Related Documents

Financial

Consolidated Financial Results for FY 2025: Supplementary Material

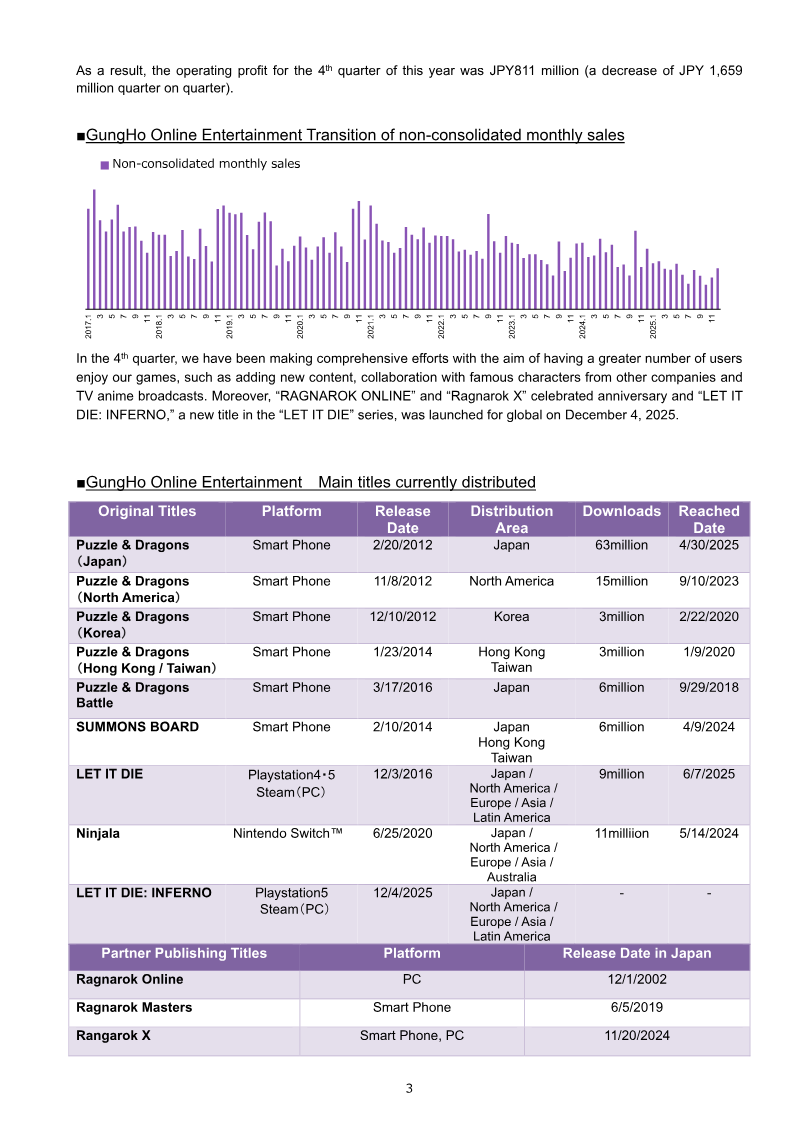

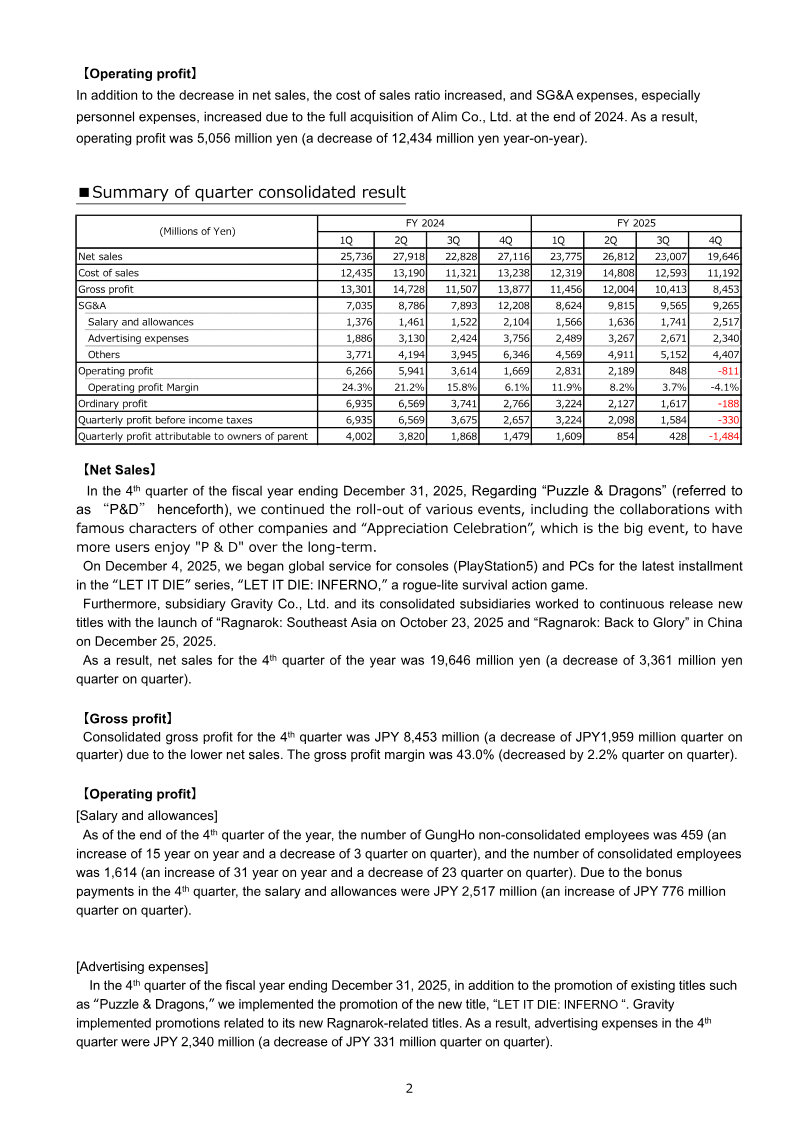

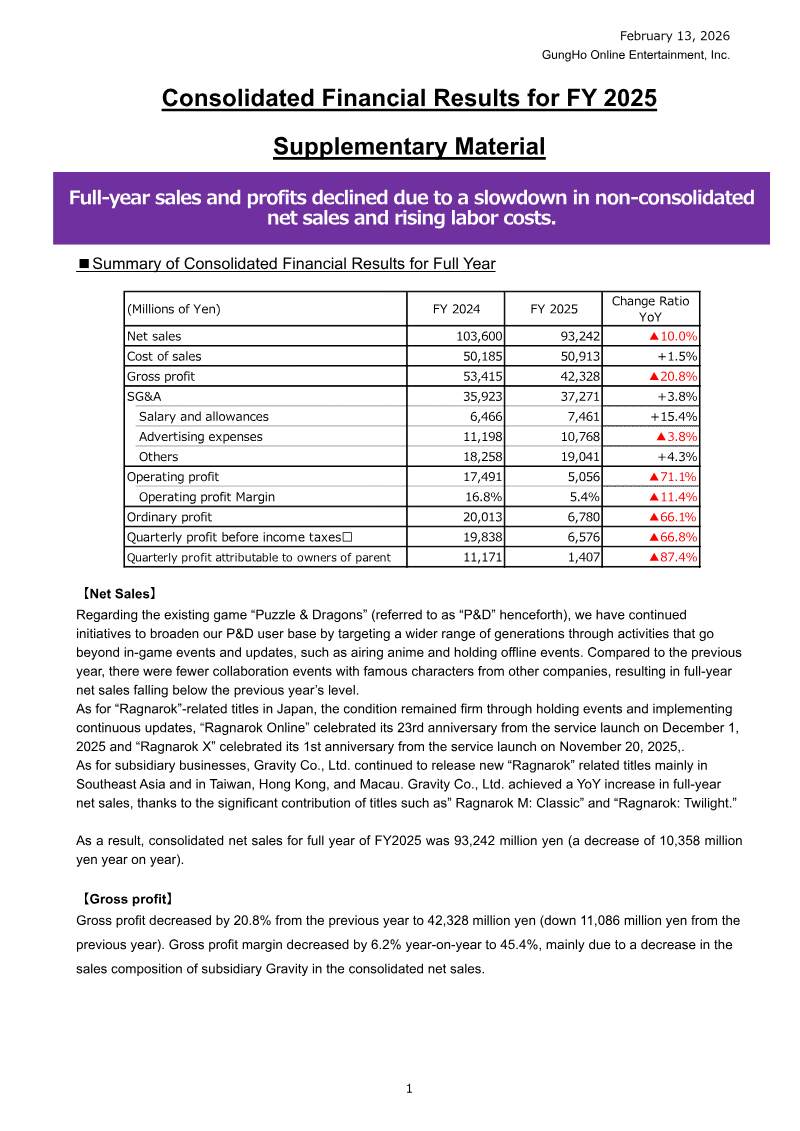

GungHo Online Entertainment reported a significant decline in financial performance for the fiscal year ending December 31, 2025. Consolidated net sales fell 10.0% year-on-year to 93,242 million yen, while operating profit plummeted 71.1% to 5,056 million yen. The downturn was primarily driven by a slowdown in non-consolidated sales from the flagship title Puzzle & Dragons, which suffered from fewer high-profile character collaborations compared to the previous year. Profitability was further pressured by rising labor costs following the full acquisition of Alim Co., Ltd. and increased bonus payments in the fourth quarter, leading to a quarterly operating loss of 811 million yen in the final period. The geographic scope of operations remains centered in Japan, though subsidiary Gravity Co., Ltd. provided a strategic buffer through successful releases in Southeast Asia, Taiwan, Hong Kong, and China. While Puzzle & Dragons remains the company’s core asset with 63 million downloads in Japan as of April 2025, newer titles like Ragnarok M: Classic and Ragnarok: Twilight contributed to Gravity’s year-on-year revenue growth. Additionally, the company expanded its multi-platform presence with the December 2025 global launch of LET IT DIE: INFERNO on PlayStation 5 and PC. Methodologically, the findings are based on consolidated financial statements and internal download tracking data. The results highlight a transition period for the company, characterized by a shifting sales mix and higher fixed costs. Despite the decline in annual net profit attributable to owners—which dropped 87.4% to 1,407 million yen—the company maintains a strong liquidity position with 130,474 million yen in cash and deposits, supporting continued investment in its long-term service titles and new global releases.

GungHo Online EntertainmentFeb 2026

Report

GungHo Online Entertainment Business Report Vol. 42

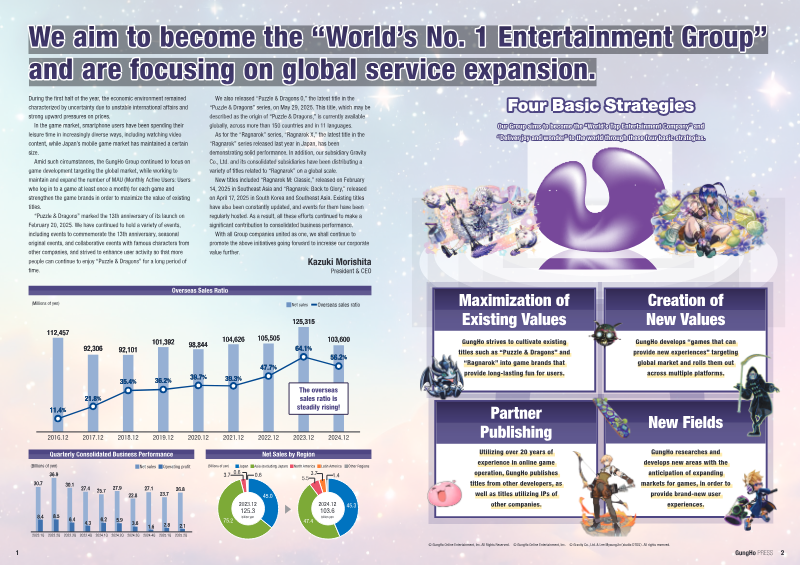

GungHo Online Entertainment’s business report outlines a strategic transition from a Japan-centric mobile focus toward a diversified global entertainment model. The primary thesis centers on leveraging established intellectual properties, specifically Puzzle & Dragons and the Ragnarok series, to anchor international expansion while developing new console and PC titles for a worldwide audience. Financial data indicates a significant shift in revenue composition, with the overseas sales ratio rising steadily to reach 64.1% by late 2024. While consolidated net sales saw a decline from 125.3 billion yen in 2023 to 103.6 billion yen in 2024, the group maintained a strong capital-to-asset ratio of 75.9%. Performance in the first half of 2025 shows net sales of 50.5 billion yen and an operating profit of 5.0 billion yen. To enhance shareholder value, the company revised its return policy in February 2025, committing to a consolidated dividend payout ratio of 30% or more and executing substantial share cancellations. The report highlights the longevity of core titles, noting that Puzzle & Dragons celebrated its 13th anniversary with over 63 million downloads in Japan. To sustain this momentum, the group released Puzzle & Dragons 0 in May 2025 across 150 countries in 11 languages. Simultaneously, the Ragnarok IP, managed by subsidiary Gravity Co., Ltd., has grown from 5 billion yen in annual sales in 2008 to approximately 50 billion yen, driven by mobile expansions in Asia and new initiatives in Latin America. Future growth is targeted through multi-platform development and the revitalization of existing series. Key projects include the redevelopment of the survival action title Deathverse: Let It Die and the release of the Lunar Remastered Collection. By focusing on original IPs for consoles and PC—areas where the group can demonstrate technical expertise—GungHo aims to establish brand recognition in Western markets where it was previously less known.

GungHo Online EntertainmentJan 2024

Financial

FY2025 Presentation Material

CyberAgent achieved record consolidated net sales of 874 billion yen for the 2025 fiscal year, marking nearly three decades of uninterrupted growth. This performance was characterized by a significant recovery in profitability, as operating income surged nearly 79% to 71.7 billion yen. The primary catalyst for this expansion was the gaming segment, which saw operating income nearly double due to the success of several new hit titles and a six-fold increase in overseas sales following aggressive global expansion. Furthermore, the Media and IP segment reached a major milestone by achieving profitability for the first time since the launch of the ABEMA streaming service, which saw record viewership and a doubling of active users for its original programming. While the gaming and media sectors flourished, the advertising division experienced a 14% decline in operating profit. This contraction resulted from heavy internal investments in artificial intelligence intended to drive long-term structural changes. Despite these costs, overall group sales grew by over 6%, supported by the establishment of new animation studios and expanded global distribution partnerships. The company’s strategic focus remains on diversifying its IP portfolio and leveraging external payment methods to improve margins within its digital storefronts. Looking toward the 2026 fiscal year, the outlook remains stable with projected sales of 880 billion yen, though operating income is expected to moderate to between 50 and 60 billion yen. This conservative forecast accounts for the inherent volatility of the gaming market and the high performance bar set by recent hits. Additionally, the organization is preparing for a significant leadership transition scheduled for late 2025, during which founder Susumu Fujita will transition to Chairman, and Takahiro Yamauchi will assume the role of President to lead the next phase of the company's evolution.

CyberAgentNov 2025

Financial

Consolidated Financial Results Data Appendix: FY2025 Q2

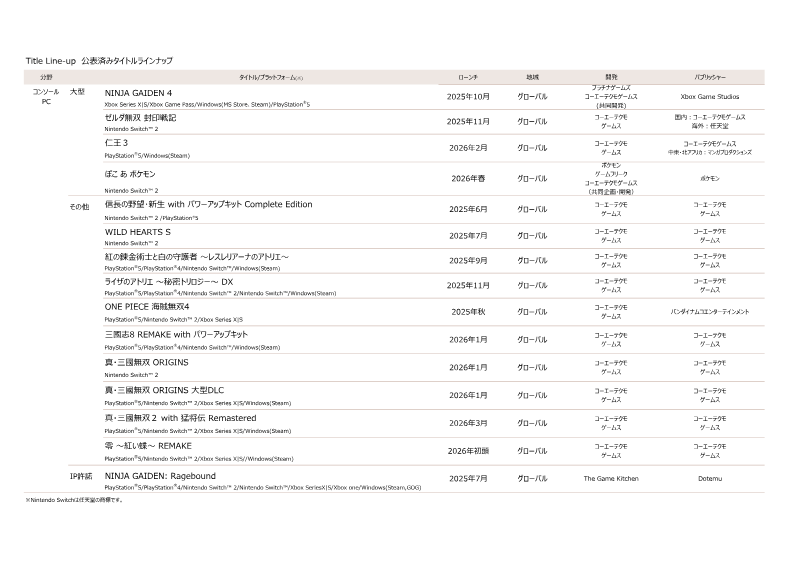

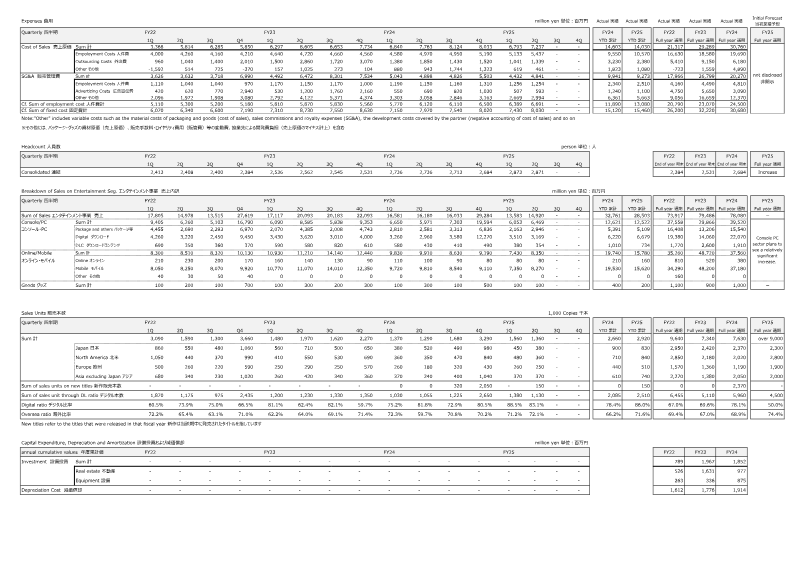

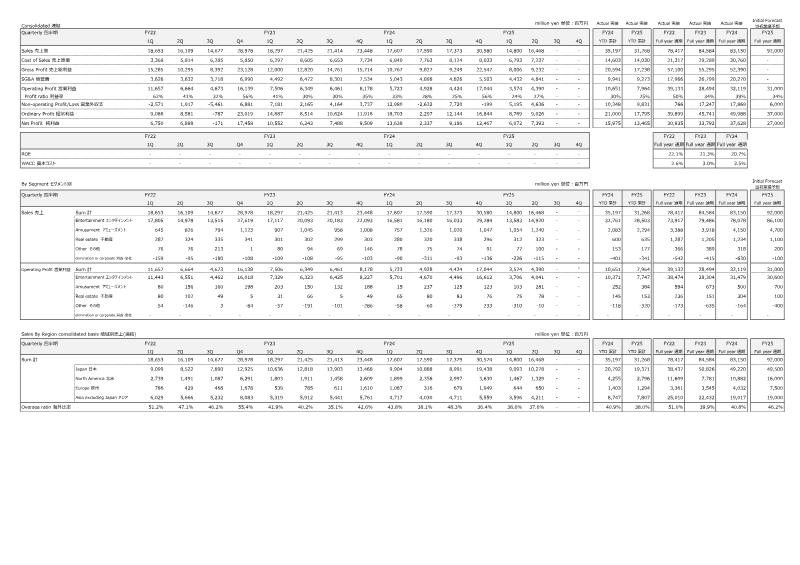

Koei Tecmo’s financial performance for the second quarter of fiscal year 2025 reflects a transitional period characterized by a year-to-date decline in consolidated sales to 31,268 million yen and an operating profit of 7,964 million yen. Despite this temporary downturn compared to the previous fiscal year, the organization maintains an optimistic full-year sales forecast of 92,000 million yen. This projected growth is predicated on a recovery in North American and European markets and the continued strength of the Entertainment segment. Operational costs have risen alongside a growing workforce, with headcount reaching 2,871 employees and employment expenses totaling 13,080 million yen. The strategic focus has shifted heavily toward digital and international markets, with digital sales now accounting for 83.1% of total revenue and overseas markets representing 72.1% of unit sales. The long-term growth strategy is supported by a robust pipeline of high-profile intellectual properties scheduled for late 2025 and early 2026. These upcoming releases include major sequels such as Ninja Gaiden 4 and Nioh 3, alongside several titles specifically optimized for the successor to the Nintendo Switch. The enduring value of established franchises remains a cornerstone of the business model. The Dynasty Warriors series continues to lead the portfolio with over 24 million lifetime units, followed by Nobunaga’s Ambition at 11 million and Romance of the Three Kingdoms at 9.5 million. Newer successes like Nioh and Atelier have each surpassed 8 million units, while Wo Long: Fallen Dynasty has secured over 5 million users. This console and PC success is complemented by a resilient online and mobile segment, where titles such as Dead or Alive Xtreme Venus Vacation have demonstrated significant longevity through more than seven years of continuous service.

Koei TecmoJan 2025