Related Documents

Report

FY25 Trading Update

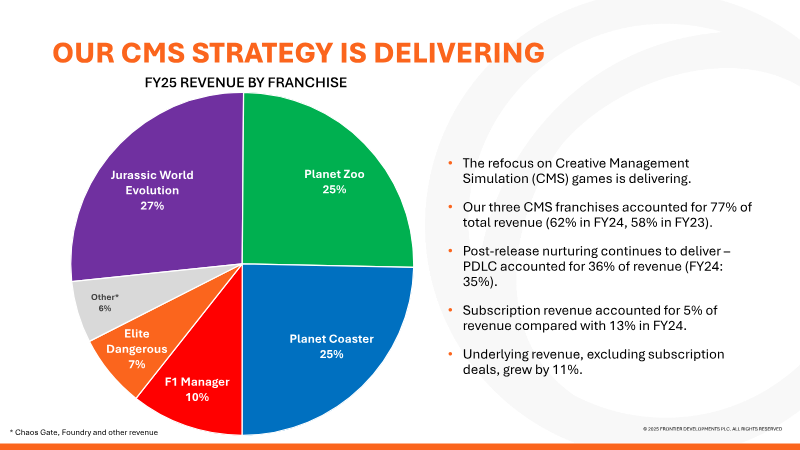

FOR THE FINANCIAL YEAR 1 JUNE 2024 TO 31 MAY 2025 PRIVATE AND CONFIDENTIAL RESERVED STRONG RESULTS AND INCREASED MOMENTUM 2 FINANCIALS the account or benefit of, U.S.

Frontier Developments

Financial

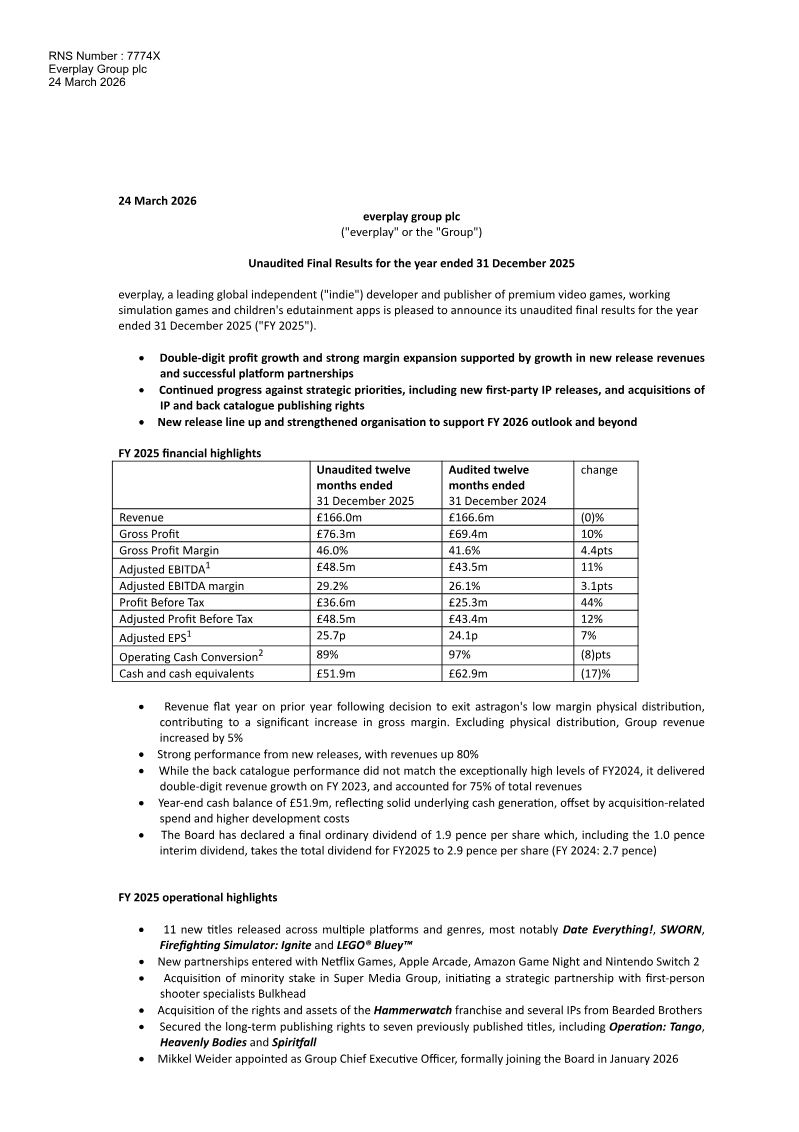

Unaudited Final Results for the Year Ended 31 December 2025

Everplay Group plc delivered unaudited FY 2025 results that demonstrate resilient profitability amid flat headline revenue. Total sales held steady at £166.0 million, a slight decline from the prior year, yet underlying revenue grew 5 % when excluding the impact of Astragon’s exit from physical distribution. Gross profit rose to £76.3 million, achieving a 46.0 % margin, while adjusted EBITDA increased 11 % to £48.5 million (29.2 % margin). Profit before tax surged 44 % to £36.6 million, driven by higher gross margins and reduced royalty expenses. The Group’s performance was underpinned by robust new‑release activity, with an 80 % revenue increase from fresh titles and a 75 % share of income derived from its back catalogue. Strategic initiatives—such as securing platform partnerships with Netflix Games, Apple Arcade and Amazon Game Night, exiting low‑margin physical distribution, and acquiring additional IP rights—position the company for future growth. Astragon’s revenue fell 33 % to £29.5 million after the distribution exit, yet its first‑party IP share climbed to 83 % of sales; StoryToys expanded revenue by 25 % to £30.4 million, buoyed by high‑profile licenses like LEGO® Bluey and Netflix Games. Share‑based remuneration expanded, with 317,970 options granted to Executive Directors, 349,805 to other employees and 87,957 to Non‑Executive Directors in FY 2025. The Long‑Term Incentive Plan now covers senior divisional leaders, and an All‑Employee Share Incentive Plan remains active. Outlook for FY 2026 highlights a pipeline of over 15 new games, including five first‑party IP titles, and anticipates H2‑weighted EBITDA growth. Financially, the Group reports a single aggregated segment comprising Games Label, Simulation and Edutainment. Revenue in 2025 split evenly between first‑party (£56.13 m) and third‑party IP (£109.86 m), with major platforms such as Steam, Microsoft, Sony, Nintendo and Apple each contributing over 10 % of sales. Operating profit benefited from amortisation of development costs (£14.16 m) and publishing rights, while tax expense rose to £9.35 million from £5.13 million in 2024 due to higher current and deferred tax adjustments. Goodwill impairment testing revealed no shortfalls except for the Astragon Simulation CGU, where recoverable amounts exceed carrying value by £78.5 million (2024: £31.0 million). Sensitivity analysis indicates that a 25 % decline in unreleased title revenues would bring the Astragon CGU to breakeven, but no other reasonable changes trigger impairment. Cash balances remained robust at £51.9 million in 2025, with operating cash flow of £57.7 million slightly below the prior year’s £59.9 million, underscoring solid liquidity and a foundation for continued profitable expansion.

Everplay GroupMar 2026

Financial

3rd Quarter Report: Fiscal Year Ending March 31, 2026

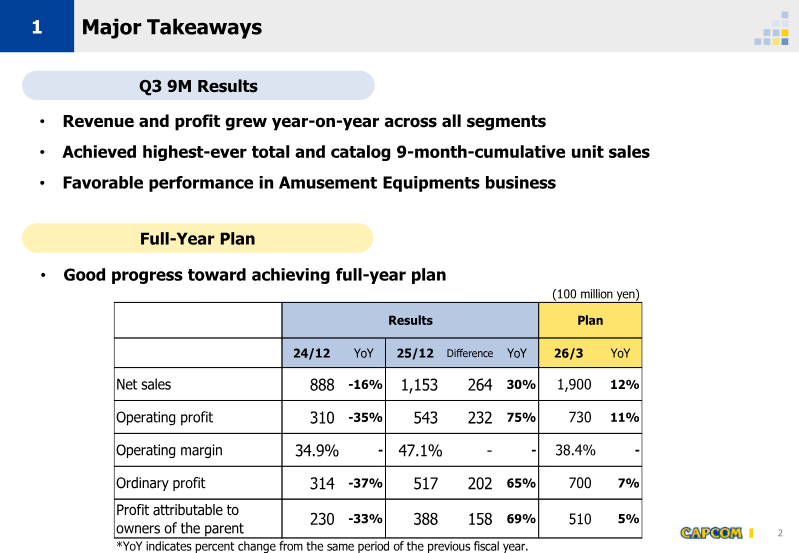

This financial report details Capcom’s consolidated performance for the third quarter of the fiscal year ending March 31, 2026. The findings indicate significant year-on-year growth in both revenue and profit across all business segments, driven primarily by the sustained performance of catalog titles and strong results in the amusement equipment division. Net sales reached 115.3 billion yen, a 30% increase over the previous year, while operating profit rose 75% to 54.3 billion yen. These results place the company on a favorable trajectory to meet its full-year targets of 190 billion yen in net sales and 730 billion yen in operating profit. The Digital Contents segment remains the primary driver of growth, with unit sales reaching a record 9-month high of 34.6 million units. Catalog titles accounted for 96.4% of these sales, underscoring the long-term value of core franchises such as Resident Evil, Monster Hunter, and Street Fighter. Notably, Monster Hunter Wilds surpassed 11 million cumulative units, while Resident Evil 4 and Street Fighter 6 continued to show steady growth. Digital sales now represent 94.1% of total units, with PC platforms alone accounting for over 55% of the volume. Geographically, overseas markets dominate the business, representing nearly 90% of total unit sales. Beyond software, the Arcade Operations and Amusement Equipments segments reported double-digit growth. Arcade sales rose 12% following the opening of new stores and the expansion of specialty formats, while Amusement Equipments saw a 74% surge in net sales due to the strong performance of smart slot titles like Shin Onimusha 3. The company’s strategic outlook remains focused on leveraging its leading brands through upcoming releases such as Resident Evil Requiem and Monster Hunter Stories 3, alongside cross-media expansions including a new Devil May Cry anime and a live-action Street Fighter film.

CapcomFeb 2026

Report

Square Enix Next: That Excitement Once Again

Square Enix’s recent performance review exposes a persistent decline in revenue growth and profitability over the past three years, with operating income falling 32 % and ROE dropping 61 %. The downturn is driven primarily by weak margins in both high‑definition (HD) and small‑dungeon (SD) game segments, excessive portfolio fragmentation, sub‑optimal product design and promotion, and escalating development costs. While the MMO licensing arm remains the sole growth driver (+11 %), overall gaming revenue has slipped, with HD and SD titles declining 4 % and 5 % respectively. Operating margins for these segments hover around 35–40 %, noticeably higher than the industry average of 28 % but still lagging behind competitors, indicating inefficiencies that are not being adequately addressed. The company’s medium‑term “Reboots” plan offers only high‑level directions without concrete key performance indicators or quantitative targets. Critical gaps include a lack of clear business‑portfolio strategy, insufficient disclosure on non‑core business rationales, and no defined mechanisms for monitoring progress or maximizing shareholder value. Capital allocation disclosures are similarly weak: cost‑of‑capital calculations, ROE and ROIC targets, and hurdle rates are absent, while share‑buyback authorization remains unused despite a sharp price decline. SG&A costs exceed peer norms by 5–6 ppt, driven largely by an oversized sales force, further eroding profit margins. Geographically, SD game revenue is almost entirely domestic; the Japanese market has contracted 2 % annually since 2020, and overseas growth remains only 3 %. The company’s global SD strategy is inert, with a 7 % overseas expansion rate falling short of projected growth and flagship titles such as *FFVII Ever Crisis* deriving 70 % of revenue from Japan. Non‑core Amusement and Publishing businesses are undervalued, with a significant conglomerate discount relative to peers and declining sales and margins. Limited cross‑synergy between game and publishing arms further hampers value creation. In summary, Square Enix faces a multifaceted challenge: declining core game performance, weak strategic direction and KPI setting, high SG&A costs, and an underperforming non‑core portfolio. Addressing these issues through tighter cost control, clearer performance metrics, aggressive overseas expansion, and potential portfolio optimization is essential to restore corporate value and achieve sustainable growth.

InvestGameDec 2025