ReportKoei Tecmo

Financial Highlights: 1st Half of the Fiscal Year Ending March 2018

2 pages~3 min full read

Key insights

6 takeaways · ~2 min read- 01

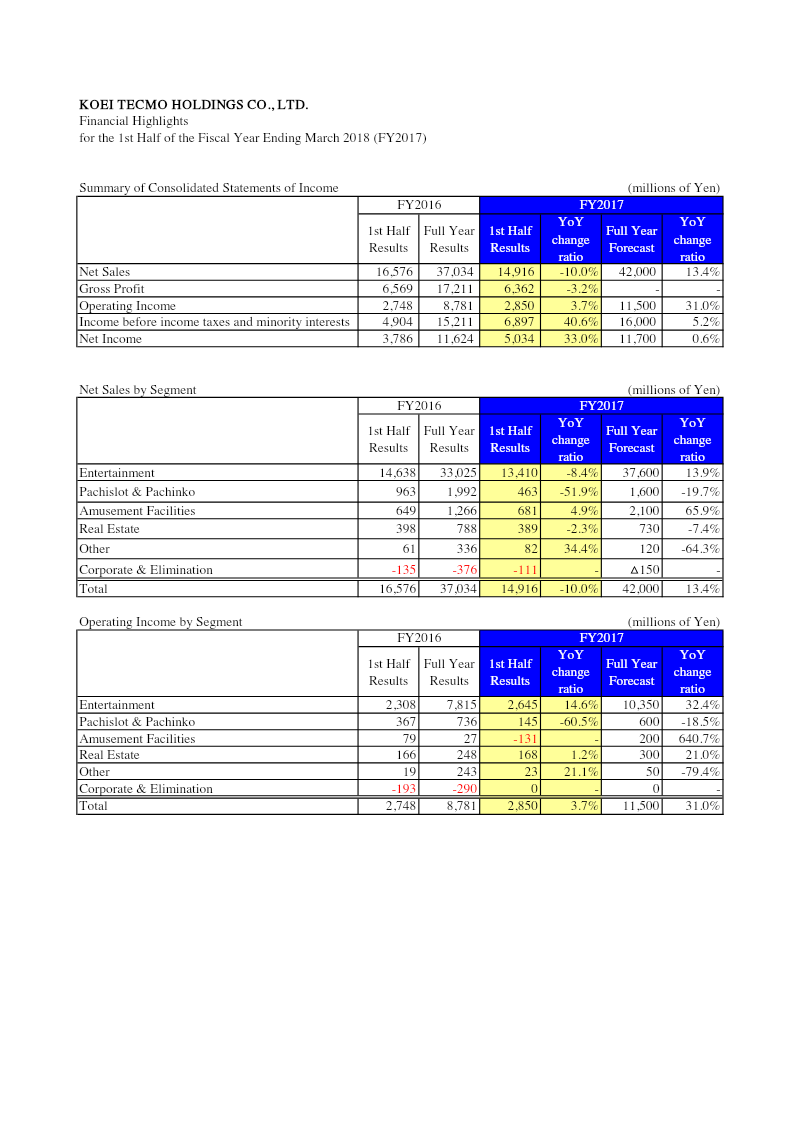

Koei Tecmo Holdings reported a 33.0% increase in net income to ¥3,786 million for the first half of FY2018, despite a 10% decline in net sales to ¥16,576 million.

See it on page 1 - 02

Operating income rose 31% to ¥2,748 million, driven by a 32.4% increase in operating income within the Entertainment segment and a 21.0% rise in the Real Estate segment.

See it on page 1 - 03

The company's top-line revenue decline was primarily caused by a 51.9% drop in Pachislot & Pachinko revenue and a 64.3% decline in the Other segment.

See it on page 1 - 04

Cash and time deposits decreased significantly from ¥11,868 million to ¥5,062 million as of September 30, 2017.

See it on page 2 - 05

Current liabilities fell sharply to ¥6,530 million from ¥11,460 million, while long-term liabilities increased to ¥2,543 million due to higher deferred tax liabilities.

See it on page 2 - 06

Shareholders' equity remained stable at ¥105.6 billion, and total assets saw a minor decline to ¥119.5 billion compared to the previous year.

See it on page 2