FinancialCyberAgent

FY2023 Consolidated Financial Results [Japanese GAAP]

1 Nov 202317 pages~31 min full read

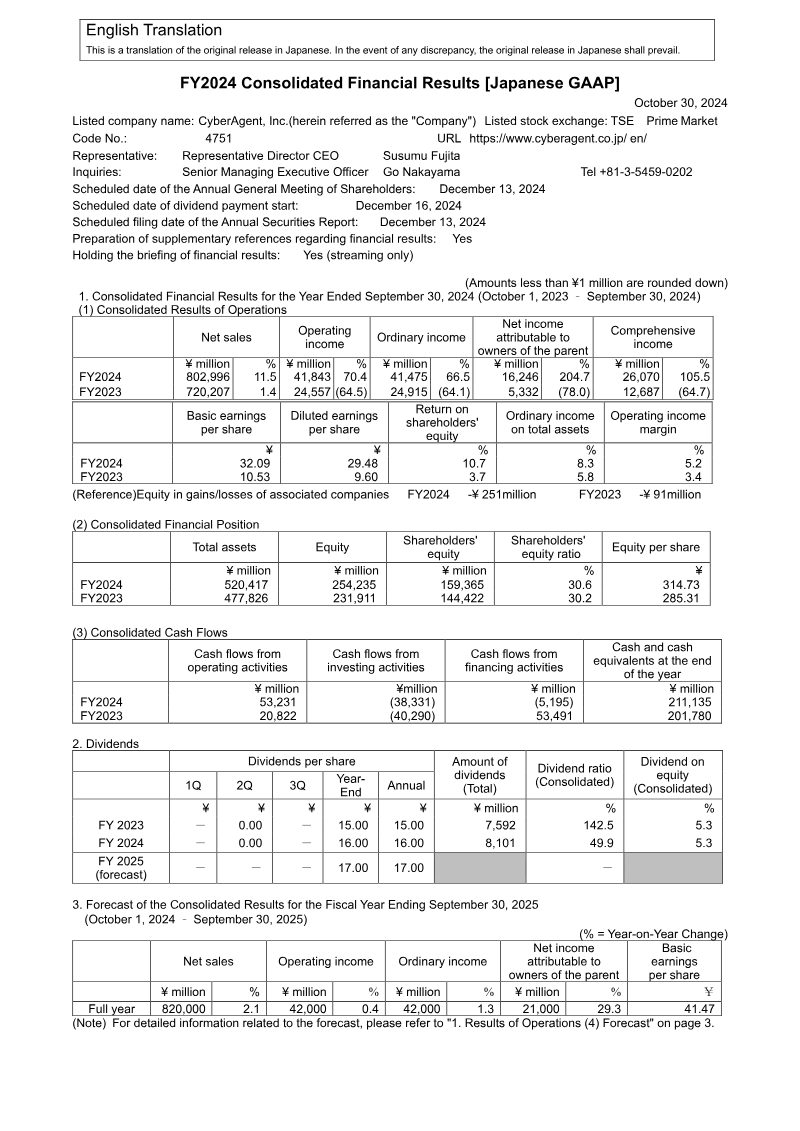

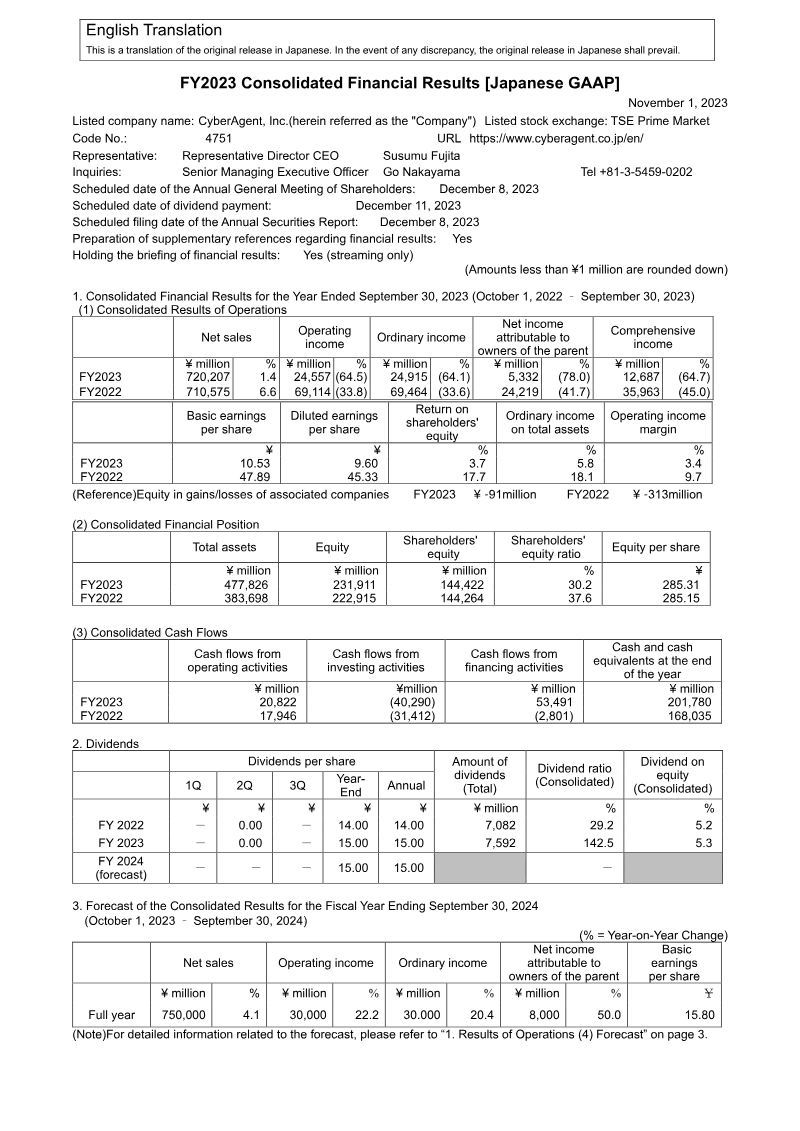

CyberAgent's FY2023 operating income fell 64.5% to ¥24,557 million, primarily due to a 62.5% profit decline in the Game Business caused by the lifecycle maturity of key titles.

See it on page 4Consolidated net sales grew by 1.4% to ¥720,207 million, while net income attributable to owners dropped significantly from ¥24,219 million to ¥5,332 million.

See it on page 1The Media Business, led by the ABEMA platform, achieved a 25.9% increase in segment sales and successfully reduced operational deficits.

See it on page 4The Internet Advertisement segment remains the company's largest revenue contributor at ¥381,206 million, though margins were compressed by upfront AI investments.

See it on page 4The company bolstered its liquidity to ¥201,780 million in cash and equivalents through ¥53 billion in financing activities, including convertible bonds and long-term loans.

See it on page 4Management projects a recovery in FY2024, forecasting a 22.2% rebound in operating income and a 50% increase in net income driven by new game releases and Media segment scaling.

See it on page 5CyberAgent maintains a highly localized business model, with over 90% of its total sales and assets concentrated within the Japanese market.

See it on page 15CyberAgent, Inc. experienced a period of significant transition during the 2023 fiscal year, characterized by modest revenue growth alongside a sharp contraction in profitability. Consolidated net sales reached ¥720,207 million, representing a 1.4% year-over-year increase, yet operating income plummeted by 64.5% to ¥24,557 million. This decline was primarily driven by the Game Business, where profits fell 62.5% due to the natural lifecycle decline of high-margin titles. Simultaneously, the Internet Advertisement segment, while remaining the largest revenue contributor at ¥381,206 million, faced margin pressure from upfront investments in artificial intelligence.

The Media Business emerged as a growth engine, with the ABEMA platform driving a 25.9% increase in segment sales and successfully narrowing its operational deficits. Despite the drop in net income attributable to owners—which fell from ¥24,219 million to ¥5,332 million—the company significantly strengthened its liquidity position. Cash and cash equivalents rose to ¥201,780 million, bolstered by over ¥53 billion in financing activities, including the issuance of convertible bonds and the acquisition of long-term bank loans. These strategic financial moves ensure a stable capital base for future expansion within the predominantly Japanese market, where over 90% of sales and assets are concentrated.

Projections for the 2024 fiscal year indicate a strategic pivot toward recovery and renewed growth. Management forecasts net sales to reach ¥750 billion, supported by a pipeline of new game releases and the continued scaling of the Media segment. Operating income is expected to rebound by 22.2%, while net income is projected to increase by 50%. This outlook suggests that the heavy investment phase and the volatility in the gaming portfolio observed in 2023 are expected to stabilize, allowing for improved earnings per share and a more balanced contribution across the advertising, gaming, and media divisions.