Financialmixi

Consolidated Financial Results for the Fiscal Year Ended March 31, 2017

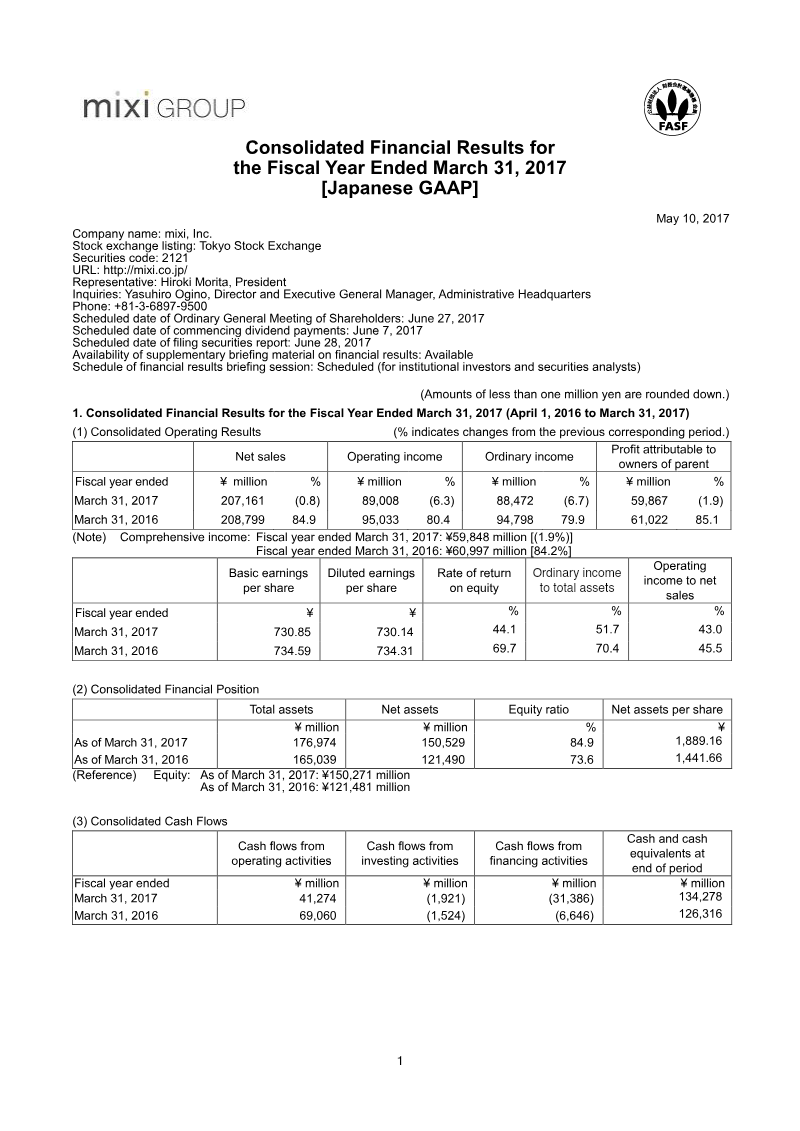

1 May 201722 pages~39 min full read

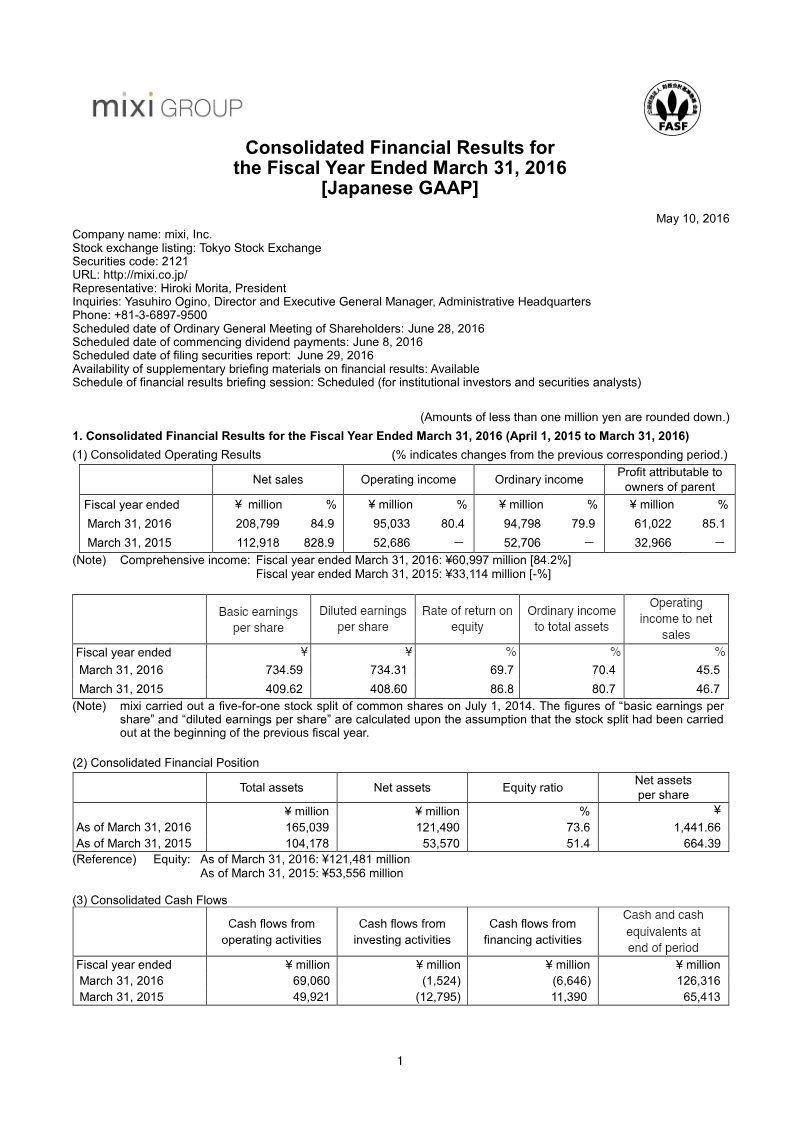

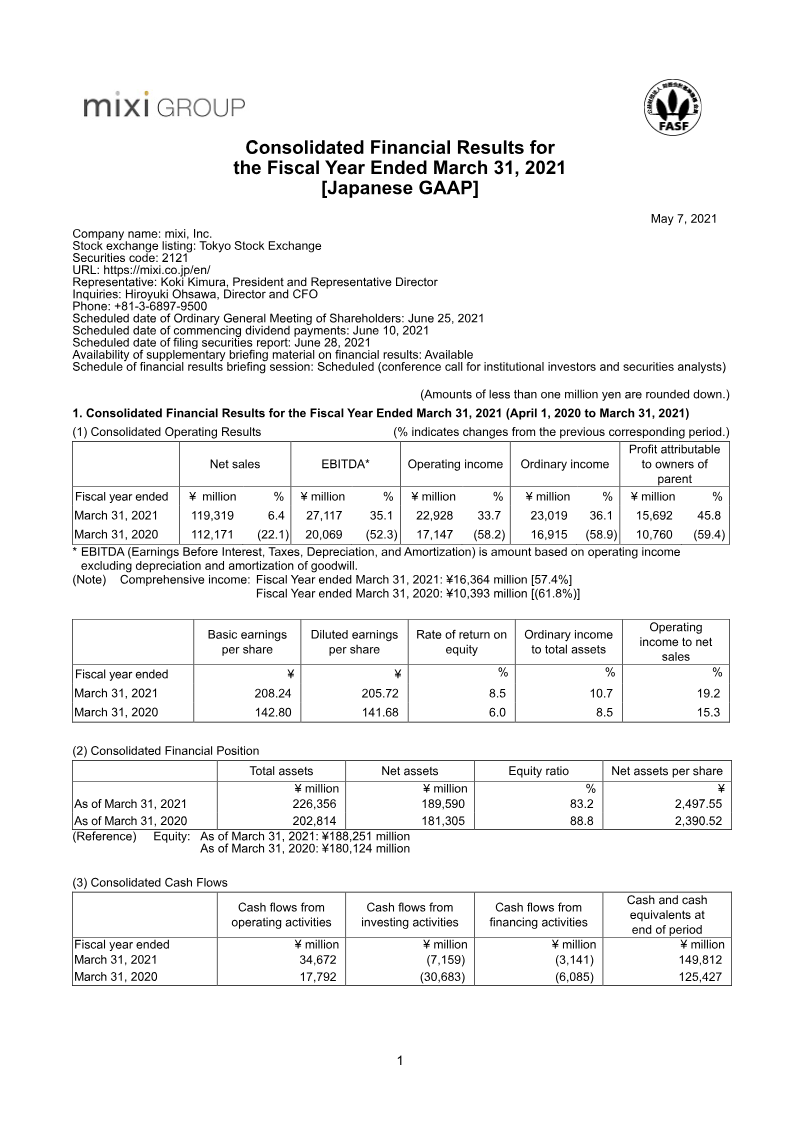

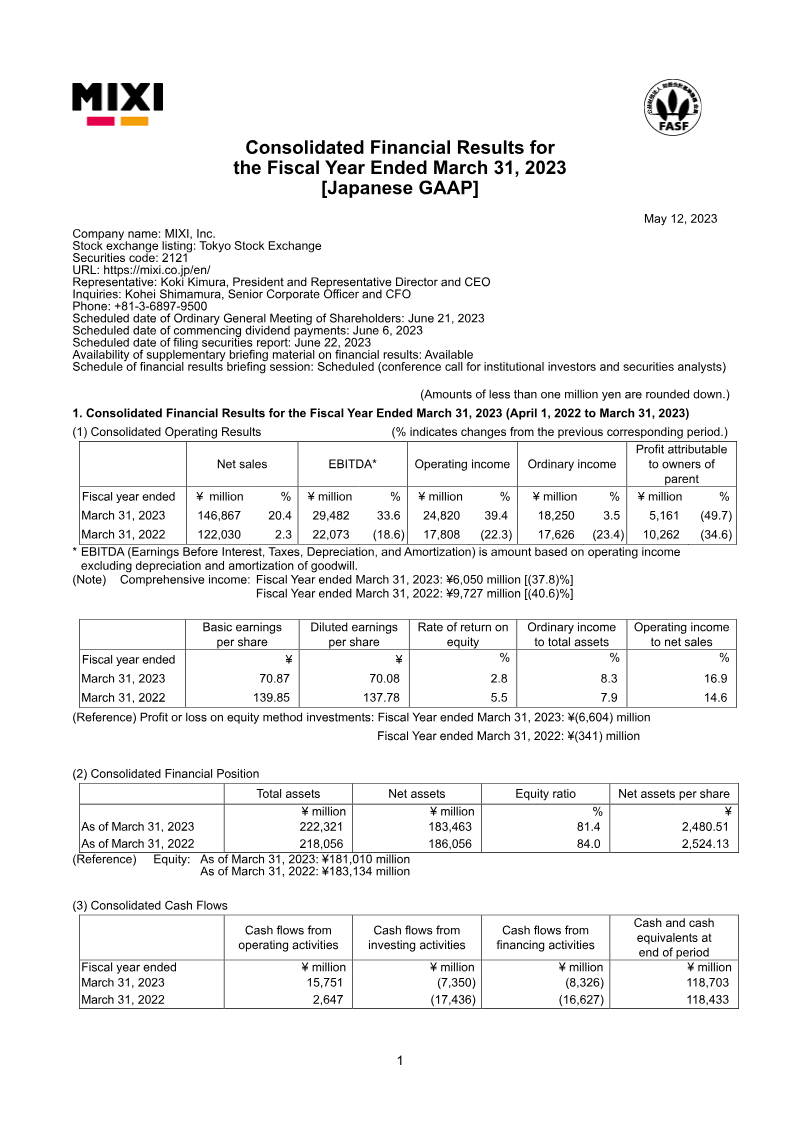

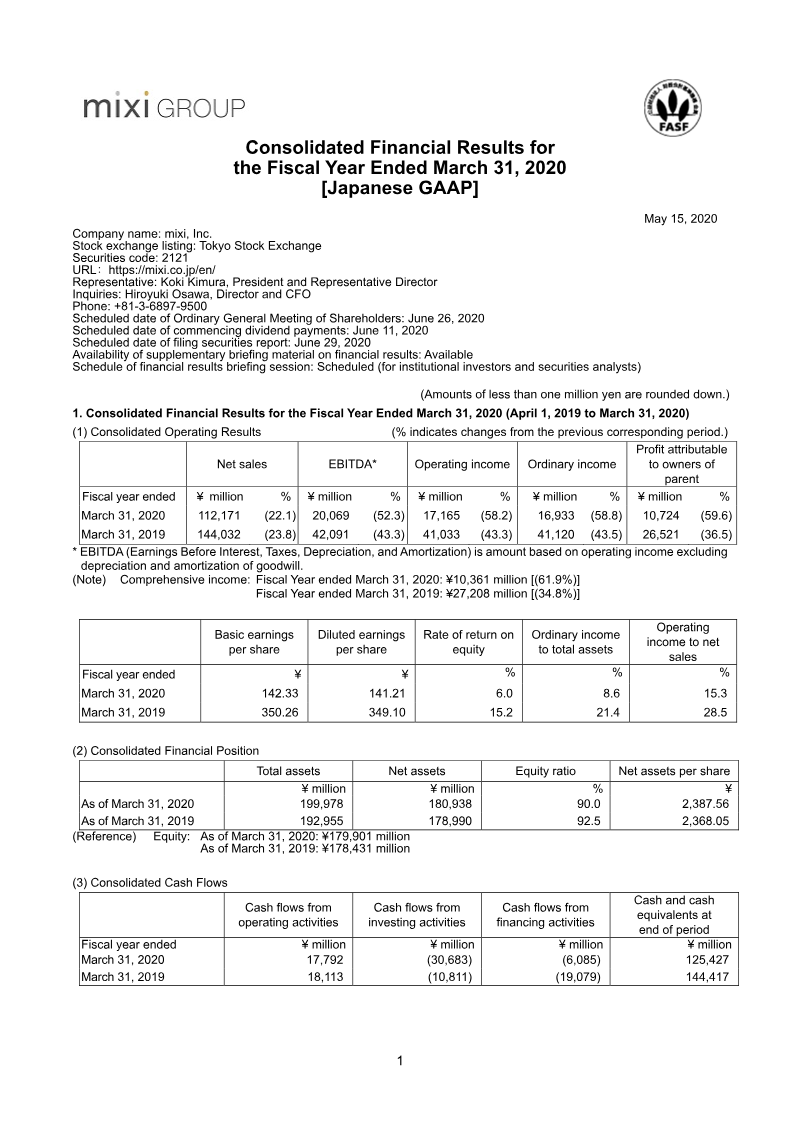

Mixi, Inc. reported fiscal year 2017 net sales of ¥207.1 billion and a profit of ¥59.8 billion, representing marginal year-over-year declines of 0.8% and 1.9%, respectively.

See it on page 1The company projects a downturn for the fiscal year ending March 2018, forecasting a 3.5% decrease in net sales and a 19.8% drop in profit.

See it on page 2The Entertainment Business remains the company's primary revenue driver, accounting for 93% of total sales and generating ¥89 billion in segment profit.

See it on page 18Despite cooling growth, the company maintains a strong financial position with an equity ratio of 84.9% and ¥134.2 billion in cash.

See it on page 1Management is prioritizing capital efficiency by retiring 2.4 million treasury shares and authorizing up to ¥10 billion in additional share buybacks for the upcoming year.

See it on page 22Strategic portfolio adjustments included the acquisition of Compath Me Inc. and the divestiture of non-core assets, specifically MUSE & Co., Ltd. and mixi research, Inc.

See it on page 22Mixi, Inc. concluded the fiscal year ending March 31, 2017, with a stable but slightly contracting financial performance, reporting net sales of ¥207.1 billion and a profit of ¥59.8 billion. These figures represent marginal year-over-year declines of 0.8% and 1.9%, respectively. Despite this cooling growth, the organization significantly bolstered its balance sheet, increasing its equity ratio to 84.9% and maintaining a robust cash position of ¥134.2 billion. This financial stability was achieved alongside strategic portfolio adjustments, including the acquisition of Compath Me Inc. and the divestiture of non-core assets such as MUSE & Co., Ltd. and mixi research, Inc.

The Entertainment Business remains the primary engine of the company, generating 93% of total revenue and contributing ¥89 billion in segment profit. To sustain this dominance, the organization increased advertising expenditures to ¥20.8 billion. Meanwhile, the Media Platform segment continues to manage significant goodwill assets totaling over ¥8.6 billion. Management has prioritized shareholder returns and capital efficiency through aggressive equity management, retiring 2.4 million treasury shares during the period and authorizing further buybacks of up to ¥10 billion for the following year.

The outlook for the fiscal year ending March 2018 suggests a period of transition and anticipated decline. Projections indicate a 3.5% decrease in net sales and a more substantial 19.8% drop in profit. This forecast reflects a cautious stance as the company navigates a maturing entertainment market and integrates its recent structural changes. While the current financial foundation remains exceptionally strong, the projected downturn highlights the challenges of maintaining the high-growth trajectory established in previous cycles.