Related Documents

Report

Aream & Co. Gaming CEO Survey 2025

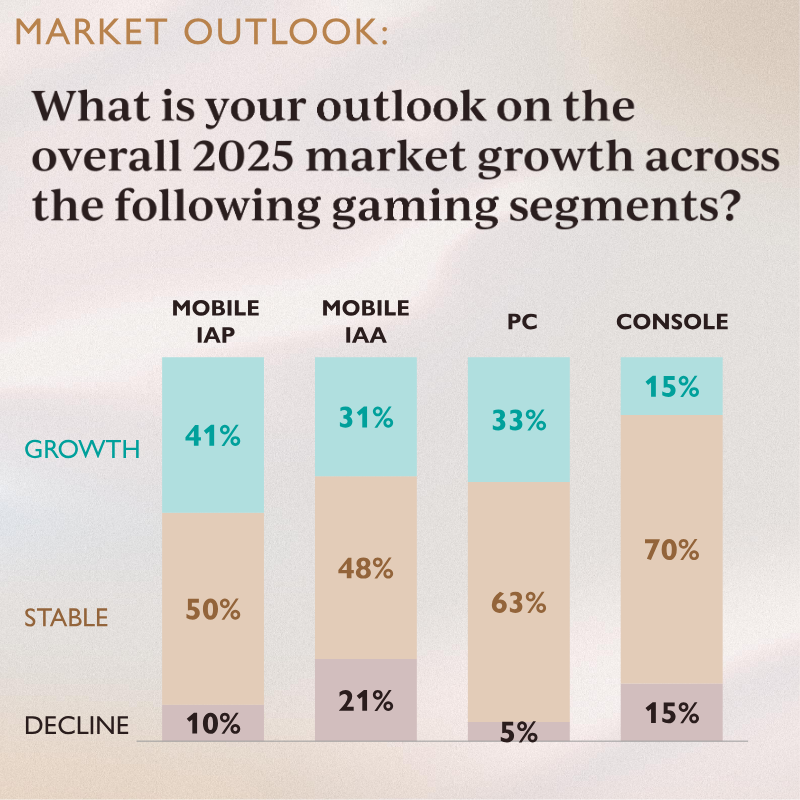

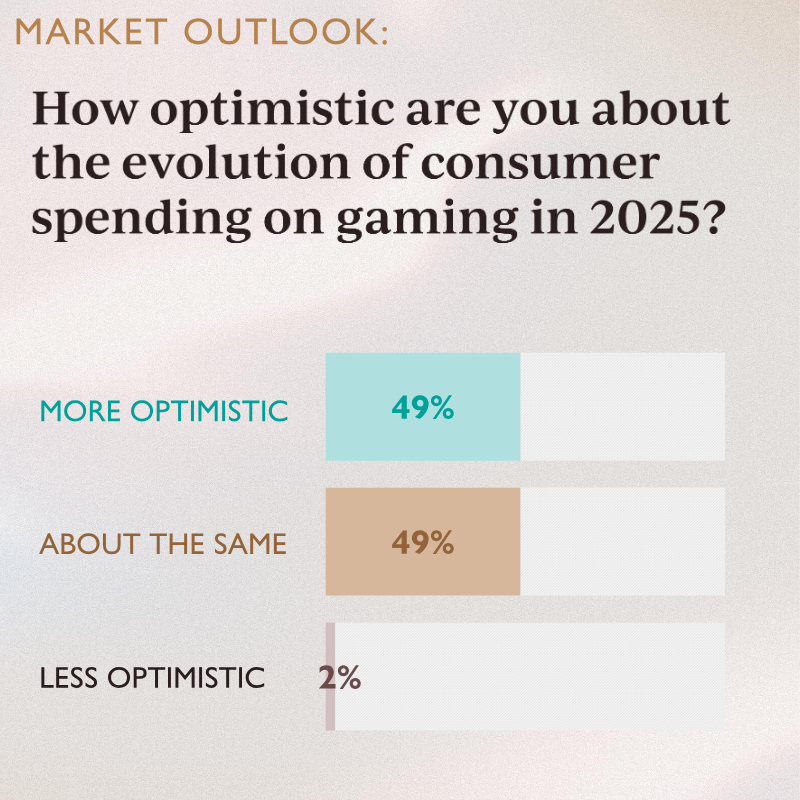

The survey, conducted by Aream & Co., gauges executive optimism regarding consumer spending on gaming in 2025 across multiple channels and functional areas. Overall, 49 % of respondents view spending as “more optimistic,” another 49 % see it as unchanged, and only 2 % are less optimistic. When broken down by platform, mobile spending is perceived as more optimistic (49 %) while PC and console views are split between “more” (15–33 %) and “about the same.” In‑app purchases are viewed as more optimistic (80 %) versus in‑app advertising (41 %). Key challenges identified include content saturation and over‑supply, with 33 % citing these as concerns; marketing environment issues affect 49 %, and macro conditions are a worry for 17 %. Despite these, 54 % anticipate more new games in 2025, and 37 % expect higher average budgets. Marketing spend is expected to rise for 48 %, while engineering and game development are seen as more optimistic (71 % and 42 %). The survey also highlights a strong appetite for mergers and acquisitions, with 71 % expecting more M&A activity. Advanced integration across multiple functions is viewed as more optimistic (49 %) but limited implementation remains a concern. The data derive from a global sample of gaming CEOs, reflecting perspectives across mobile, PC, console, and various functional departments. The findings suggest a cautiously optimistic outlook for 2025, tempered by supply‑side pressures and marketing challenges.

Aream & CoFeb 2026

Report

Gaming Industry Report: Q3 2024

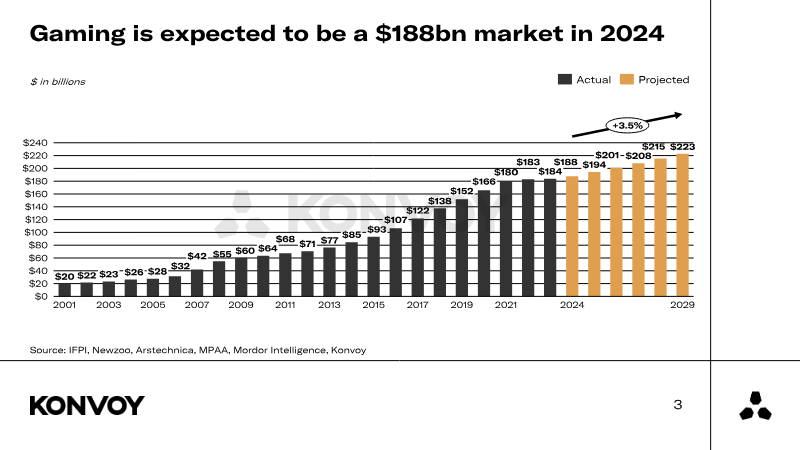

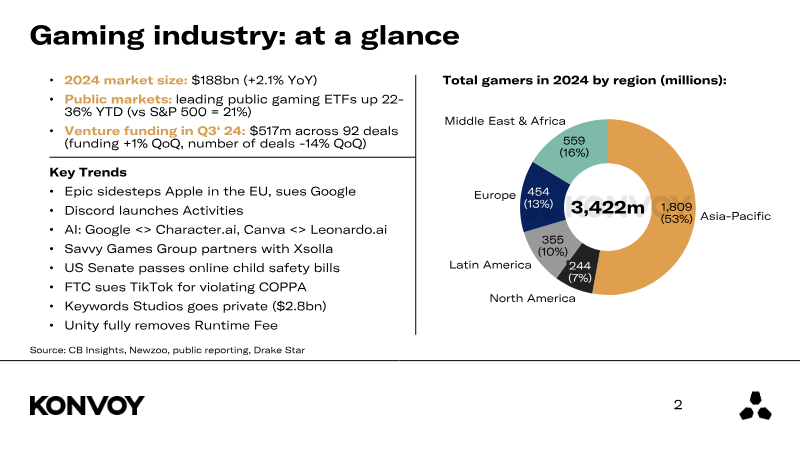

• 2024 market size: $188bn (+2.1% YoY) Total gamers in 2024 by region (millions): • Public markets: leading public gaming ETFs up 22- • 36% YTD (vs S&P 500 = 21%) Middle East & Africa Venture funding in Q3‘ 24: $517m across 92 deals 559 (funding +1% QoQ, number of deals -14% QoQ) (16%) • Epic sidesteps Apple in the EU, sues Google Europe (454 3,422m • Discord launches Activities ...

KonvoyOct 2024

Financial

Console/PC Games Investment Report 2024

Investment activity within the console and PC gaming sectors throughout 2023 reveals a strategic focus on early-stage developers, artificial intelligence integration, and blockchain-enabled platforms. Venture capital firms and strategic corporate investors prioritized studios capable of delivering high-fidelity experiences or innovative user-generated content tools. Andreessen Horowitz emerged as a leading contributor, deploying $82 million across various rounds, highlighted by a $55 million Series A investment in The Believer Company. This trend underscores a broader industry movement toward backing unproven but high-potential studios during their foundational stages. The funding landscape also highlights the significant role of strategic industry players like KRAFTON and specialized funds such as Makers Fund. KRAFTON’s involvement included a notable $30.7 million post-IPO equity injection into People Can Fly, while Makers Fund distributed $22.5 million across multiple early-stage ventures including Noodle Cat Games and World Makers. These investments suggest a dual interest in established mid-tier developers and lean, agile startups focusing on niche PC markets. Blockchain and Web3 gaming remained a resilient segment for capital allocation, particularly through investors like Merit Circle and Polygon. These firms concentrated on seed-stage rounds for developers such as Farcana, which secured $10 million, and Delabs Games. The data indicates that while the broader market faced economic headwinds, specialized sectors involving AI-driven development and decentralized gaming infrastructure continued to attract tens of millions of dollars in capital. Overall, the 2023 investment cycle was defined by a preference for Series A and Seed rounds, signaling a long-term bet on the next generation of console and PC intellectual property.

DDMSept 2024

Financial

Nintendo Q1 FY2024 Financial Results (English)

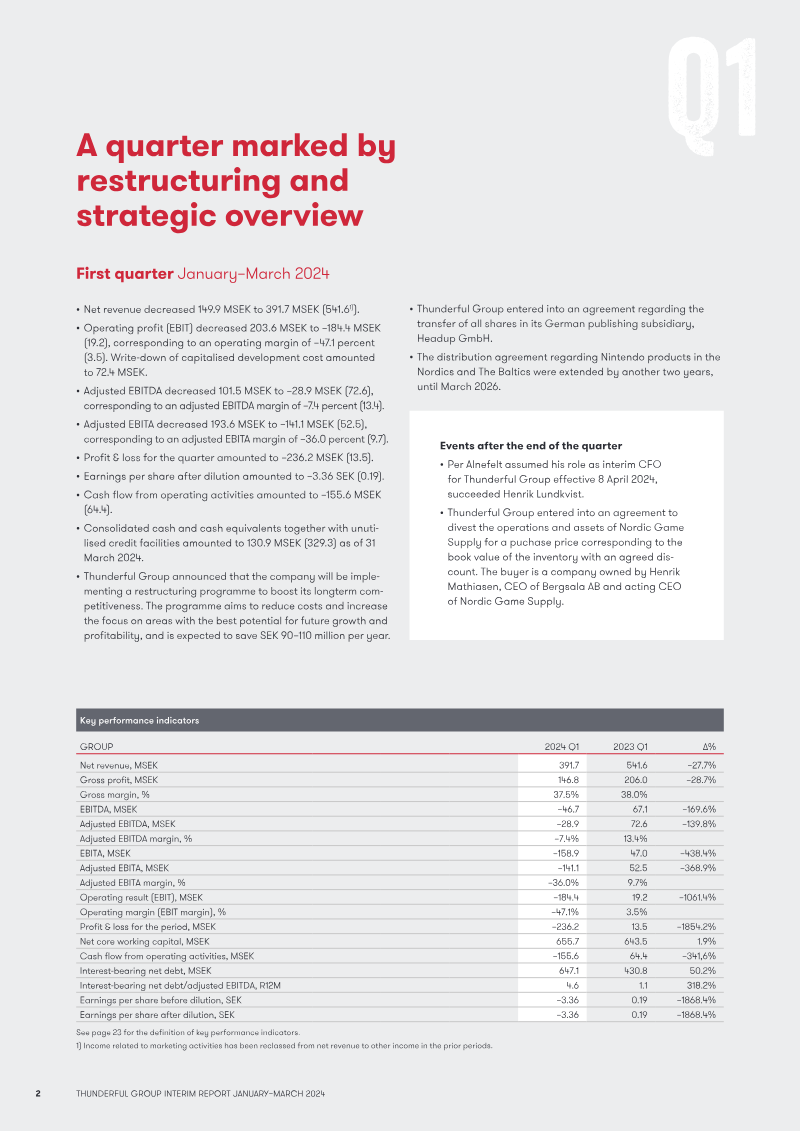

Thunderful Group’s interim report for the first quarter of 2024 details a period of significant financial decline and aggressive corporate restructuring. Net revenue fell 27.7 percent to 391.7 MSEK, while the group recorded an operating loss (EBIT) of 184.4 MSEK, a sharp reversal from the 19.2 MSEK profit reported in the same period the previous year. This downturn was driven by a 35.5 percent revenue drop in the Games segment and a 25.7 percent decrease in Distribution, largely due to weaker market demand for Nintendo Switch products and the underperformance of the internal title SteamWorld Build. To address these challenges, the group initiated a restructuring program aimed at annual cost savings of 90–110 MSEK. This process involved a 72.4 MSEK write-down of capitalized development costs following the cancellation or divestment of twelve game projects. Strategic shifts include the divestment of the German publishing subsidiary Headup GmbH and the sale of Nordic Game Supply’s assets to reduce net debt. Despite these pressures, the group successfully extended its Nintendo distribution agreement for the Nordics and Baltics through March 2026 and reported 13.9 percent growth in its Amo Toys division. The report covers the group’s global operations with a focus on European and Nordic markets for the period of January to March 2024. Financial data indicates a strained liquidity position, with cash and credit facilities dropping to 130.9 MSEK from 329.3 MSEK year-over-year. Management secured a bank waiver conditional on asset divestments and maintains that current funds are sufficient for continued operations. The overarching strategy moving forward emphasizes a simplified games portfolio, more rigorous project validation, and a balanced risk profile across internal and external development.

NintendoJan 2024