Related Documents

Financial

FY26/3 Earnings Summary and Mid- to Long-Term Growth Strategies: Capcom

Capcom achieved a historic peak in FY26/3, reporting net sales of ¥1.95 billion and operating profit of ¥752 million—both up 15% year‑over‑year. The surge was driven by strong new‑title releases and catalog sales, particularly through digital channels, and marked the company’s highest cumulative unit sales at 5.9 million. Retail expansion reached 61 stores, including the first overseas Capcom Store in Taipei, underscoring a growing global footprint. Looking ahead to FY27/3, Capcom targets more than 10% operating‑profit growth and ¥2.1 billion in sales, underpinned by a steady pipeline of new IP launches such as *Pragma* and an expanded catalog strategy. The company plans to release one new machine per quarter, aiming for 53 000 units across four titles—including Biohazard RE:3 and Resident Evil 7—while projecting net sales of ¥209 million and operating profit of ¥104 million. A key focus is deepening IP monetisation through e‑sports, media tie‑ins, and mobile extensions, with an expected 18% year‑over‑year increase in pachislo volume and intensified expansion into emerging markets. The FY26/3 earnings report also highlights significant workforce growth, with an annual addition of over 100 developers and the integration of AI tools to enhance efficiency. Financially, net sales rose 14% YoY to ¥1,259 bn and operating profit increased 18% to ¥508 bn, while maintaining a strong cash position that balances shareholder returns, employee compensation, and reinvestment. Diversity metrics improved, with female core‑role representation at 15.7% and paternity leave utilization at 79.7%, reflecting a broader talent strategy aimed at sustaining long‑term innovation and market leadership.

CapcomMay 2026

Financial

Fiscal Year Ended March 2026: Results Presentation

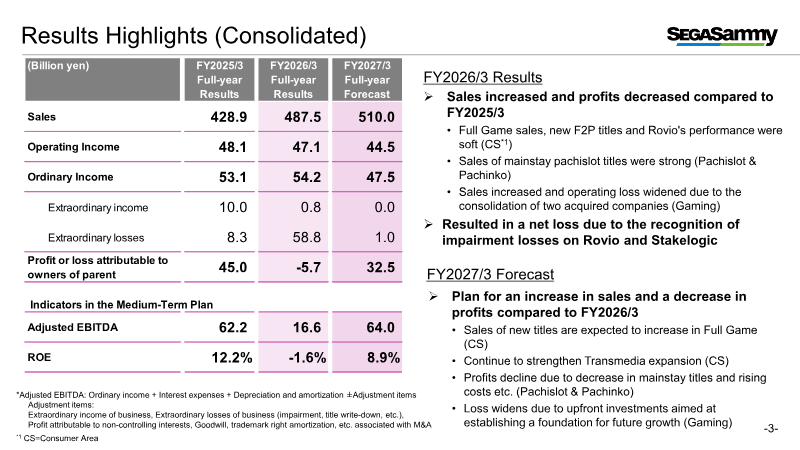

Fiscal year 2026 ended with a 13 % rise in sales to ¥487.5 bn, yet operating income swung from a ¥48.1 bn profit in FY2025 to a ¥5.7 bn loss, driven by significant goodwill impairments on Rovio and Stakelogic and a widening deficit in the Gaming segment. Adjusted EBITDA fell to ¥16.6 bn, reflecting heavy upfront development costs and impairment charges, while net equity contracted by ¥48.7 bn as cash balances were depleted following the acquisitions of GAN and Stakelogic. Within Entertainment Contents, sales edged up to ¥326.6 bn from ¥321.5 bn, but operating income declined from ¥40.8 bn to ¥32.4 bn because new Full‑Game and F2P titles underperformed, despite steady growth in licensing revenue. Forecasts for FY2027 project sales of ¥357 bn and operating income of ¥42.5 bn, contingent on successful new IP launches, repeat sales, and a planned lift in licensing income. Margin erosion from title underperformance remains a key risk. Capital allocation for FY2026/3 was restructured to focus on ¥190 bn of cumulative investment over FY2025–FY2027, allocating ¥80 bn to development, ¥120 bn to strategic acquisitions, and planning ¥70 bn in share buybacks while pausing large‑scale M&A. Shareholder returns are expected to rise sharply, with FY2026/3 projected at ¥31.5 bn (≈¥11.7 bn in dividends) and FY2027/3 potentially reaching ¥16.2 bn under a 50 % total‑return ratio applied to projected net income. Pachislot sales showed modest growth, buoyed by new titles and strong first‑week performance of flagship IPs such as “Hokuto No Ken” and “Kabaneri of the Iron Fortress.” Pachinko sales declined as the temporary lift from Lucky Trigger 3.0 Plus faded and hall utilization softened. The group plans to introduce reel‑exchangeable cabinets, expected to account for roughly 20 % of pachislot revenue, and is positioning the gaming business for a J‑curve bottom in FY2027 through intensive lease sales and B2B platform upgrades. The release schedule for FY2026/3 emphasizes a concentrated push of multi‑platform titles, including the Nintendo Switch 2 launch in March 2026 and a slate of global releases across consoles, PC, and mobile from late 2025 to mid‑2026. Key animation properties such as *Detective Conan* and *Lupin the Third* are slated for April–June 2025, with several new IPs and Netflix exclusives planned for early 2026. Pachislot and pachinko product launches are detailed with projected unit sales ranging from 8,000 to 49,000 units across varying gambling‑specification tiers.

SegaSammyMay 2026

Financial

FY2025 Consolidated Financial Results

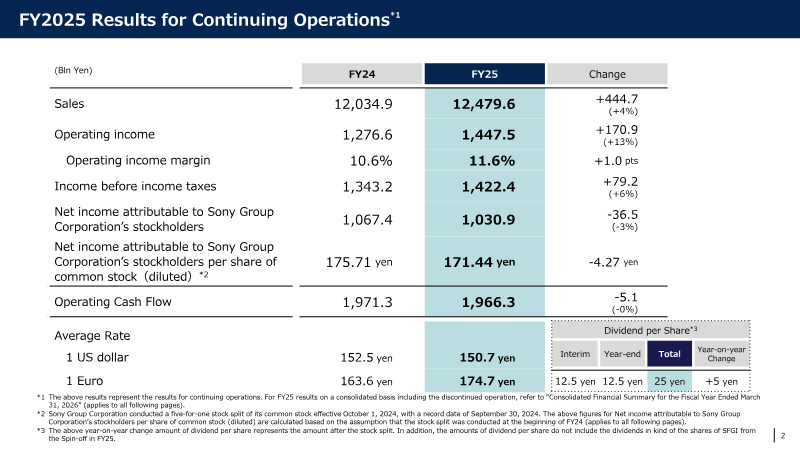

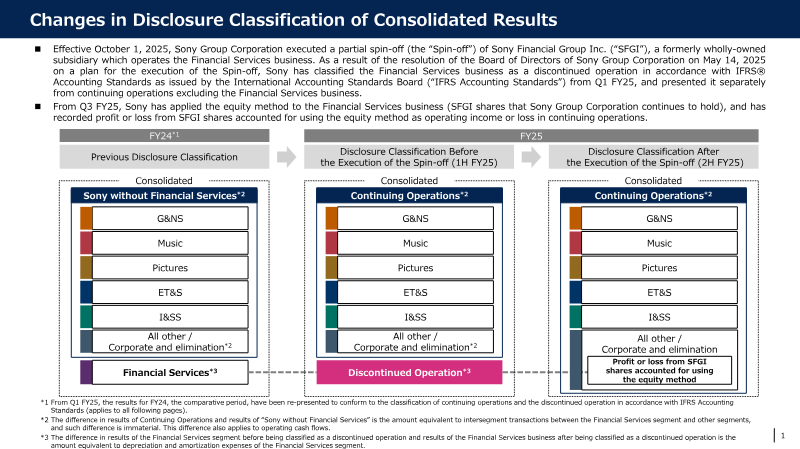

Sony Group’s FY2025 consolidated results demonstrate modest revenue growth and a mixed profitability profile across its core business units. Total sales increased 4 % to ¥12.48 trn, largely driven by higher operating income in the Imaging & Sensing Solutions (I&SS) and Music segments. Operating income rose 13 % to ¥1.45 trn, while net income attributable to shareholders fell 3 % to ¥1.03 trn because of a larger equity‑method loss in the Financial Services arm and higher impairment charges. Operating cash flow remained flat at ¥1.97 trn, and the spin‑off of Sony Financial Group was treated as a discontinued operation from Q1 FY25 onward. Within the Music division, sales climbed 15 % to ¥277.5 billion, propelled by growth in Recorded Music and Music Publishing streaming revenues (+9 % and +14 % respectively), live‑event income, and a strong contribution from the Demon Slayer franchise. Operating income in this segment surged 25 % to ¥89.7 billion, reaching a record high even after excluding one‑time items. Sony projects flat sales for FY2026, with operating income expected to decline 11 % to ¥47 billion as streaming gains are offset by the loss of Demon Slayer’s impact. The company consolidates its Pictures and Music results on a U.S. dollar basis, translating foreign‑currency sales and costs using weighted average exchange rates while accounting for hedging transactions. Foreign‑exchange fluctuations affect both sales and operating income, with I&SS hedging gains or losses incorporated into these calculations. These disclosures supplement, but do not replace, Sony’s IFRS‑compliant consolidated financial statements.

Sony Group CorporationMay 2026

Financial

Consolidated Financial Results: Fiscal Year Ended March 31, 2026

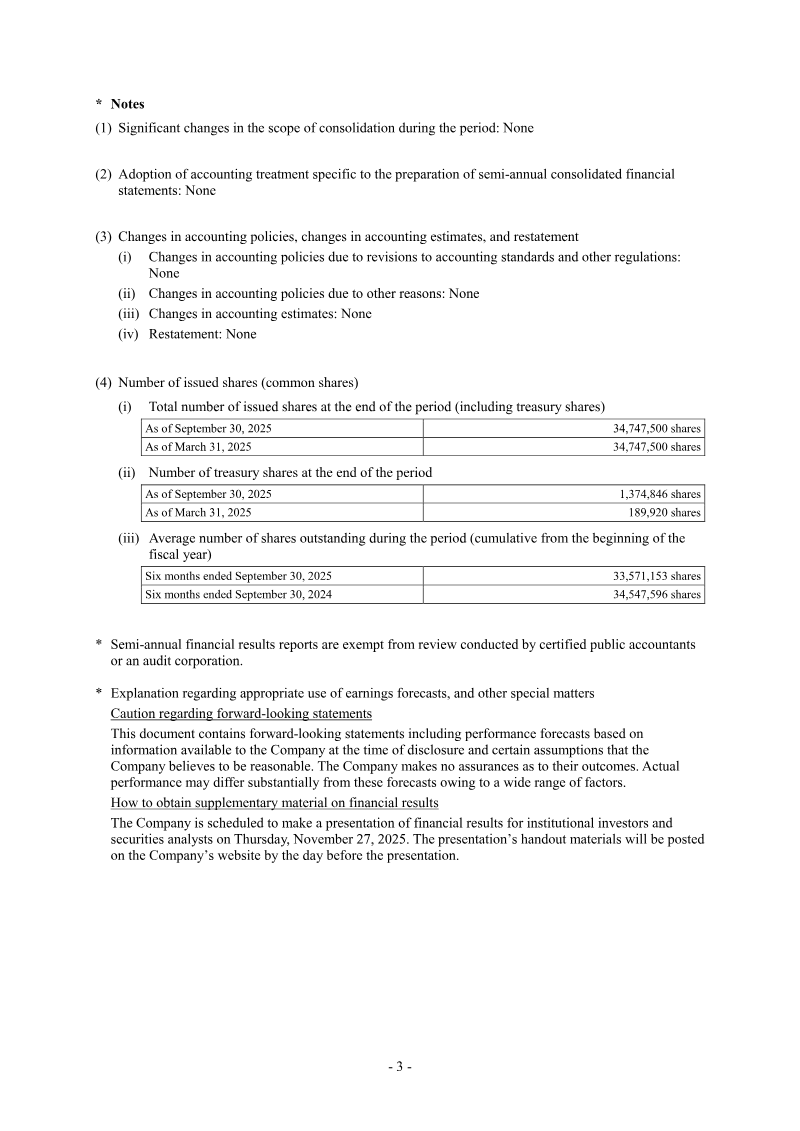

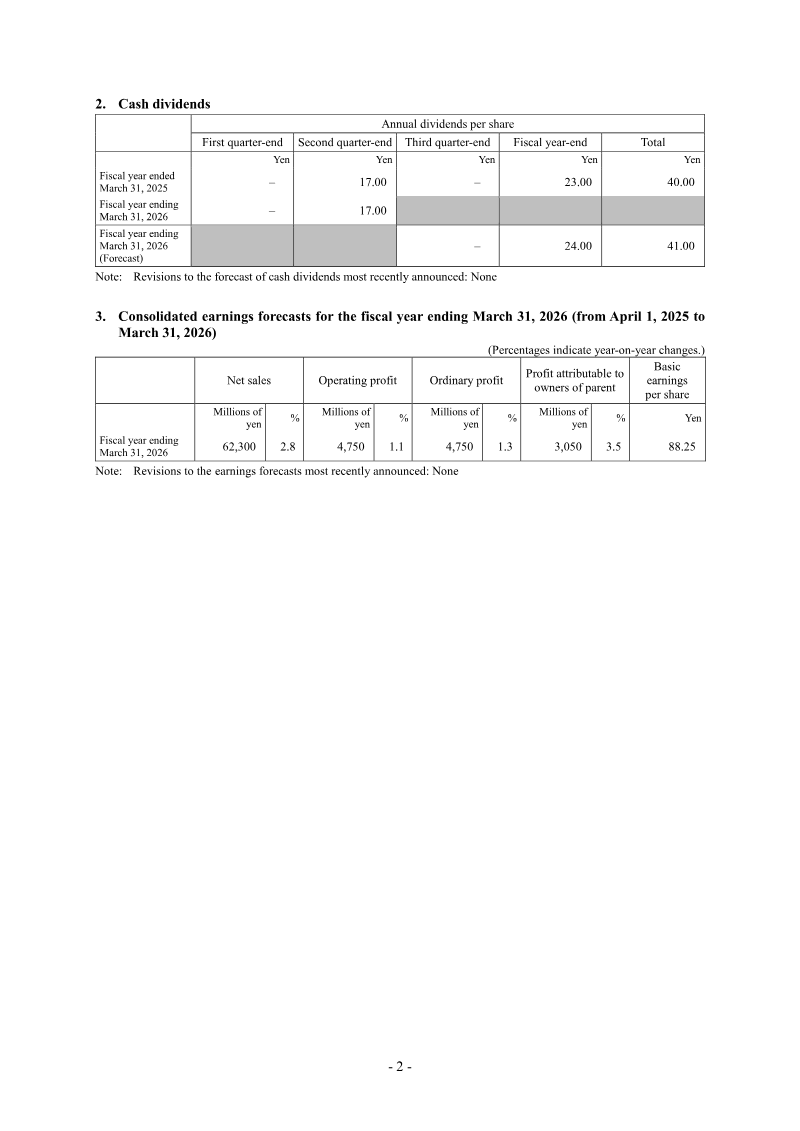

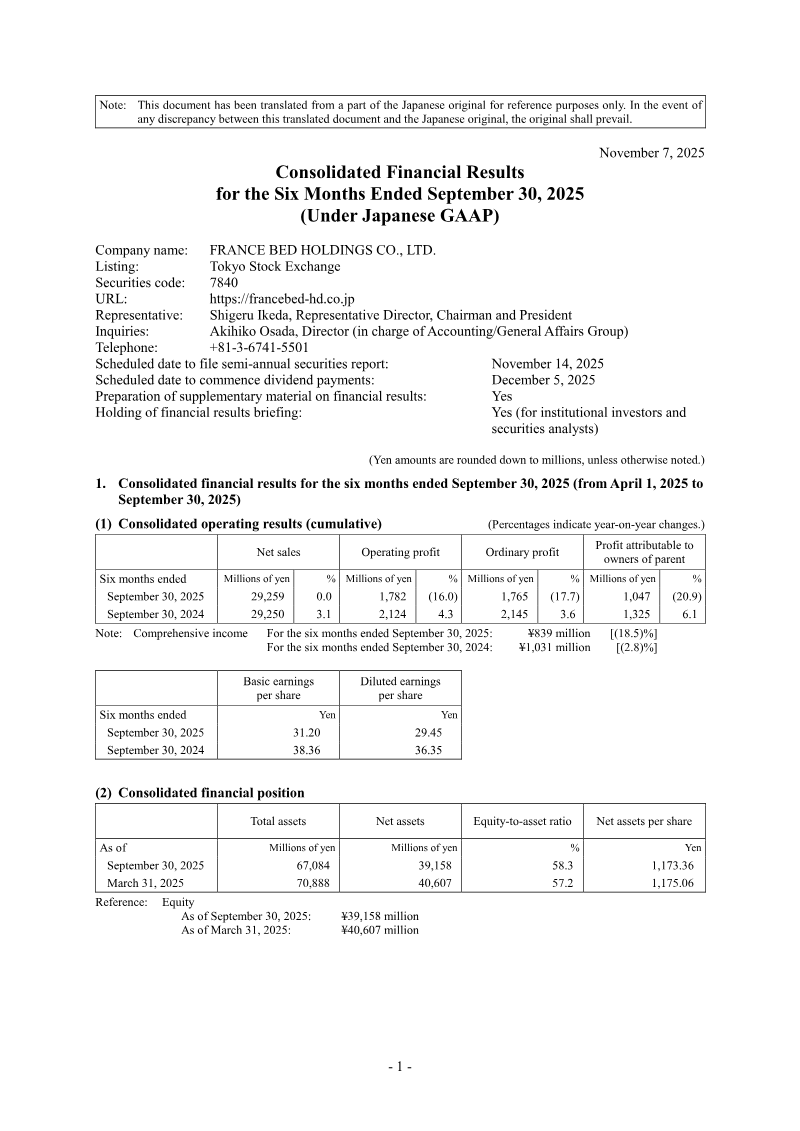

France Bed Holdings Co., Ltd. released its consolidated financial results for the six-month period ending September 30, 2025, prepared in accordance with Japanese GAAP. The report details the company’s operating performance, financial position, and cash flow status, while maintaining its previously announced earnings forecasts for the full fiscal year ending March 31, 2026. During the first half of the fiscal year, the company reported net sales of 29,259 million yen, remaining essentially flat compared to the same period in the previous year. However, profitability metrics experienced a decline, with operating profit falling 16.0% to 1,782 million yen and ordinary profit decreasing 17.7% to 1,765 million yen. Profit attributable to owners of the parent reached 1,047 million yen, representing a 20.9% year-on-year decline. Basic earnings per share for the period were 31.20 yen, down from 38.36 yen in the prior year. The company’s financial position as of September 30, 2025, shows total assets of 67,084 million yen and net assets of 39,158 million yen, resulting in an equity-to-asset ratio of 58.3%. Cash flows from operating activities provided 2,541 million yen, while investing and financing activities reflected ongoing capital allocation, including the purchase of treasury shares and continued investment in property, plant, and equipment. Looking ahead to the full fiscal year ending March 31, 2026, the company maintains its forecast of 62,300 million yen in net sales and 4,750 million yen in operating profit. These projections reflect a modest growth expectation of 2.8% in sales and 1.1% in operating profit compared to the previous fiscal year. The company continues to operate under stable accounting policies with no significant changes in the scope of consolidation.

FRANCE BED HOLDINGS CO.May 2026