Presentation

Slovak Game Industry Infographic 2024

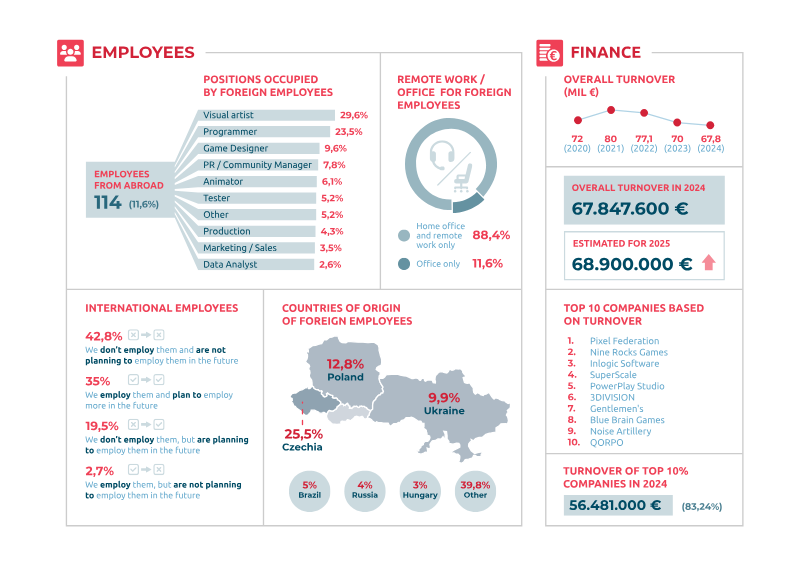

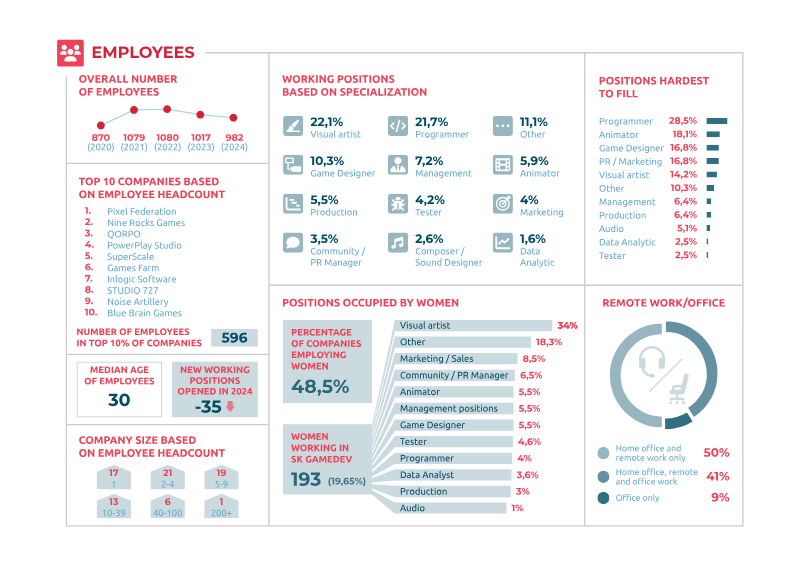

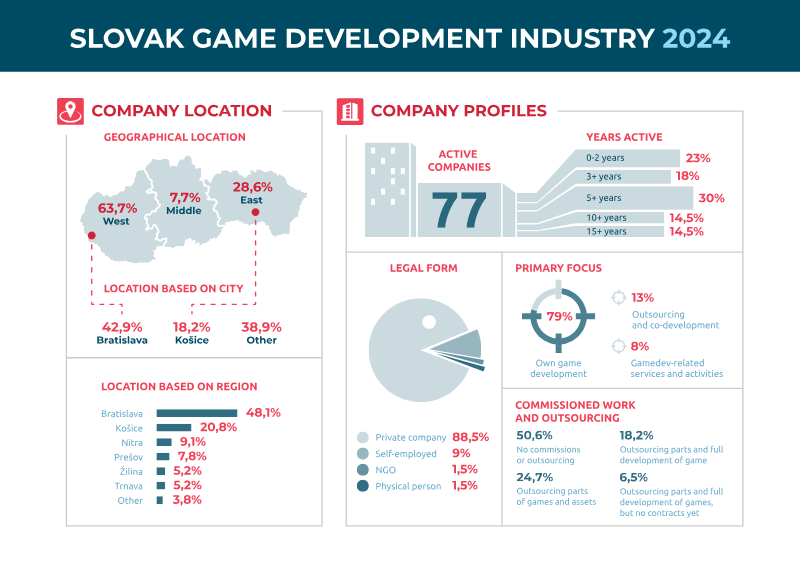

The 2024 Slovak Game Industry report provides a comprehensive overview of the nation’s game development sector, detailing its economic performance, workforce composition, and operational landscape as of December 31, 2024. The industry is characterized by a mix of established firms and newer entrants, with a primary focus on own-game development, which accounts for nearly 43% of activities, followed by outsourcing and co-development services. Geographically, the industry is concentrated in Bratislava and Košice, reflecting the urban centralization of technical talent and infrastructure. Financially, the sector generated a total turnover of approximately 67.8 million euros in 2024, with a high degree of market concentration; the top 10% of companies account for over 83% of this revenue. The workforce consists of 982 employees with a median age of 30 to 35. While the industry remains male-dominated, women represent nearly 20% of the workforce, primarily in visual arts and marketing roles. Foreign talent is a significant component of the ecosystem, comprising 11.6% of the total headcount, with employees largely sourced from Poland, Ukraine, and Czechia. Remote work is highly prevalent, with 91% of companies offering some form of home office or fully remote arrangements. Development trends show a strong preference for PC platforms, which serve as the primary target for both released and in-development titles. Self-funding remains the dominant financial model for projects, utilized by 80.5% of companies, while public funding and international publishers play secondary roles. Despite the industry's growth, stakeholders identify a need for improved state support, specifically requesting tax incentives, increased R&D funding, and more effective mechanisms for hiring foreign professionals. The report highlights a sector that is technically mature but actively seeking structural improvements to enhance its international competitiveness and sustainability.

Slovak Game Developers AssociationJan 2024

Presentation

Slovak Game Industry Infographic

The Slovak game industry demonstrates consistent growth and professional maturation, characterized by a robust increase in both turnover and workforce capacity. As of the end of 2019, the sector comprised 55 active companies, with a significant geographic concentration in Bratislava, which hosts 52 percent of all firms, followed by Košice at 24 percent. The industry’s economic footprint is substantial, with the top ten companies generating over 48 million euros in annual turnover. Workforce development has kept pace with this expansion, as the total number of employees rose from 436 in 2016 to 762 by 2019, supported by the creation of 238 new positions in the final year of the reporting period. Development activity remains diverse, with a strong emphasis on PC and mobile platforms. PC development leads the market at 73 percent, followed closely by Android and iOS at 60 percent and 44 percent, respectively. While self-publishing remains the dominant business model—utilized by 77 percent of companies for PC and 74 percent for mobile—the industry also leverages a mix of public funding, which supports 29 percent of projects, and commissioned work. Despite this growth, the sector faces talent acquisition challenges, particularly in filling roles for programmers, game designers, and marketing specialists. The industry maintains a global outlook, with 40 international employees and a significant portion of the workforce engaged in outsourcing and international collaboration. Women represent a notable segment of the industry, occupying 129 positions, primarily within graphic arts, marketing, and production roles. With 221 active projects reported in 2020 and ongoing support from the Slovak Arts Council, the industry is positioned for continued development, balancing in-house creative output with strategic international partnerships and a diversified platform strategy.

Slovak Game Developers AssociationJan 2020