Legal11 bit studios

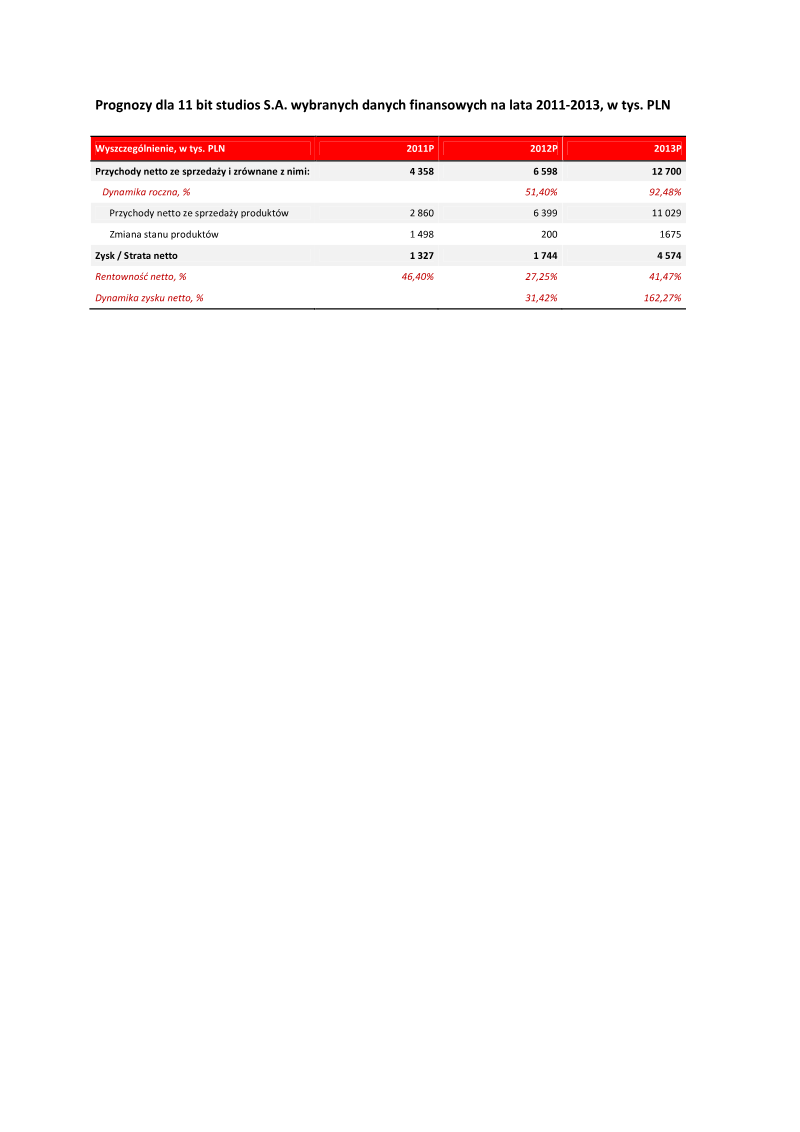

Selected Financial Data and Projections 2011–2013 — 11 bit studios S.A.

1 May 20151 pages~1 min full read

11 bit studios S.A. projects net revenue to grow from 4.36 million PLN in 2011 to 12.7 million PLN by 2013, driven by a 92.48% revenue increase in the final year.

Net profit is forecasted to more than triple over the three-year period, rising from 1.33 million PLN in 2011 to 4.57 million PLN by 2013.

The company expects a significant 162.27% year-over-year increase in net income between 2012 and 2013.

Product sales are identified as the primary growth engine, with revenue from this segment projected to reach 11.03 million PLN by 2013.

Net profit margins are expected to fluctuate due to development cycles, starting at 46.4% in 2011, dipping to 27.25% in 2012, and recovering to 41.47% in 2013.

The financial projections indicate a strategic transition for the studio from early-stage development to a high-output commercial phase.

Financial projections for 11 bit studios S.A. between 2011 and 2013 indicate a period of aggressive expansion and increasing profitability within the digital entertainment sector. The primary objective of these forecasts is to outline the anticipated growth trajectory for net sales revenues and bottom-line earnings over a three-year horizon. Total net revenues are expected to rise from 4.36 million PLN in 2011 to 12.7 million PLN by 2013, representing a significant compound growth rate. This upward trend is particularly pronounced in the final year of the forecast, where annual revenue growth is projected to accelerate to 92.48% following a more moderate 51.4% increase in 2012.

The data highlights a robust correlation between product sales and overall net profit. While net profit is estimated at 1.33 million PLN for 2011, it is expected to more than triple to 4.57 million PLN by the end of 2013. This surge is characterized by a massive 162.27% year-over-year increase in net income during the final period. Net profitability margins show some volatility, starting at a high of 46.4% in 2011 before dipping to 27.25% in 2012 and recovering to 41.47% in 2013. These fluctuations likely reflect the cyclical nature of game development cycles and the timing of major product releases.

The scope of these figures is limited to the internal financial performance of the Polish studio, focusing specifically on net sales of products and changes in product inventories. By 2013, the revenue from product sales alone is expected to reach 11.03 million PLN, serving as the primary engine for the company's valuation. These projections suggest a strategic transition from early-stage development toward a high-output commercial phase, positioning the studio for substantial scaling within the global gaming market.