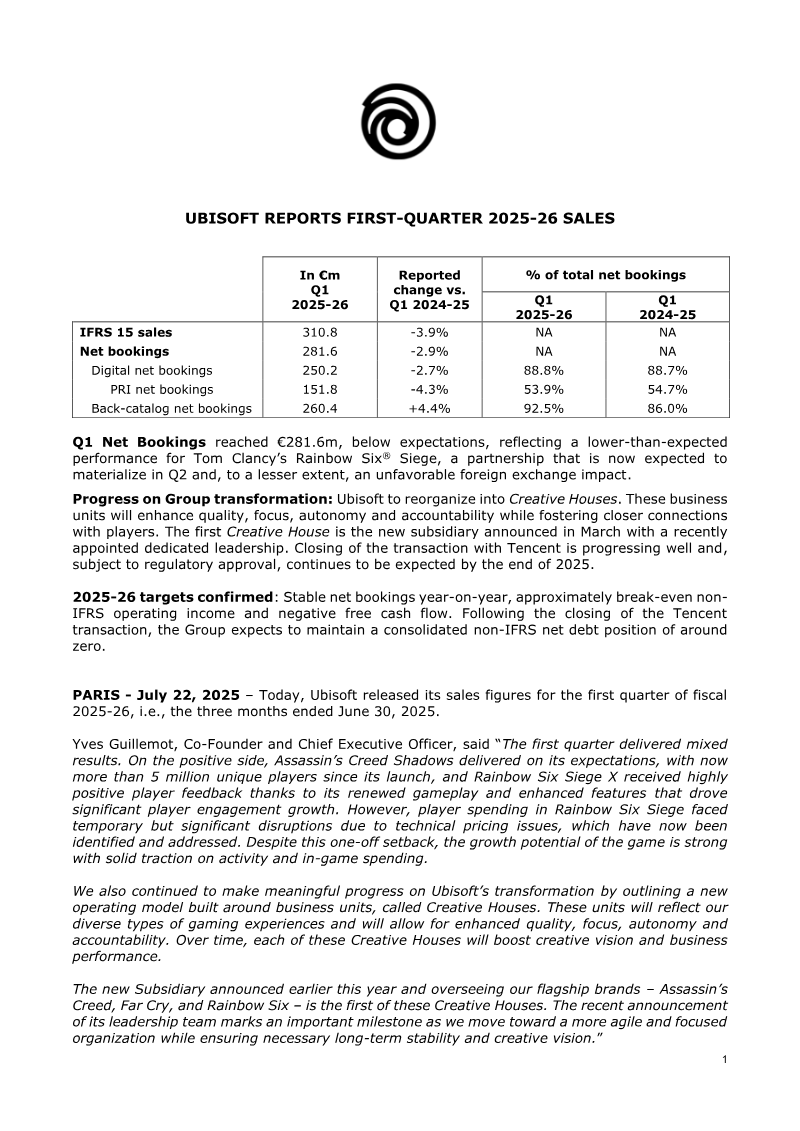

Ubisoft’s first-quarter results for fiscal year 2025-26 reflect a period of mixed performance, with net bookings reaching €281.6 million. This figure fell short of internal expectations, representing a 2.9% decline compared to the same period in the previous fiscal year. The shortfall is primarily attributed to technical pricing issues involving prepaid currency cards that impacted in-game spending for Tom Clancy’s Rainbow Six Siege, alongside unfavorable foreign exchange impacts. Despite these setbacks, the company maintains its full-year financial targets, which include stable year-on-year net bookings and a break-even non-IFRS operating income.

The company is currently undergoing a significant organizational transformation, shifting toward a model centered on autonomous business units known as Creative Houses. This strategy is designed to enhance creative focus, accountability, and operational agility across its diverse portfolio. The first of these units, which oversees flagship franchises including Assassin’s Creed, Far Cry, and Rainbow Six, has already appointed its leadership team. Furthermore, the company continues to progress toward the closing of its transaction with Tencent, which is anticipated by the end of 2025.

Operational highlights for the quarter include strong engagement for Assassin’s Creed Shadows, which surpassed 5 million unique players, and a robust start for Tom Clancy’s The Division 2. While the Rainbow Six Siege pricing exploit caused temporary disruption, the title showed strong recovery in June, achieving its third-highest monthly active user performance in history. Looking ahead, the company expects second-quarter net bookings to reach approximately €450 million, supported by new B2B partnerships and continued content expansion across its core titles.

Ubisoft · 2026

Ubisoft · 2026

Ubisoft · 2026

Ubisoft · 2026

Ubisoft · 2026

Ubisoft · 2026

Ubisoft · 2026

Ubisoft · 2025

Ubisoft · 2025

Ubisoft · 2025

Ubisoft · 2025

Ubisoft · 2025

Aream & Co · 2026

Konvoy · 2024

DDM · 2024

Nintendo · 2024

Frontier Developments

11 bit studios

Frontier Developments

Koei Tecmo

PCF Group

Frontier Developments

Capcom

11 bit studios