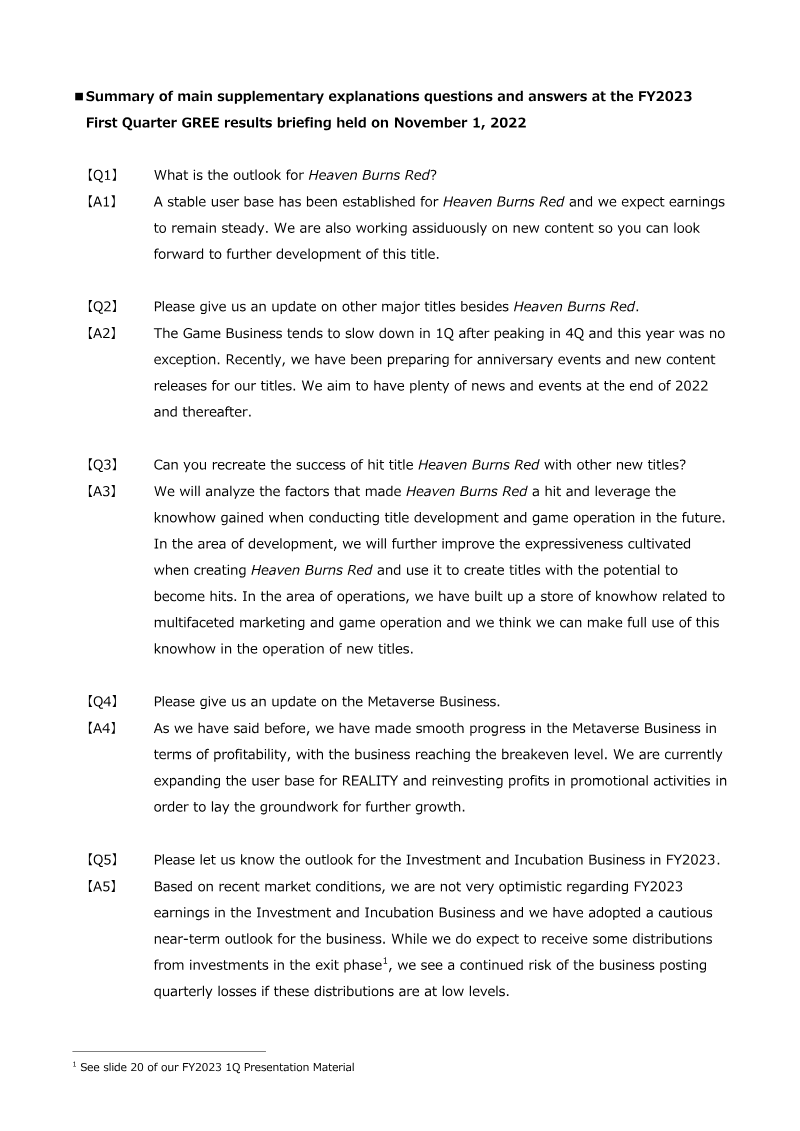

Key insights

4 takeaways · ~2 min read- 01

The provided report content for Q1 FY2026 covers the period of October through December 2025.

See it on page 16 - 02

The document outlines performance metrics specifically for the company's Internet Advertisement Business.

See it on page 3 - 03

Management explicitly notes that actual financial results may differ materially from the provided earnings forecasts due to inherent risks and uncertainties.

See it on page 2 - 04

The report serves as formal presentation material for the first quarter of the 2026 fiscal year.

See it on page 7