Related Documents

Financial

Q4 2025 Interim Report

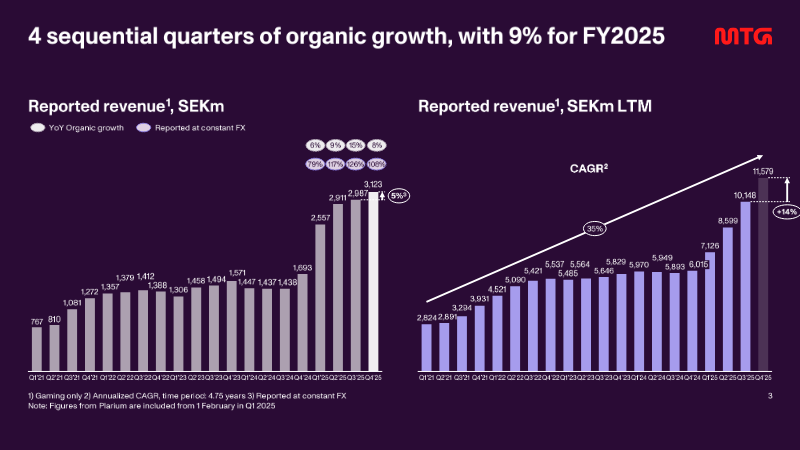

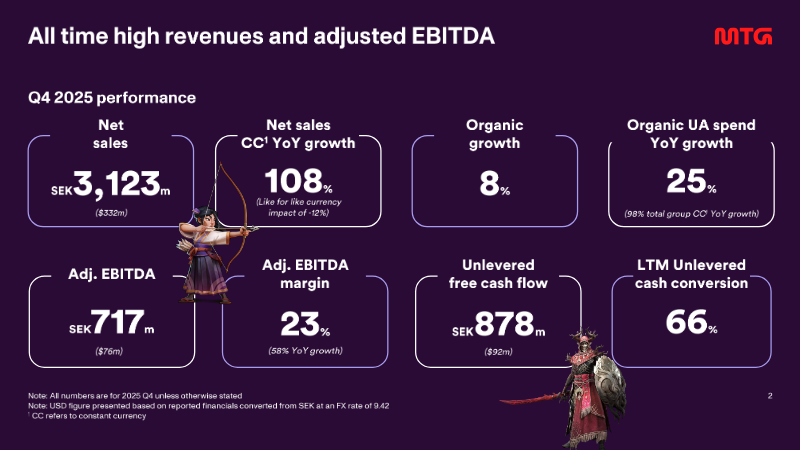

The interim filing presents the fourth‑quarter 2025 financial results for a midcore‑casual gaming group, emphasizing a record‑setting revenue run and the successful execution of a transformation agenda that includes the integration of the Plarium acquisition and the rollout of a new district structure in early 2026. Revenue reached SEK 3,123 million, reflecting 108 % organic growth year‑on‑year and a 25 % increase on a constant‑currency basis, while adjusted EBITDA rose to SEK 717 million, delivering a 23 % margin that matches the full‑year figure. Unlevered free cash flow amounted to SEK 878 million, with a cash‑conversion rate of 66 % and a leverage ratio of five times EBITDA, underscoring robust liquidity and disciplined capital management. User‑acquisition spending accelerated, representing 38 % of quarterly revenue—up from 37 % in the prior quarter—and grew 76 % on a reported basis, driven by heightened investment in original studios, new casual titles, and the racing franchise. The direct‑to‑consumer channel expanded by 600 basis points to 32 % of total revenue, reflecting a strategic shift toward higher‑margin in‑app purchases. Across the fiscal year, the company posted a 9 % organic revenue increase, with word‑games, racing, and RAID franchises delivering the strongest quarter‑end performance. Operating cash flow for the quarter stood at SEK 840 million, while adjusted net income was SEK 1,390 million, translating to an adjusted EPS of SEK 11.33. The financial outcomes exceed guidance and position the firm to meet its medium‑term outlook, with a pre‑IPO study for PlaySimple concluded and the midcore transformation progressing as planned.

Modern Times GroupFeb 2026

Report

Beyond the Game: How Gamification is Becoming Mainstream

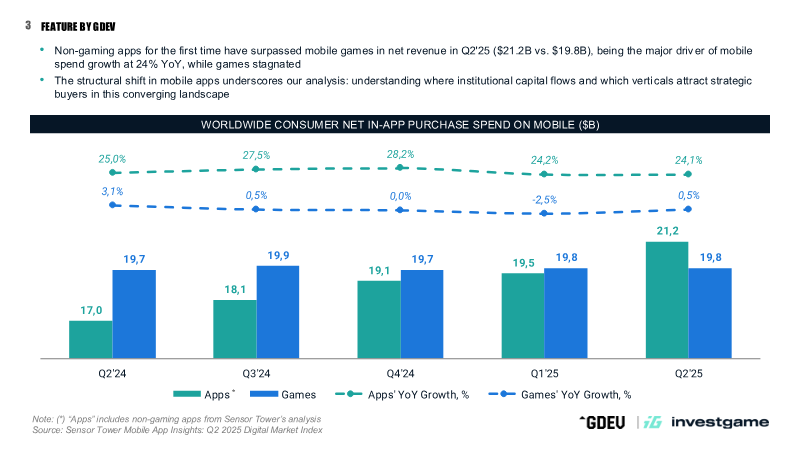

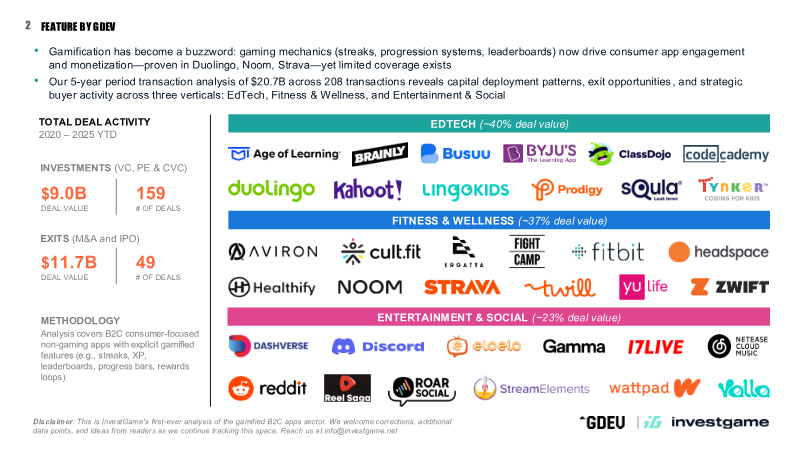

The analysis examines how gamification—applying game‑like mechanics such as streaks, leaderboards, and reward loops—to non‑gaming consumer apps has shifted the mobile app economy over a five‑year period (2020‑2025). Data from 208 transactions totaling $20.7 billion reveal that EdTech, Fitness & Wellness, and Entertainment & Social are the primary verticals, with deal value shares of roughly 40 %, 37 %, and 23 % respectively. EdTech dominates both deal volume (43 %) and exit activity, accounting for 45 % of exits and 34 % of exit value, indicating a mature market attractive to strategic buyers. Fitness & Wellness shows concentrated exits in two mega‑deals (Headspace $3 billion, Fitbit $2.1 billion) but a broader spread of capital across many platforms, suggesting growth potential beyond the top brands. Entertainment & Social receives steady, diversified investment; its exits lean toward IPOs (e.g., Reddit, NetEase Cloud Music) rather than M&A, reflecting limited strategic buyer appetite. Capital flows peaked during the 2020‑21 COVID boom but recovered quickly for gamified apps, with 2024 stabilizing and 2025 YTD already surpassing full‑year 2024 figures. Seed and Series A rounds remain active, while late‑stage activity accelerated in 2025 following earlier Series A momentum. Early‑stage capital is evenly split between Fitness & Wellness and Entertainment & Social, highlighting a white‑space opportunity, whereas EdTech shows limited early‑stage activity due to market consolidation. The report underscores that non‑gaming apps have overtaken mobile games in net revenue (Q2 '25: $21.2 billion vs. $19.8 billion) and are driving 24 % YoY mobile spend growth, while games stagnated. This structural shift signals that institutional capital increasingly targets gamified consumer apps across these three verticals, with strategic buyers actively consolidating the EdTech segment and exploring IPO pathways in Entertainment & Social.

InvestGame

Report

Global Gaming Report Q1 2026

LOS ANGELES | SAN FRANCISCO | NEW YORK | LONDON | PARIS | MUNICH | BERLIN | DUBAI PROVEN TRACK RECORD IN GAMING M&A AND GROWTH FINANCING ADVISORY PROVEN TRACK RECORD IN GAMING M&A AND GROWTH FINANCING ADVISORY MICHAEL METZGER JULIAN RIEDLBAUER Linkedin - Free social media icons MOHIT PAREEK Linkedin - Free social media icons MICHAEL METZGER JULIAN RIEDLBAUER ...

Drake Star PartnersApr 2026

Report

Video Game Market Update: Q1 2026

This report is provided for general information and discussion purposes only and is intended solely for subscribers. It does not constitute a financial promotion, investment advice, or a recommendation to engage in any investment activity. The content reflects the views of the authors at the time of publication and may be subject to change without notice.

Aream & CoApr 2026