Financialmixi

Consolidated Financial Results for the Fiscal Year Ended March 31, 2016

1 May 201646 pages~84 min full read

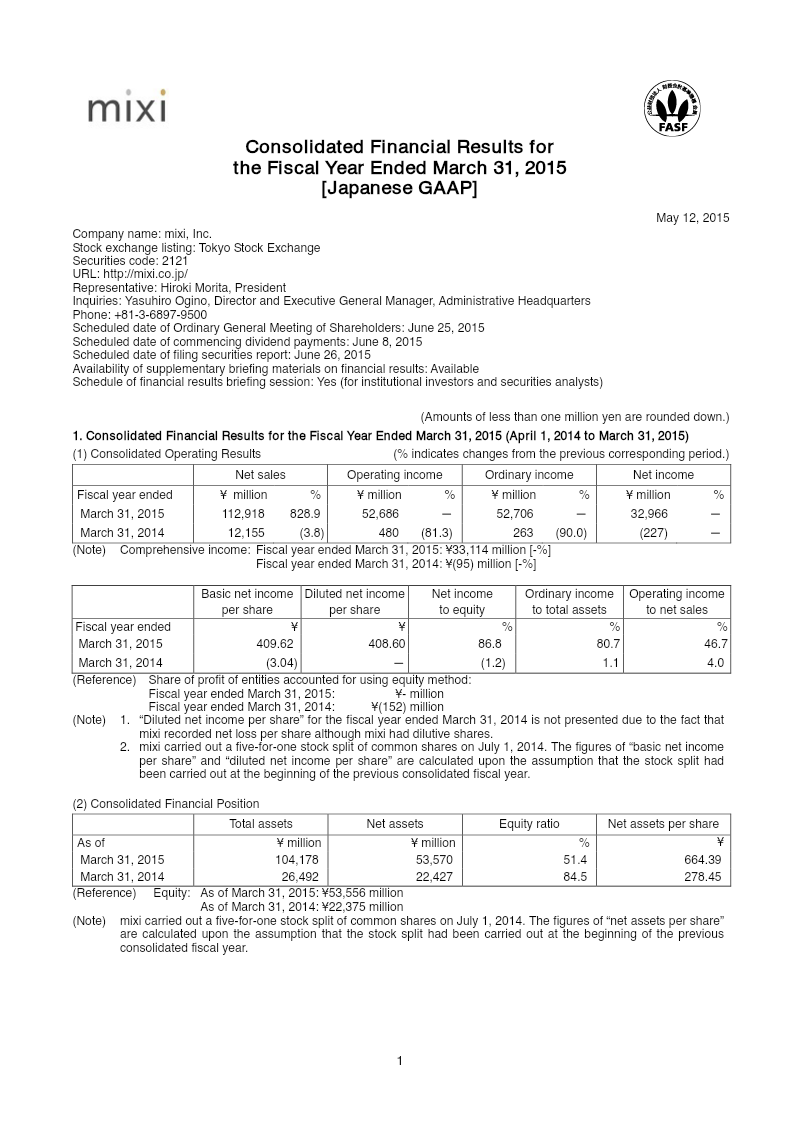

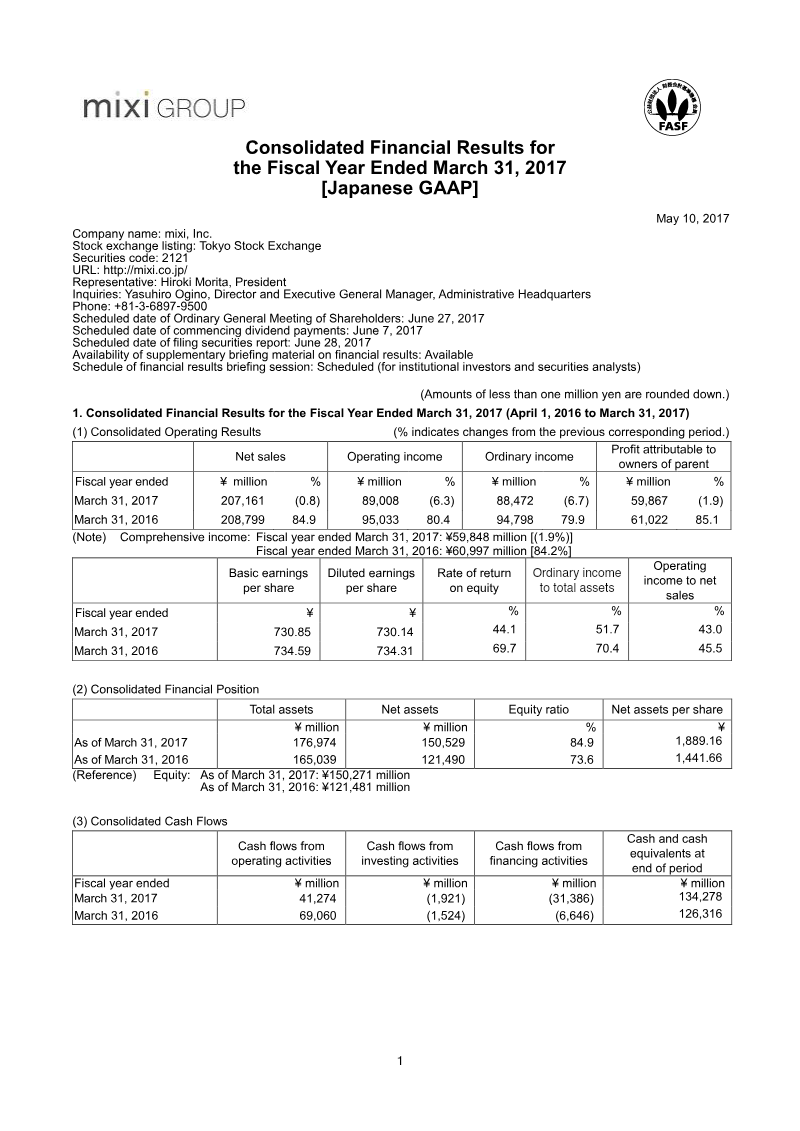

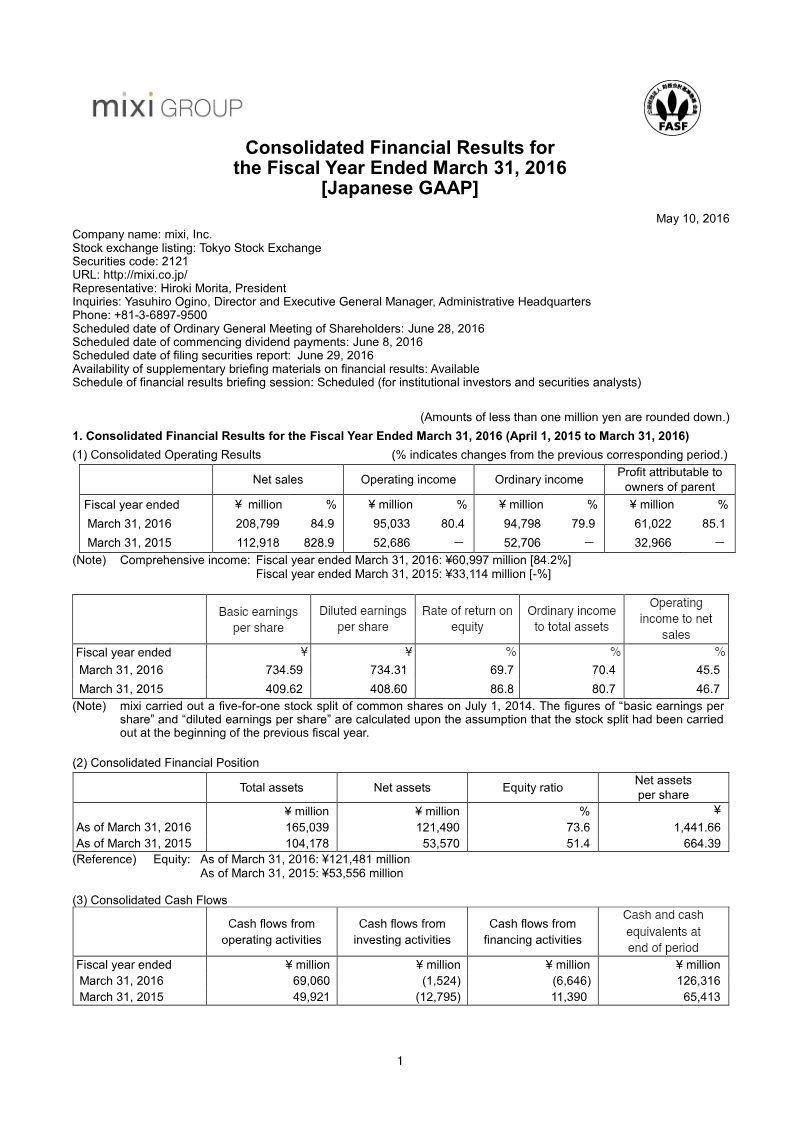

Mixi, Inc. achieved significant growth in the fiscal year ending March 31, 2016, with net sales rising 84.9% to ¥208,799 million and profit attributable to owners increasing 85.1% to ¥61,022 million.

See it on page 1The company’s financial position strengthened substantially, with cash and cash equivalents nearly doubling to ¥126,316 million and the equity ratio improving from 51.4% to 73.6%.

See it on page 1Operating income reached ¥95,033 million, primarily driven by the Entertainment Business, while the company diversified its ecosystem through the acquisitions of Hunza, Inc. and MUSE & Co., Ltd.

See it on page 27Operational scaling led to increased costs, with settlement fees rising to over ¥60 billion and advertising expenses reaching ¥15.8 billion.

See it on page 13Capital efficiency measures included a five-for-one stock split, an overseas share offering, and a ¥10 billion share repurchase program.

See it on page 22The outlook for the fiscal year ending March 31, 2017, is conservative, projecting a modest 4.4% increase in net sales and an 11.5% decline in net profit.

See it on page 2Operations remain heavily concentrated in the Japanese market, which accounts for over 90% of the company's total sales and assets.

See it on page 31Mixi, Inc. achieved exceptional financial growth during the fiscal year ended March 31, 2016, driven primarily by the expansion of its entertainment and smartphone-based commerce segments. Net sales surged 84.9% to ¥208,799 million, while profit attributable to owners rose 85.1% to ¥61,022 million. This performance significantly bolstered the company’s balance sheet, nearly doubling cash and cash equivalents to ¥126,316 million and increasing the equity ratio from 51.4% to 73.6%. While the Entertainment Business provided the vast majority of the ¥95,033 million in operating income, the company also integrated key acquisitions, including TicketCamp operator Hunza, Inc. and MUSE & Co., Ltd., to diversify its ecosystem.

The period was characterized by substantial operational scaling and capital restructuring. Settlement fees nearly doubled to over ¥60 billion, and advertising expenses rose to ¥15.8 billion, reflecting the intensified costs of supporting a high-growth digital portfolio. Following the previous year’s acquisition of Hunza, Inc. for ¥11,573 million, the company established an eight-year amortization period for its goodwill while opting for a full one-time amortization of MUSE & Co.’s remaining goodwill. To optimize capital efficiency, a five-for-one stock split was executed alongside an overseas share offering and a ¥10 billion share repurchase program.

Despite the record-breaking results of 2016, the outlook for the fiscal year ending March 31, 2017, remains conservative. Projections suggest a modest 4.4% increase in net sales and an anticipated 11.5% decline in net profit. Geographically, operations remain heavily concentrated in the Japanese market, which accounts for over 90% of total sales and assets. The adoption of revised Japanese accounting standards for business combinations further aligned financial reporting with modern regulatory frameworks without impacting the immediate bottom line.