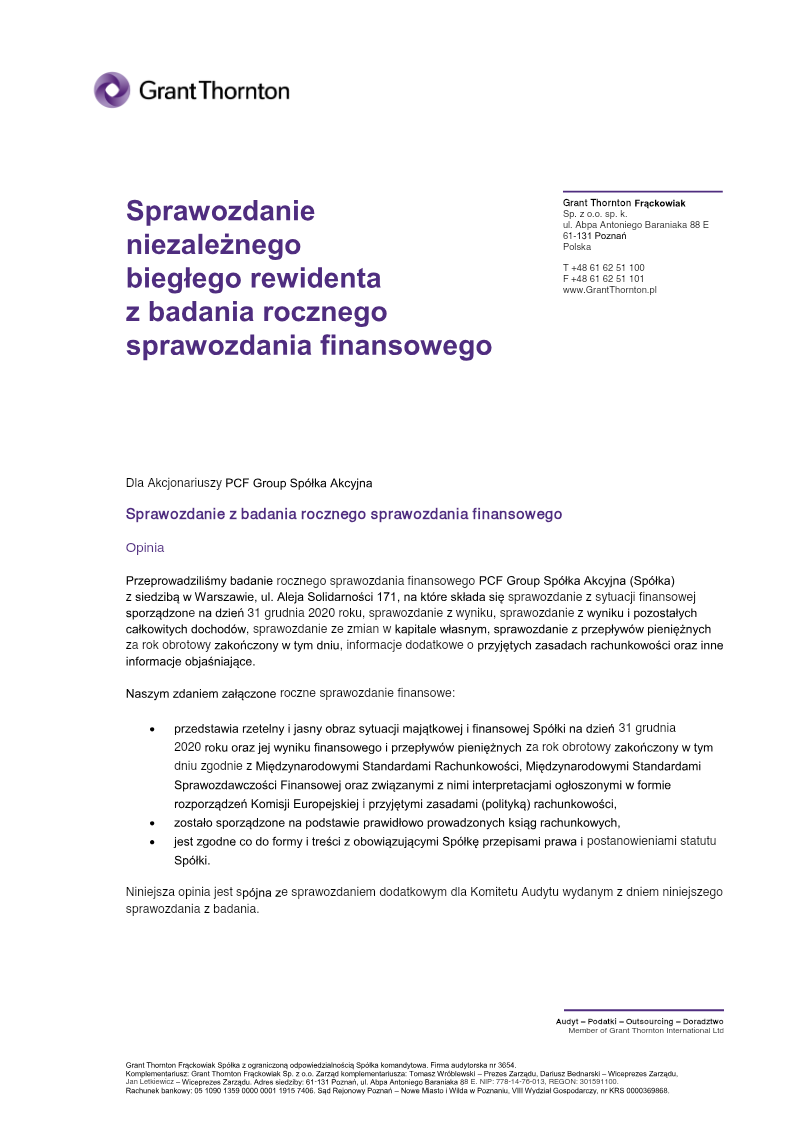

ReportPCF Group

Independent Auditor's Report: Annual Financial Statement 2020

6 pages~14 min full read

PCF Group received an unqualified audit opinion for its 2020 financial statements, confirming they present a true and fair view in compliance with IFRS and EU regulations.

See it on page 1The audit confirmed that PCF Group’s financial records are accurate and free from material misstatements resulting from error or fraud as of 31 December 2020.

See it on page 1Auditors focused specifically on the valuation of contract-based receivables and obligations, which involved complex, frequently modified agreements requiring significant management judgment.

See it on page 2Revenue recognition policies were evaluated under IFRS 15, with specific scrutiny applied to the allocation of transaction prices and estimates for variable considerations like bonuses and warranties.

See it on page 2The company’s annual report and corporate governance statement were found to be consistent with the financial statements and prepared in accordance with applicable legal requirements.

See it on page 5The audit engagement adhered to Polish auditing law, International Standards on Auditing (ISA), and EU Regulation 537/2014, with no prohibited non-audit services rendered.

See it on page 1The audit opinion confirms that PCF Group’s 2020 financial statements present a true and fair view of the company’s assets, liabilities, equity, income, expenses, and cash flows as of 31 December 2020. The statements comply with International Financial Reporting Standards, IFRS, and related EU regulations, and are based on properly maintained accounting records. The auditor’s responsibility was carried out under Polish auditing law, the International Standards on Auditing (ISA), and the EU Regulation 537/2014. Independence was maintained in accordance with IESBA ethics, and the audit team performed sufficient procedures to obtain reasonable assurance that no material misstatement exists due to error or fraud.

Key audit focus areas included the valuation of contract‑based receivables and obligations, where complex, frequently modified agreements required significant judgment. The auditor evaluated the company’s revenue recognition policies under IFRS 15, assessed estimates of variable consideration such as bonuses and warranties, and reviewed the allocation of transaction prices to identified performance obligations. These matters were disclosed in Notes 3 and 18 of the financial statements.

The audit also covered other information, including the annual report and corporate governance statement. The auditor expressed an unqualified opinion on these disclosures, finding them prepared in accordance with applicable laws and consistent with the financial statements. No material misstatements were identified, and no prohibited non‑audit services were rendered during the engagement.