Related Documents

Financial

Gaming Deals Report 2023: Striving for Elevation

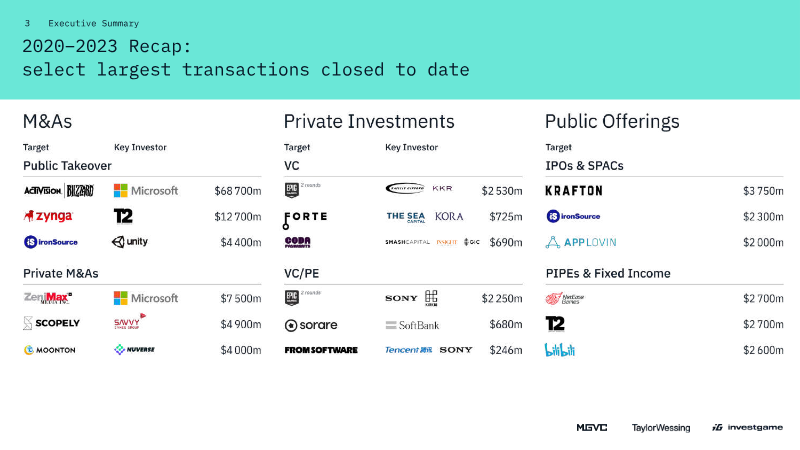

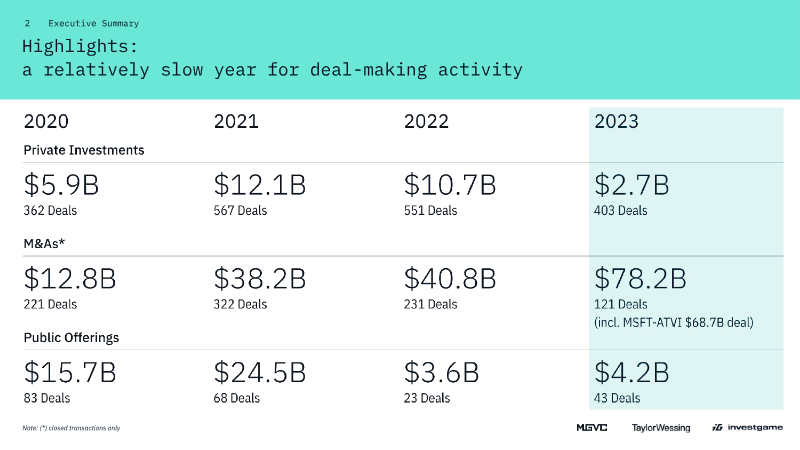

The 2023 Gaming Deals Report evaluates investment activity across the video‑game sector from 2020 through 2023, aiming to clarify how capital flows and transaction structures have reshaped the industry. By aggregating private‑equity, venture‑capital, and merger‑and‑acquisition data, the analysis demonstrates a pronounced shift from early‑stage financing toward large‑scale consolidation, while also tracking the emergence of artificial‑intelligence (AI) applications within game development and publishing. Overall capital raised by private‑equity and venture‑capital funds peaked at $12.1 billion in 2021 before retreating sharply to $2.7 billion in 2023, reflecting a contraction in early‑stage funding. The number of such deals followed a similar pattern, falling from a high of 567 in 2021 to 403 in 2023. In contrast, M&A activity accelerated dramatically, with closed‑deal value more than doubling from $40.8 billion in 2022 to $78.2 billion in 2023, even as the count of transactions remained modest. This divergence indicates that larger players are pursuing strategic acquisitions to capture market share and talent, while smaller firms face tighter financing conditions. AI‑related transactions, though still a niche segment, have shown a steady upward trajectory, with the cumulative count of closed AI deals rising from single‑digit figures in 2020 to over twenty in 2023. The report characterizes AI’s role as evolutionary rather than disruptive, suggesting that developers are integrating machine‑learning tools to enhance production efficiency and player experiences without fundamentally overturning existing business models. Collectively, the findings portray a gaming ecosystem in which capital concentration is intensifying, consolidation is accelerating, and emerging technologies are being incrementally adopted. Stakeholders are advised to monitor the narrowing gap between early‑stage funding and large‑scale M&A, as well as the growing relevance of AI, to anticipate future competitive dynamics.

InvestGameMar 2024

Report

Gaming Deals Activity Report: Q1–Q3 2022

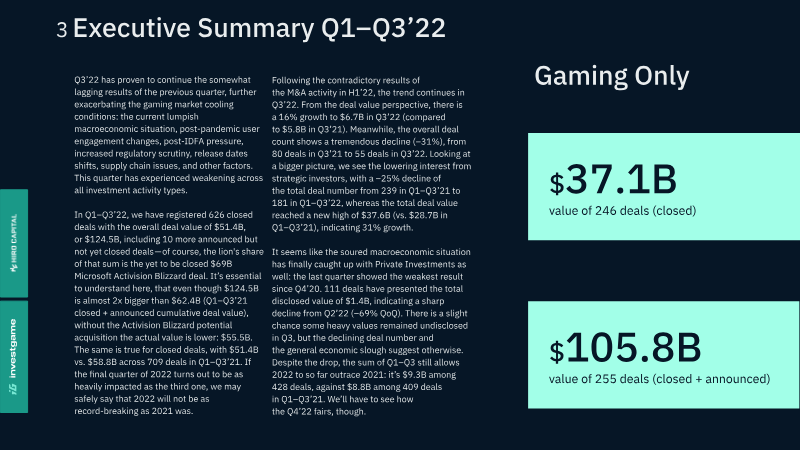

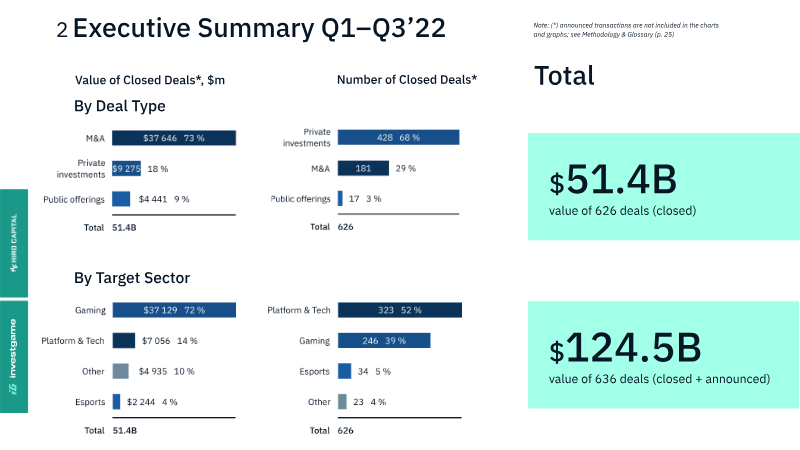

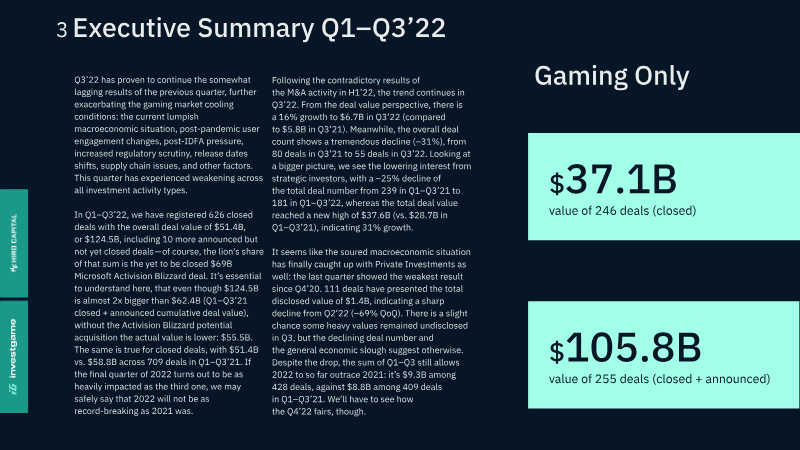

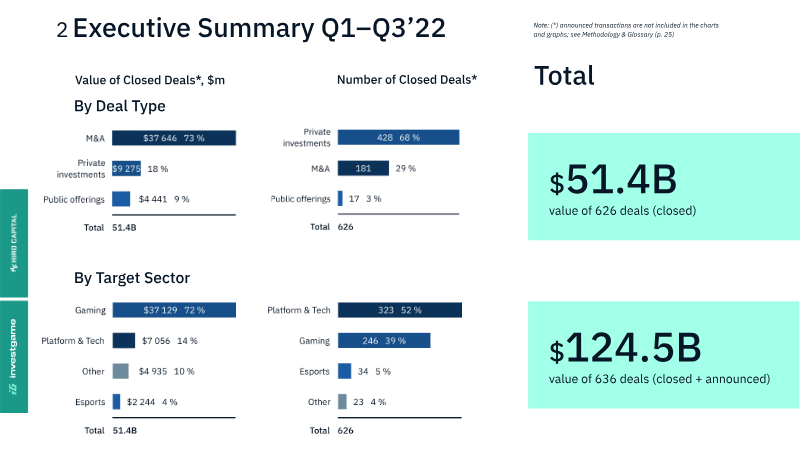

The gaming investment landscape in the first three quarters of 2022 reflects a significant market correction following a record-breaking 2021. While the total value of closed and announced deals reached $124.5 billion—nearly double the previous year's volume—this figure is heavily skewed by Microsoft’s pending $69 billion acquisition of Activision Blizzard. Excluding that single transaction, the market shows clear signs of cooling due to macroeconomic instability, post-pandemic shifts in user engagement, and increased regulatory scrutiny. Strategic mergers and acquisitions (M&A) remain the primary driver of deal value, reaching a record $101.4 billion year-to-date, despite a 40% decline in the number of closed transactions. Major players like Embracer Group, Sony, and Saudi Arabia’s Public Investment Fund (PIF) dominated this activity. Conversely, public offerings have nearly collapsed, reaching their lowest point since early 2020, with deal values shrinking fivefold compared to 2021. Private investments also saw a sharp decline in the third quarter, dropping 69% from the previous quarter, signaling that the "soured" economic climate has finally impacted venture capital and corporate rounds. The report highlights a notable shift in the blockchain and Web3 gaming sectors. While early-stage investment in this space previously drove market growth, the third quarter of 2022 marked the first period of negative growth for blockchain-related investments, with total deal value falling 14% year-over-year. Investors are becoming more selective, moving away from infrastructure platforms toward studios capable of producing engaging content. Geographically, the United States remains the most active market for gaming investments, followed by the United Kingdom and Turkey. Gender diversity remains a challenge for the industry, as 89% of companies receiving investment are male-led, with women-led entities representing only 2% of the total.

InvestGameJan 2022

Report

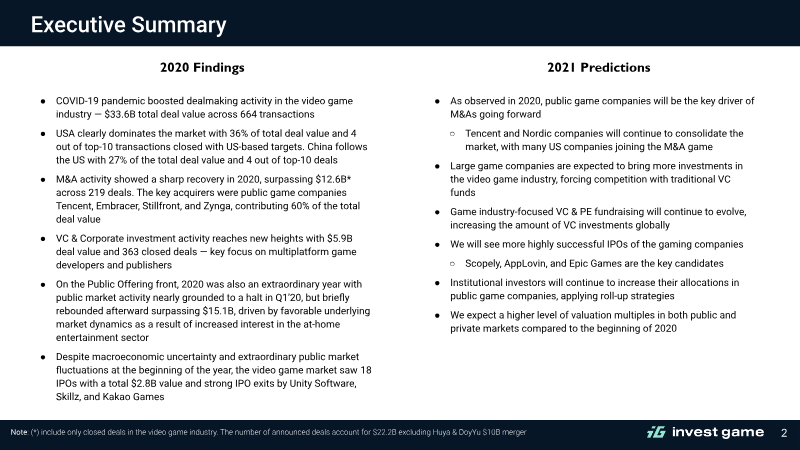

Global Video Game Deals Report 2020

The 2020 fiscal year marked a historic period of consolidation and capital infusion for the global video game industry, largely catalyzed by the COVID-19 pandemic and the resulting surge in at-home entertainment. Total deal value reached $33.6 billion across 664 transactions, encompassing mergers and acquisitions, private investments, and public offerings. The United States and China emerged as the primary geographical drivers, collectively representing 63% of the total deal value. The market demonstrated significant resilience, recovering from a stagnant first quarter to reach record-breaking activity levels in the second half of the year. M&A activity was a primary pillar of this growth, totaling $12.6 billion across 219 deals. This sector was dominated by public strategic acquirers such as Tencent, Embracer Group, Stillfront, and Zynga, who accounted for 60% of the total M&A value. Private investment also reached new heights, with $5.9 billion raised through venture capital and corporate rounds, specifically targeting multiplatform developers and mobile studios. Public markets followed a similar trajectory; after a quiet start to the year, public offerings surpassed $15.1 billion, supported by high-profile IPOs from companies like Unity Software and Kakao Games, as well as significant fixed-income activity as firms moved to refinance debt at lower interest rates. The analysis segments the industry into gaming, platform technology, and esports. While gaming remained the most active sector, platform and tech saw substantial late-stage investments in companies like Roblox and Epic Games. Looking forward, the industry is expected to see continued consolidation led by Nordic and Chinese firms, increased competition between traditional venture capital and large strategic investors, and a robust pipeline of IPO candidates. This data was compiled by tracking closed transactions across public media and financial databases, excluding pure gambling and betting entities to focus on the core video game ecosystem.

InvestGameJan 2020

Financial

Gaming Deals Activity Report Q1‑Q3'22

The analysis tracks deal activity across the global gaming ecosystem during the first three quarters of 2022, quantifying both merger‑and‑acquisition (M&A) and venture‑capital trends to assess how regulatory shifts and macro‑economic conditions reshaped investment patterns. A total of 626 transactions closed, generating $51.4 billion in value—a 31 percent rise over the same period in 2021—yet the quarterly count of deals contracted sharply, falling from 80 in Q1 to 55 by Q3. This contraction is attributed to heightened regulatory scrutiny, the fallout from the IDFA privacy changes, and a broader slowdown in economic confidence. M&A activity remained the dominant driver, accounting for roughly 73 percent of total deal value, with gaming‑specific mergers representing 72 percent of that share, underscoring the sector’s preference for consolidation over organic growth. In contrast, venture investment slipped 25 percent year‑over‑year, reflecting investor caution amid the same external pressures. Within the venture segment, crypto‑gaming emerged as a distinct outlier: Series A rounds averaged $40 million, markedly above the $25 million average across all gaming deals, highlighted by sizable raises such as Jot Art’s $55 million, Iskra’s $34 million, and Planetarium Labs’ $32 million. Overall, the period illustrates a market in transition, where large‑scale M&A continues to capture the bulk of capital while emerging niches like crypto‑gaming attract disproportionately high funding despite a general retreat in venture activity. The findings suggest that future deal flow will likely hinge on regulatory clarity and the ability of niche segments to sustain investor enthusiasm in a constrained macro environment.

InvestGameSept 2022