FinancialGames Workshop Group

Half-Yearly Report: 27 November 2016

23 Jan 201715 pages~38 min full read

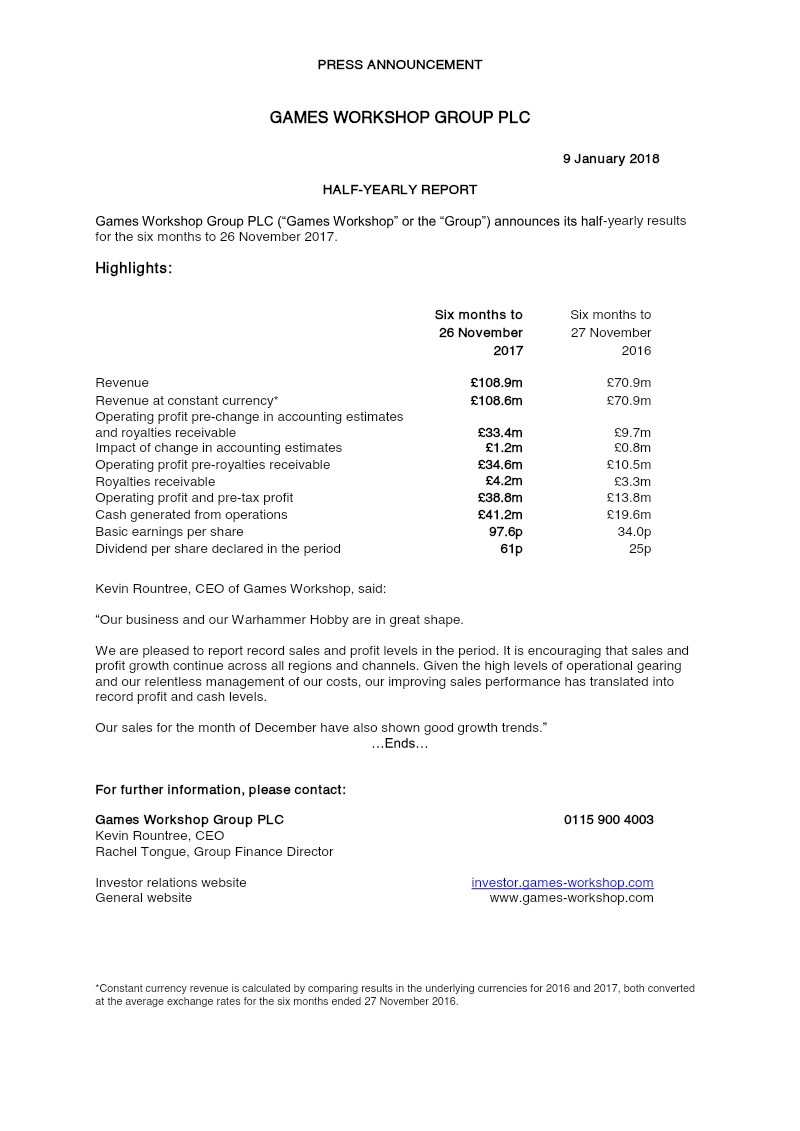

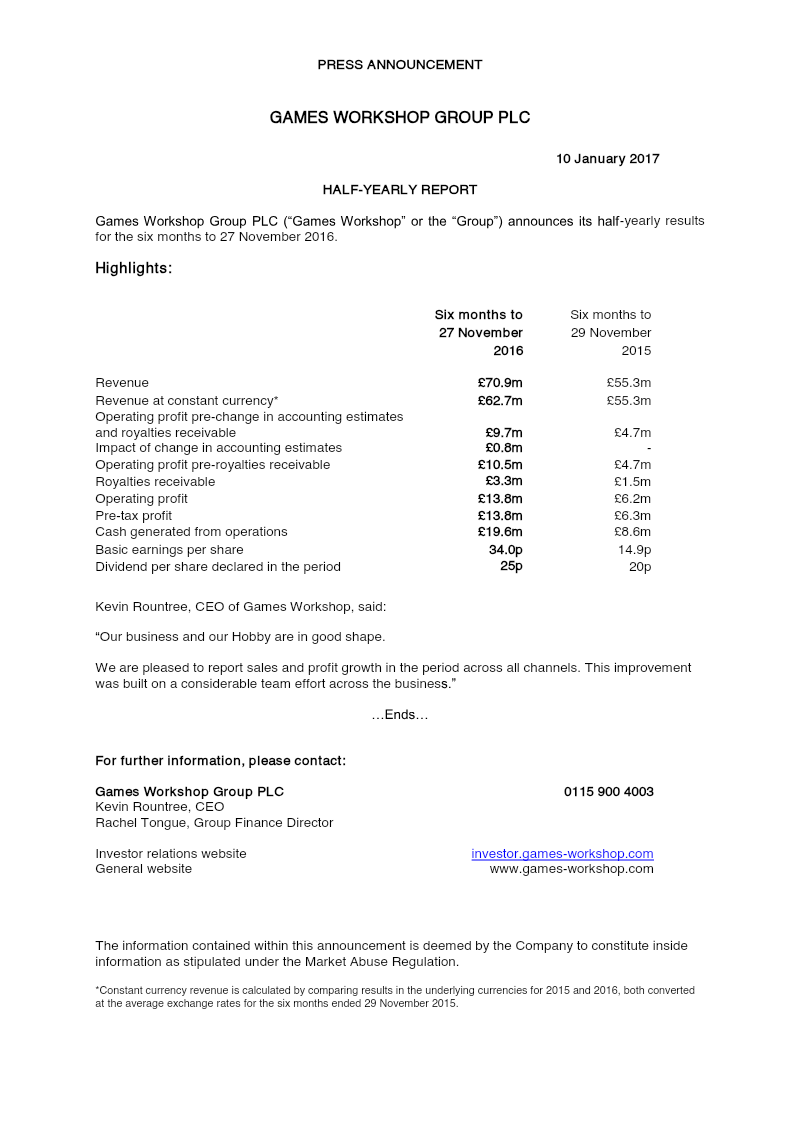

Games Workshop reported a 28% revenue increase to £70.9 million and more than doubled pre-tax profit to £13.8 million for the six months ending November 27, 2016.

Royalties receivable surged by 120% to £3.3 million, serving as a primary driver for the company's increased profitability.

The company generated £19.6 million in operational cash, facilitating a dividend payment of 25p per share and £6.8 million in capital investments.

Strategic accounting adjustments to the amortization of development costs and depreciation of moulding tools added £0.8 million to the operating profit.

Basic earnings per share rose to 34.0p, supported by a 40% return on capital and a healthy net cash position.

Growth was broad-based across all primary sales channels, including Retail, Trade, and Mail Order.

Games Workshop achieved substantial financial growth during the six months ending November 27, 2016, characterized by a 28% increase in revenue to £70.9 million and a more than doubling of pre-tax profit to £13.8 million. This performance reflects broad-based success across all primary sales channels, including Retail, Trade, and Mail Order. A significant driver of this profitability was a 120% surge in royalties receivable, which reached £3.3 million, alongside a robust return on capital of 40%. The period was marked by strong operational cash generation of £19.6 million, allowing for increased dividend payments of 25p per share and continued investment in the business.

The financial results were further bolstered by strategic adjustments to accounting estimates regarding the amortization of development costs and the depreciation of moulding tools. These changes, designed to better align expenditures with product revenue cycles, contributed an additional £0.8 million to the operating profit. Consequently, basic earnings per share rose to 34.0p, up from the previous year’s performance. The Group’s net cash position remained healthy, supporting £8.0 million in dividend distributions and £6.8 million in capital investments.

The overall trajectory indicates a period of high operational efficiency and market expansion for the tabletop gaming manufacturer. By leveraging strong performance in the Trade and Royalties segments, the company successfully translated increased external revenue into significant bottom-line growth. This fiscal period demonstrates a successful alignment of product development cycles with financial reporting, ensuring that the Group maintains a high level of liquidity while rewarding shareholders through consistent capital returns.