Related Documents

Report

Mobile Gaming Market Outlook 2022

The global mobile gaming landscape has entered a period of stabilization following pandemic-era surges, with quarterly downloads maintaining a steady baseline of 14 billion. Although total revenue experienced a 6% year-over-year decline to $21.2 billion in early 2022, the market remains significantly larger than its pre-pandemic state. Casual games continue to lead in volume, representing 80% of all downloads, yet Mid-Core titles remain the primary economic engine, generating 60% of total player spending. While the United States maintains its position as the leading consumer market, the Asia-Pacific region exerts increasing influence, evidenced by Taiwan’s rise to the fifth-largest global market and the region's dominance in high-monetization genres like MMORPGs and Card Battlers. Strategic advertising and intellectual property integration have become essential for navigating this competitive environment. Strategy and RPG titles are increasingly prioritizing YouTube for share of voice, while the acquisition of MoPub by AppLovin has shifted the advertising landscape for strategy games. Success in the rapidly growing Card Battler sub-genre, which earns 62% of its revenue from the APAC region, is largely driven by high-performing titles like Yu-Gi-Oh! Master Duel and the effective use of Live Ops and Season Passes. Furthermore, cross-media synergies, such as the impact of the Netflix series Arcane on game downloads, demonstrate the power of multimedia IP in driving user acquisition. The market outlook suggests a temporary correction phase with a projected return to growth by 2023. While Asian markets currently account for 80% of MMORPG revenue, Western interest is growing, as seen with the successful U.S. launch of Diablo Immortal. Similarly, the Real-Time Strategy sector is seeing a geographic shift, with China overtaking the U.S. as the top market for the sub-genre. Future expansion across these segments will likely depend on localized IP collaborations and sophisticated user acquisition strategies tailored to specific regional preferences.

Sensor TowerMay 2022

Report

The State of Mobile Gaming 2022: Market Trends and Top Titles in the U.S., Europe, and Asia

Global mobile gaming revenue experienced its first historical year-over-year decline in the first quarter of 2022, falling 6% to $21.2 billion. This contraction follows a period of unprecedented pandemic-driven growth and is largely attributed to market stabilization and rising inflation, which contributed to a 22% spending drop on Google Play. While established markets such as the United States and Japan saw double-digit revenue decreases, global game adoption remained resilient at approximately 14 billion quarterly downloads, a figure significantly higher than pre-pandemic benchmarks. Geographic performance diverged sharply between mature and emerging regions. The U.S. market saw consumer spending fall 10% to $5.8 billion, and the broader Asian market declined 7% to $11.2 billion. Conversely, emerging markets in Southeast Asia and the APAC region showed significant growth. India solidified its position as the global leader in volume, accounting for 15% of worldwide installs and a 73% increase in consumer spending. In Europe, Turkey emerged as a primary growth hub, recording a 36% revenue increase and becoming the region's fastest-growing market for both downloads and development. Genre and monetization trends indicate a shift toward sophisticated engagement mechanics. While RPG and Shooter revenues fell by 13% and 14% respectively, RPG remains the highest-grossing genre globally, and Hypercasual titles continue to dominate downloads with a 32.5% market share. Real-Time Strategy emerged as the fastest-growing sub-genre by revenue. To combat declining spending, developers are increasingly adopting Season Passes, now utilized by half of the world’s top-grossing titles to revitalize legacy games. Furthermore, strong correlations have emerged between specific aesthetics and monetization strategies, particularly the synergy between Anime art styles and Gacha mechanics, as well as the integration of ad-removal subscriptions within casual titles.

Sensor TowerJan 2022

Report

The State of Mobile Gaming 2023: Mobile Gaming Market Trends and Top Titles in the U.S., Europe, and Asia

The global mobile gaming landscape underwent a significant structural transition in 2022, characterized by a 14% decline in total player spending from its 2021 peak alongside a stabilization of download volumes at approximately 13.8 billion per quarter. While major markets such as the United States, Japan, and South Korea experienced revenue contractions, China emerged as the second-largest market globally, and India solidified its position as the leader in download volume, accounting for 17% of total installs. This period marked a definitive shift away from the hypercasual genre, which saw an 18% decline in downloads due to rising user acquisition costs and broader economic pressures. In response to these market pressures, the industry is pivoting toward a hybridcasual model that blends accessible core mechanics with sophisticated mid-core monetization and meta-progression features. This emerging segment grew by 13% and generated $1.4 billion in revenue, driven by significantly higher player engagement than traditional casual titles. Success in the current environment is increasingly dictated by the effective use of Live Ops, which now accounts for 97% of revenue among top-grossing games. Features such as character collection and social clan systems have become essential for maintaining high engagement levels and driving long-term player retention. While established genres like RPGs and shooters faced revenue declines, the action genre grew by 9%, and subscription-based models gained momentum, exemplified by the expansion of ad-free gaming catalogs. Conversely, the crypto and NFT gaming sector experienced a sharp downturn, with downloads falling from 46 million to 29 million and revenue dropping by 35%. Despite the overall contraction in spending, the market remains larger than pre-pandemic levels, with legacy titles like Honor of Kings and Subway Surfers maintaining dominance in revenue and download rankings, respectively, across a diversifying global audience.

Sensor TowerJan 2023

Report

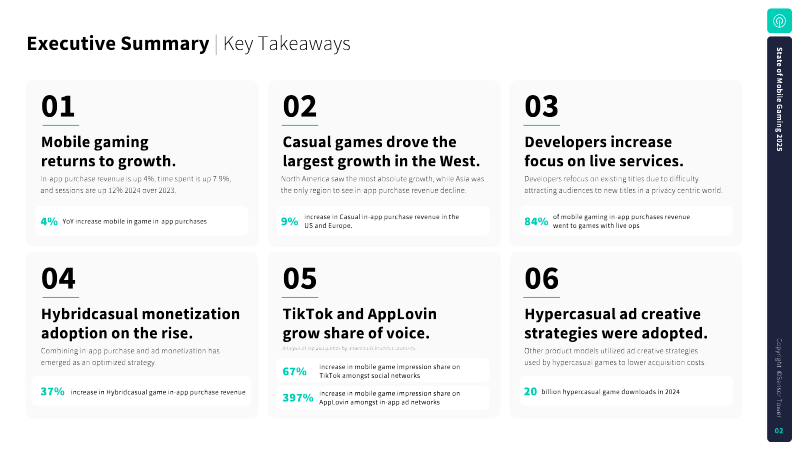

State of Mobile Gaming 2025

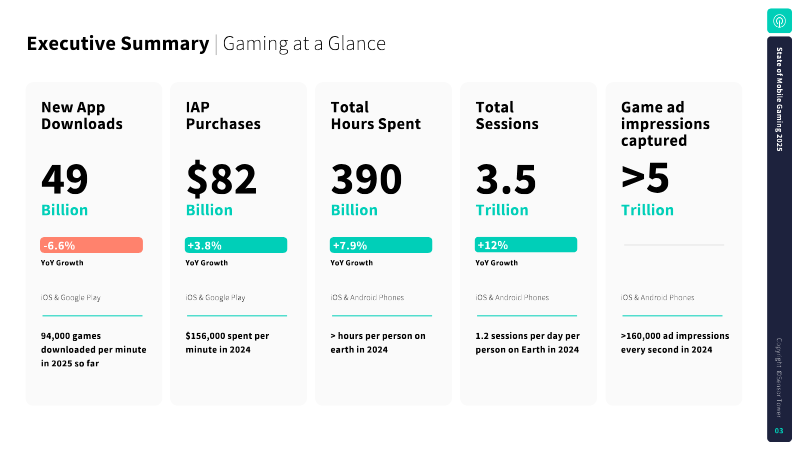

The global mobile gaming market entered a period of mature recovery in 2024, characterized by a strategic pivot toward live services and high-value player retention. While total downloads declined by 6.6%, global in-app purchase revenue grew by 4% to reach $82 billion. This growth was primarily driven by North America and the Middle East, offsetting spending declines in Asia. The industry has transitioned into a "live operations" era, where 84% of all revenue is generated by games utilizing continuous updates and seasonal events. This shift is further evidenced by a 50% decrease in new game releases since 2020, as publishers prioritize high-quality core titles over volume. Genre performance highlights a market dominated by Strategy and RPG titles, which collectively generated over $34 billion in 2024. Action games emerged as the fastest-growing category with a 46% revenue increase, fueled by breakout hits like Last War: Survival. Despite the dominance of established franchises, a record 11 games surpassed $1 billion in annual consumer spend, including MONOPOLY GO!, which secured the top global position. The market is also seeing a demographic shift, particularly in the United States, where the 18-24 age group now represents 18% of the player base, up from 13% in 2022. Marketing strategies have evolved to combat rising user acquisition costs, with a significant move toward high-intent creative content and short-form video platforms. TikTok experienced a 67% year-over-year growth in social ad share, while mid-core developers nearly doubled their impression share on social networks. To maintain profitability, publishers are increasingly leveraging external web stores, celebrity partnerships, and localized cultural influencers, such as virtual YouTubers in the Japanese market. These trends underscore a broader industry movement toward sophisticated monetization models and IP-driven growth in an increasingly concentrated competitive landscape.

Sensor TowerMar 2025