FinancialSega Sammy Holdings

Financial Results for Q3 of the Fiscal Year Ending March 2026: Major Questions in Results Briefing

5 pages~12 min full read

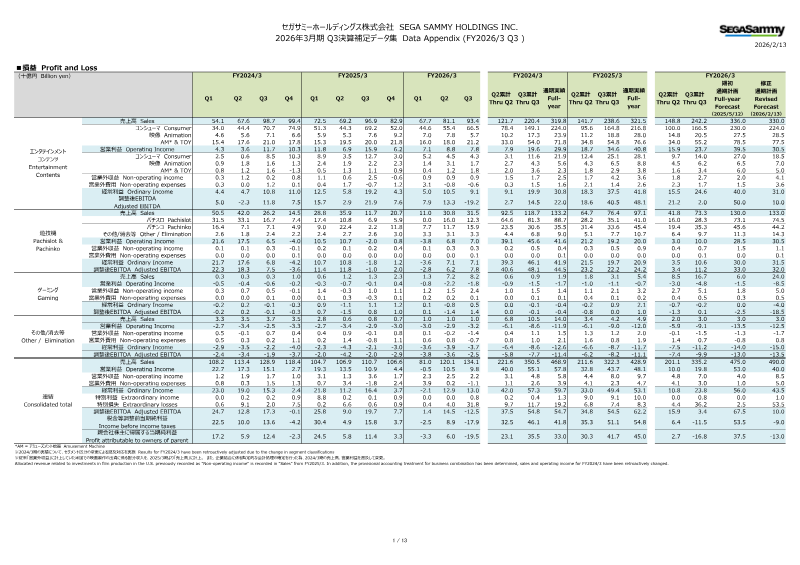

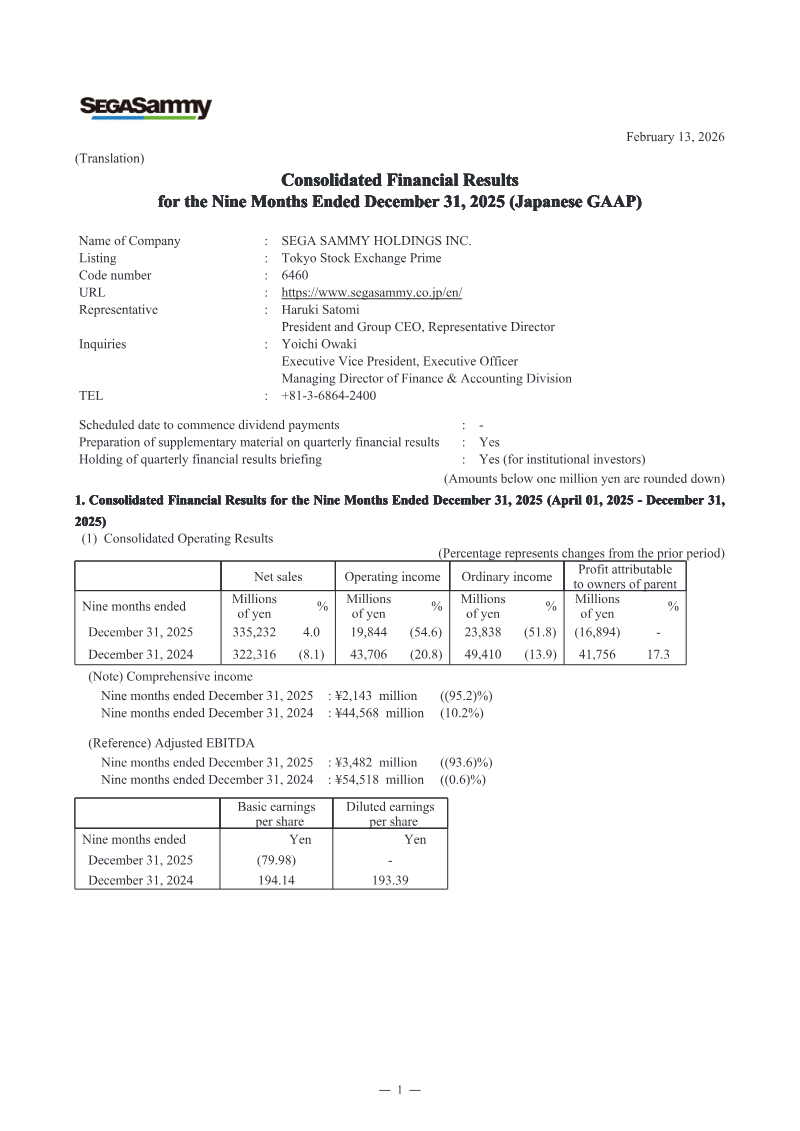

Sega Sammy Holdings’ third-quarter financial results briefing for the fiscal year ending March 2026 outlines a strategic shift toward improved capital efficiency and a more unified global marketing structure. Facing a net debt position and performance shortfalls in certain segments, management is prioritizing the optimization of existing assets over large-scale mergers and acquisitions. The company intends to refine its capital allocation policy in the upcoming medium-term plan, focusing on businesses where it can leverage core strengths to ensure sustainable growth.

In the Entertainment Contents segment, the company is addressing challenges in its consumer business by transitioning from a region-specific publishing model to a centralized, data-driven global strategy. While the acquisition of Rovio’s "Beacon" system has not yet yielded the expected results due to operational differences between casual and core mobile titles, the company remains committed to maximizing the value of its intellectual property. Future growth is anchored by a robust pipeline of major titles scheduled for the fiscal year ending March 2027, alongside a transmedia strategy that leverages the Sonic the Hedgehog film franchise to drive licensing and merchandise revenue.

The Pachislot and Pachinko business continues to serve as a stable earnings pillar, with the company maintaining flexible pricing strategies to navigate competitive pressures. Despite a downward revision in unit sales volume, high demand for mainstay titles has allowed the company to remain on track with its profit forecasts. Meanwhile, the Gaming business is focused on integrating recent acquisitions, such as GAN and Stakelogic, to expand recurring revenue through platform migration and content development. Management has clarified that it will not pursue large-scale investments in domestic integrated resorts, preferring instead to offer operational expertise and equipment supply if opportunities arise.

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2024

Sega Sammy Holdings · 2024

Sega Sammy Holdings

Sega Sammy Holdings

Sega Sammy Holdings

Sony Group Corporation · 2026

Bandai Namco · 2026

InvestGame · 2025

Square Enix · 2025

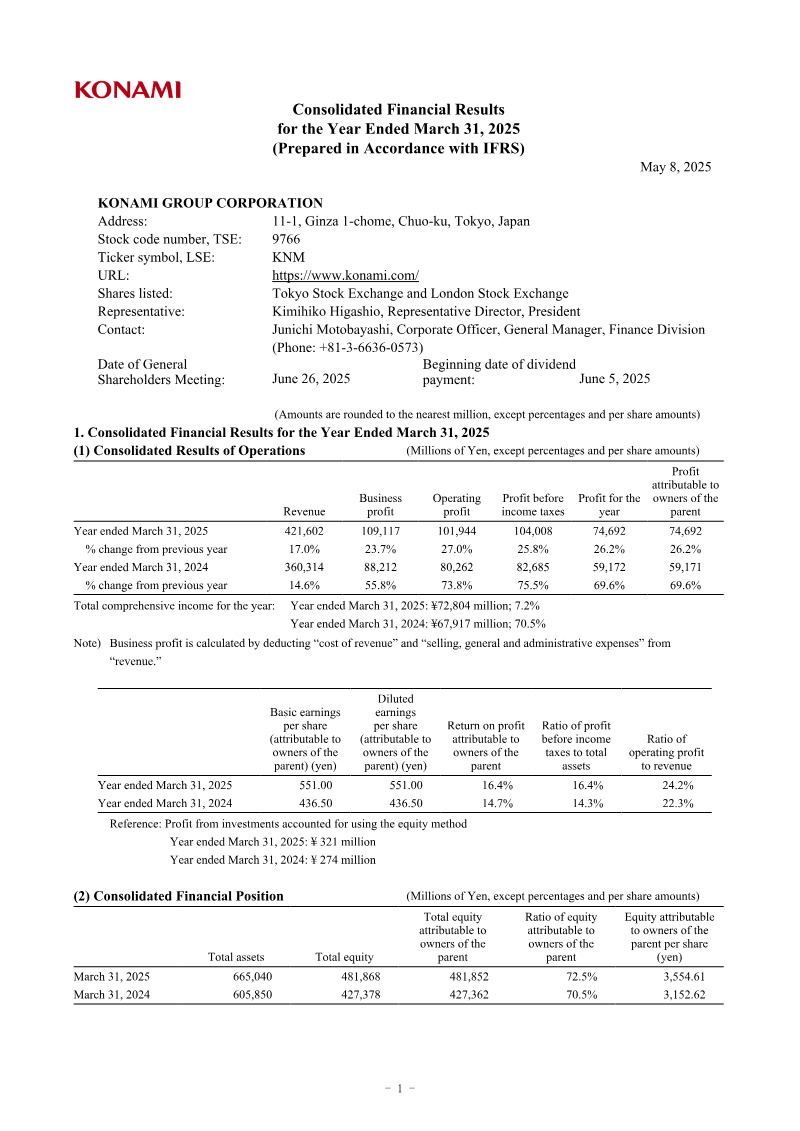

Konami · 2025

Nintendo · 2024

Bandai Namco · 2022

Bandai Namco · 2021

GREE · 2017

Bandai Namco · 2017

GREE Inc. · 2016

Bandai Namco · 2014