Related Documents

Report

Global Gaming M&A and Growth Financing Advisory: Q1 2025

The global gaming industry experienced a notable resurgence in early 2025, characterized by a rebound in merger and acquisition activity and sustained interest in private financing. During the first quarter, 48 announced acquisitions reached a total value of $4.4 billion, anchored by the significant $3.5 billion acquisition of Niantic’s games division by Scopely. Simultaneously, the private placement market remained active, recording 149 deals worth $3.5 billion. These investments were primarily concentrated in mobile-focused developers and companies integrating artificial intelligence into their entertainment platforms, with major strategic entities like Savvy Games Group and Tencent continuing to drive market momentum. Despite this activity, the financial landscape remains bifurcated. While the broader sector shows signs of recovery, with the Drake Star Gaming Index posting a 16.37% gain, performance remains highly volatile across the top 35 public gaming companies. Valuation disparities are particularly pronounced; industry leaders such as NVIDIA and AppLovin command premium revenue multiples, while many other firms face a more challenging environment. Furthermore, while early-stage funding remains accessible, later-stage financing continues to present significant hurdles for companies seeking capital. Looking forward, the industry is positioned for a gradual increase in consolidation as public markets stabilize. Strategic focus is shifting toward the integration of AI and advanced technological platforms, which are expected to serve as primary catalysts for future growth. As market conditions improve, the sector is likely to see a renewed pipeline of initial public offerings, signaling a transition toward a more mature and diversified investment climate for global gaming stakeholders.

Drake StarJan 2025

Report

Q1 2024 Gaming Deals Report

The gaming industry is currently navigating a period of strategic stabilization defined by cautious capital deployment and a pivot toward long-term profitability. High interest rates and broader macroeconomic pressures have dampened late-stage financing and public listing activity, leading investors to prioritize capital efficiency over aggressive expansion. Despite these headwinds, the ecosystem remains supported by a robust foundation of over $15 billion in dry powder held across more than 65 gaming-focused funds, which continues to fuel a healthy pipeline of early-stage seed investments. Market performance is increasingly bifurcated across platforms. The PC and console sectors demonstrate notable resilience, bolstered by the consistent success of independent studios and sustained engagement on digital storefronts like Steam. In contrast, the mobile gaming market is undergoing a necessary contraction following post-pandemic volatility and the persistent impact of privacy-related advertising headwinds. While mobile startups currently face significant barriers to entry and a decline in late-stage venture interest, the sector is expected to initiate a gradual recovery by 2025 as business models adjust to the new regulatory and acquisition landscape. Looking ahead, the industry is transitioning away from the speculative growth patterns of previous years toward a more disciplined investment environment. Syndicate-based funding has emerged as a primary mechanism for risk mitigation, reflecting a broader trend of collaborative investment. As the market stabilizes, expectations are shifting toward an uptick in midcap merger and acquisition activity throughout the remainder of the year. This evolution underscores a fundamental industry-wide commitment to sustainable growth, with investors increasingly favoring established platforms and proven development teams over high-risk, late-stage ventures.

InvestGameJan 2024

Report

Gaming Report: Q1 2024

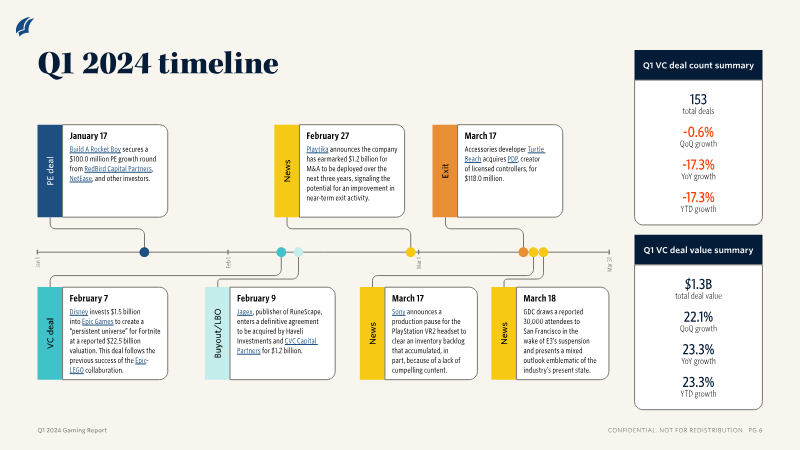

The gaming venture capital landscape in the first quarter of 2024 reflects a market reaching a steady state, characterized by a shift away from speculative Web3 and metaverse investments toward more sustainable development and content-focused funding. Global venture activity during this period totaled $1.3 billion across 153 deals. While deal count remained largely flat compared to the previous quarter, total deal value increased by 22.1% quarter-over-quarter. Despite a 17.3% year-over-year decline in deal volume, the market is currently on track to exceed 2023’s aggregate funding levels, suggesting a stabilization of capital deployment within a more realistic valuation environment. Development-focused companies, particularly those specializing in blockchain infrastructure and developer tools, captured significant attention in early 2024, momentarily outpacing content-focused investments. However, the broader industry remains highly competitive, with PC and console gameplay increasingly concentrated in established "forever titles." New content faces a challenging landscape, as only a small fraction of total playtime is dedicated to non-annual franchise releases. Investors are increasingly prioritizing high-quality content and scalable infrastructure, creating a more selective, investor-friendly environment. The report also highlights the growing importance of in-game advertising as a critical monetization strategy. With major industry players and brands integrating programmatic ad solutions, the sector is seeing increased utility for both developers and advertisers. Companies like Anzu exemplify this trend, leveraging technology to bridge the gap between brand reach and measurable return on investment. As the industry moves past the hype-driven cycles of the pandemic, the focus has shifted toward long-term operational efficiency and proven monetization models, with exit activity expected to improve as market conditions stabilize.

PitchBookJan 2024

Report

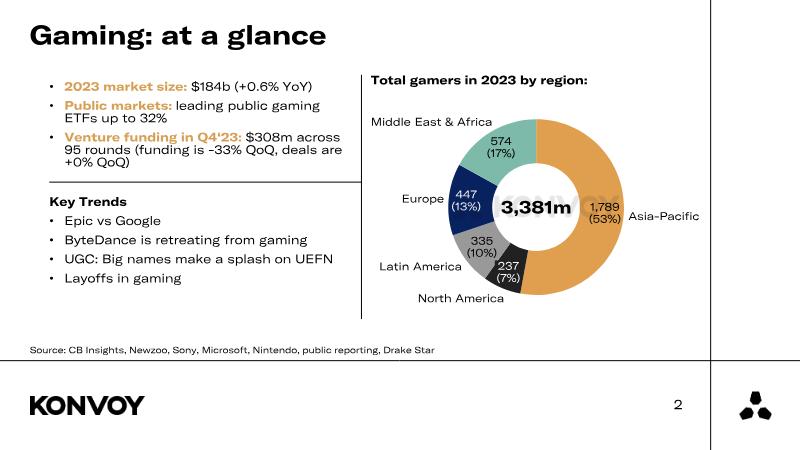

Gaming Industry Report: Q4 2023

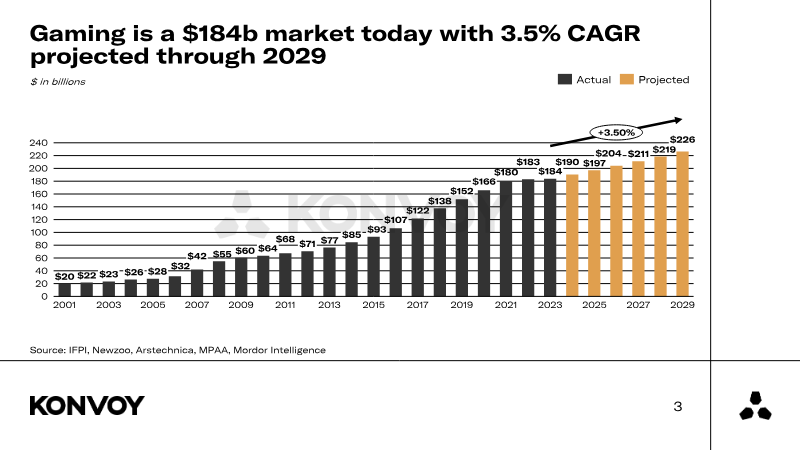

The global gaming industry reached a market valuation of $184 billion in 2023, representing a modest year-over-year growth of 0.6%. Despite this stability, the sector experienced a significant contraction in investment activity, with venture funding falling 33% quarter-over-quarter in Q4 to $308 million. This decline reflects a broader normalization of capital flows to pre-pandemic levels, as the industry shifts away from the high-growth, speculative environment of 2021 and 2022. Key industry trends in late 2023 were defined by regulatory and operational restructuring. A landmark legal verdict against Google established that its app store practices constituted an illegal monopoly, forcing potential shifts in how developers distribute content and process payments. Simultaneously, major players like ByteDance began retreating from gaming divisions, while the industry at large grappled with approximately 10,500 layoffs. These workforce reductions were driven by a heightened focus on operational efficiency, the prioritization of high-retention projects, and the consolidation of assets following major mergers and acquisitions. Geographically, North America remains the primary hub for venture capital, though the industry maintains a global footprint with significant activity in Asia and Europe. While venture funding and M&A deal volumes have stabilized, public gaming stocks demonstrated resilience, with leading exchange-traded funds outperforming broader market indices by year-end. Looking forward, the industry is projected to maintain a compound annual growth rate of 3.5% through 2029, supported by the continued integration of user-generated content platforms and advancements in developer tools that emphasize productivity and cost-effective scaling.

KonvoyJan 2024