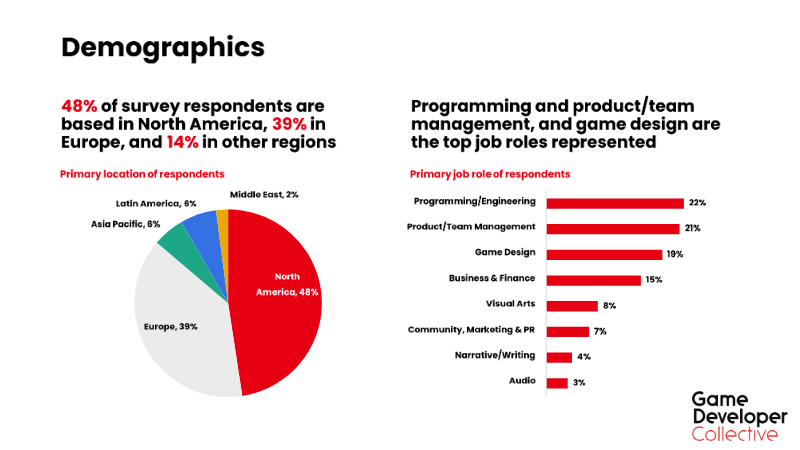

Game Developer Collective Survey Results: November 2024

The November 2024 Game Developer Collective Survey examines how game developers allocate resources to software tools and services, focusing on the adoption of game engines, cloud platforms, and ancillary technologies. The central thesis is that while the market now offers a broader array of solutions than ever before, studios face divergent realities: many are eager to leverage these options to boost efficiency and output, yet a substantial portion confronts tightening budgets that limit further investment. This tension is reflected in the “Industry Conditions and Performance” findings, which portray a challenging commercial environment for the sector. Key observations indicate that developers increasingly view diversified toolsets as pathways to improved productivity, but cost pressures are intensifying across regions. The survey highlights a split between studios that can expand their technology stack and those that must defer additional spending, underscoring a growing disparity in capability to innovate. The analysis also signals that forthcoming research on “Working Environments,” slated for release in January 2025, will delve deeper into how these financial constraints intersect with workplace dynamics and talent management. The study spans a global developer base, encompassing respondents from the Americas, Europe‑Middle East‑Africa, and Asia‑Pacific, and captures sentiment as of November 2024. Although specific sample sizes and data sources are not disclosed in the excerpt, the findings are presented under the Omdia research umbrella, with standard disclaimer language indicating that the material is provided “as‑is” and reflects the original publication date. The survey’s conclusions serve as a barometer of current investment trends and the fiscal pressures shaping the game development landscape.

Game Developer CollectiveNov 2024

Report

State of Play: Spring Edition

Mobile gaming has solidified its position as the industry’s primary driver, currently engaging 1.9 billion players and tracking toward $118 billion in annual revenue by 2027. This growth is occurring alongside a fundamental restructuring of digital commerce. Regulatory shifts, such as the European Union’s Digital Markets Act and recent judicial rulings, are dismantling the traditional walled gardens of major app stores. By forcing the adoption of alternative billing systems and out-of-app commerce, these changes allow developers to bypass standard commission fees and engage in direct-to-consumer marketing, fundamentally altering the economics of mobile distribution. The industry is simultaneously transitioning toward a cross-platform ecosystem where seamless play and unified payment systems across mobile, PC, and console are becoming standard. Consumer behavior supports this shift, as 87% of multiplayer gamers now engage in cross-platform play. Younger demographics, specifically Gen Alpha and Gen Z, exhibit a 52% payer conversion rate, significantly outperforming older cohorts. To capture this value, developers are increasingly forming strategic alliances with telecommunications providers to integrate 5G infrastructure and mobile wallets, ensuring frictionless transactions in a "cross-pay" environment. Despite a significant cooling in investment during 2023—characterized by a 75% drop in Web3 funding and a 43% decline in merger and acquisition activity—the sector is recalibrating toward a sustainable "new normal." The workforce is becoming more formalized, with nearly three-quarters of designers holding university degrees. Market analysts anticipate a recovery throughout 2024, marked by a 20% increase in deal flow and the entry of major media entities like Netflix and Disney. This stabilization is supported by a shift in venture capital toward alternative models that prioritize marketing and operational support over traditional equity-only investments.

XsollaMar 2024

Report

Turkey Game Market 2021 Report

The Turkish gaming market experienced a transformative period of growth and institutionalization in 2021, reaching a total market volume of $1.2 billion. Despite global challenges such as hardware shortages and pandemic-related delays in AAA titles, the local ecosystem expanded to include over 42 million active players. This growth was primarily catalyzed by the mobile segment, which generated $620 million in revenue and solidified Turkey’s position as a global leader in the hyper-casual genre. The year was further defined by record-breaking financial activity, with $266 million invested across 54 startups and the emergence of Dream Games as a new industry "unicorn." Strategically, the market is shifting toward a "gaming-focused entertainment" model, characterized by the rapid adoption of Web3 technologies, including blockchain, NFTs, and Play-to-Earn (P2E) frameworks. While mobile gaming remains the dominant force, there is a burgeoning esports ecosystem supported by approximately 6 million followers and a national federation overseeing 165 licensed clubs. Turkey’s selection as the host for the Global Esports Games 2022 underscores its rising international profile. However, industry experts note a strategic need to diversify beyond mobile platforms into PC and console development to ensure long-term sustainability. The regional landscape reveals Turkey as the primary gaming powerhouse in the Middle East, outperforming neighboring markets in both revenue and player engagement. Success for international entrants remains contingent on high-quality localization and cultural adaptation, given the country's low English proficiency and unique consumer preferences for competitive genres and specific musical influences. As the sector transitions into 2022, the focus remains on bridging the talent gap through specialized academic programs and leveraging the return of large-scale physical exhibitions to maintain momentum in the evolving Metaverse and digital advertising spaces.

Gaming in TurkeyJan 2021