LegalKadokawa Corporation

Notice Concerning Change of Major and Principal Shareholder

2 pages~5 min full read

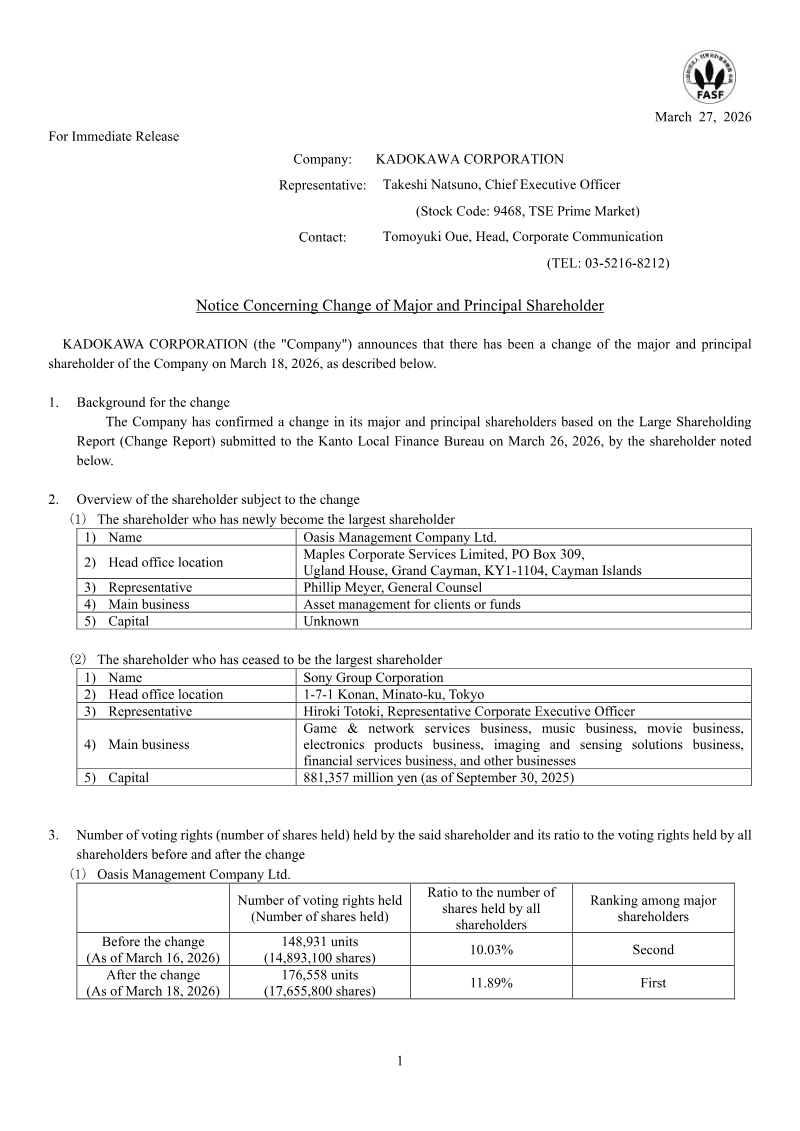

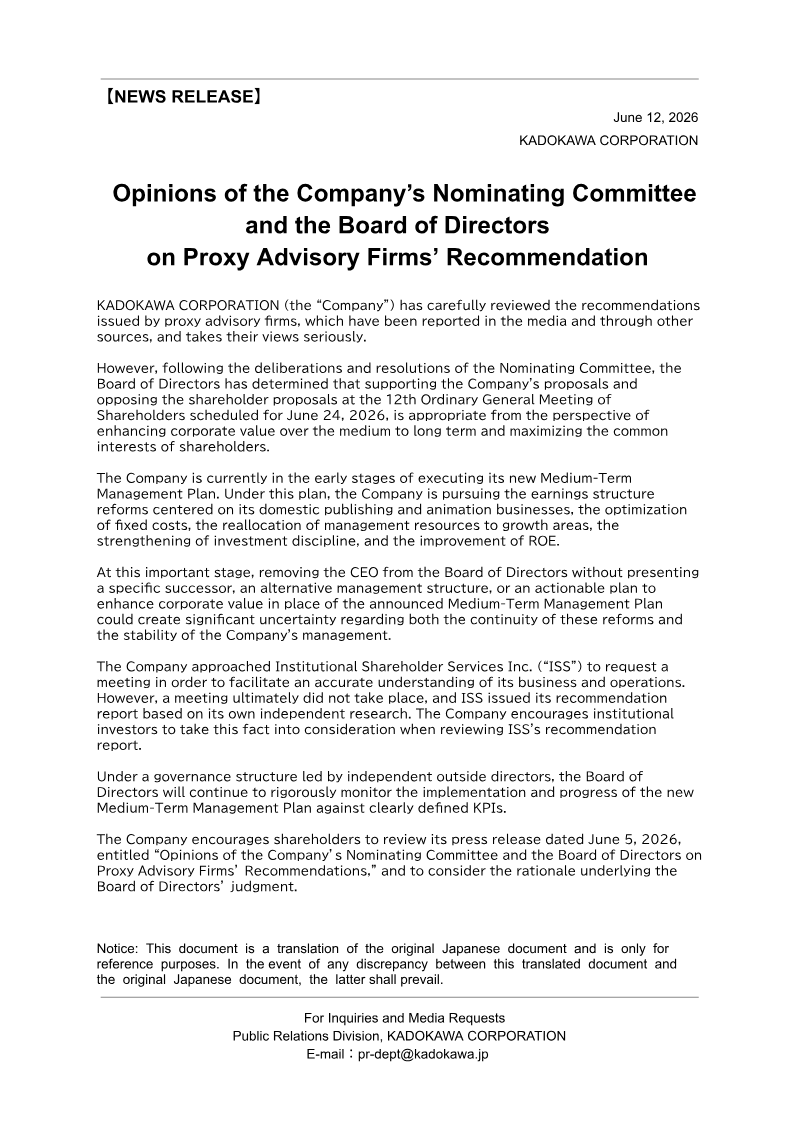

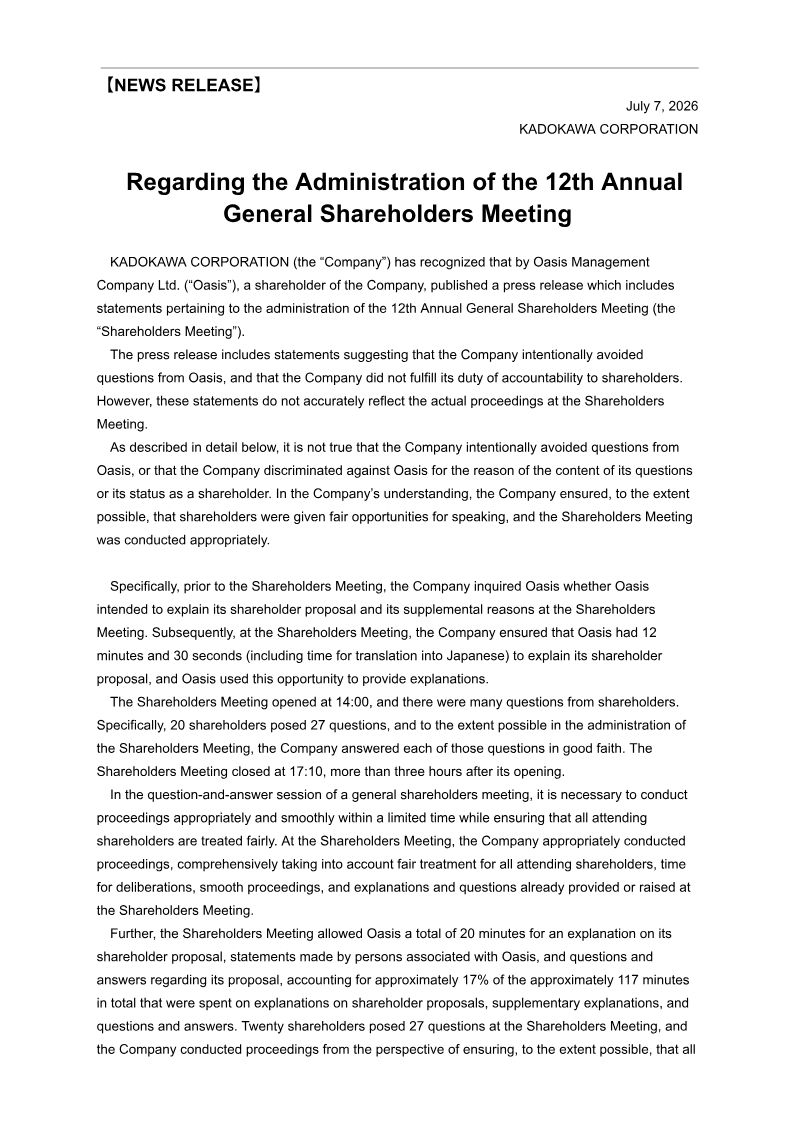

KADOKAWA CORPORATION has officially confirmed a shift in its primary shareholder structure, effective March 18, 2026. Oasis Management Company Ltd., a Cayman Islands-based asset management firm, has ascended to the position of the company’s largest shareholder, surpassing the Sony Group Corporation. This transition follows the submission of a Large Shareholding Report to the Kanto Local Finance Bureau, which detailed the acquisition of additional voting rights by the investment firm.

Data indicates that Oasis Management increased its holdings from 148,931 voting units to 176,558 units, raising its ownership stake from 10.03% to 11.89%. Conversely, the Sony Group Corporation, which previously held the top position with a 10.10% stake, now holds 10.04% of the voting rights, moving into the second position among major shareholders. These figures are calculated against a total of 1,484,474 voting rights, a total that accounts for recent treasury share disposals related to performance-based stock compensation plans.

The findings are derived from official regulatory filings and internal shareholder register assessments conducted by KADOKAWA CORPORATION as of March 2026. While the company has acknowledged this change in its ownership hierarchy, it has issued no specific commentary regarding the future strategic implications of this shift in its shareholder base. The disclosure serves as a formal notification to the Tokyo Stock Exchange and the public regarding the change in the company's principal investor.

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation · 2026

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

Kadokawa Corporation

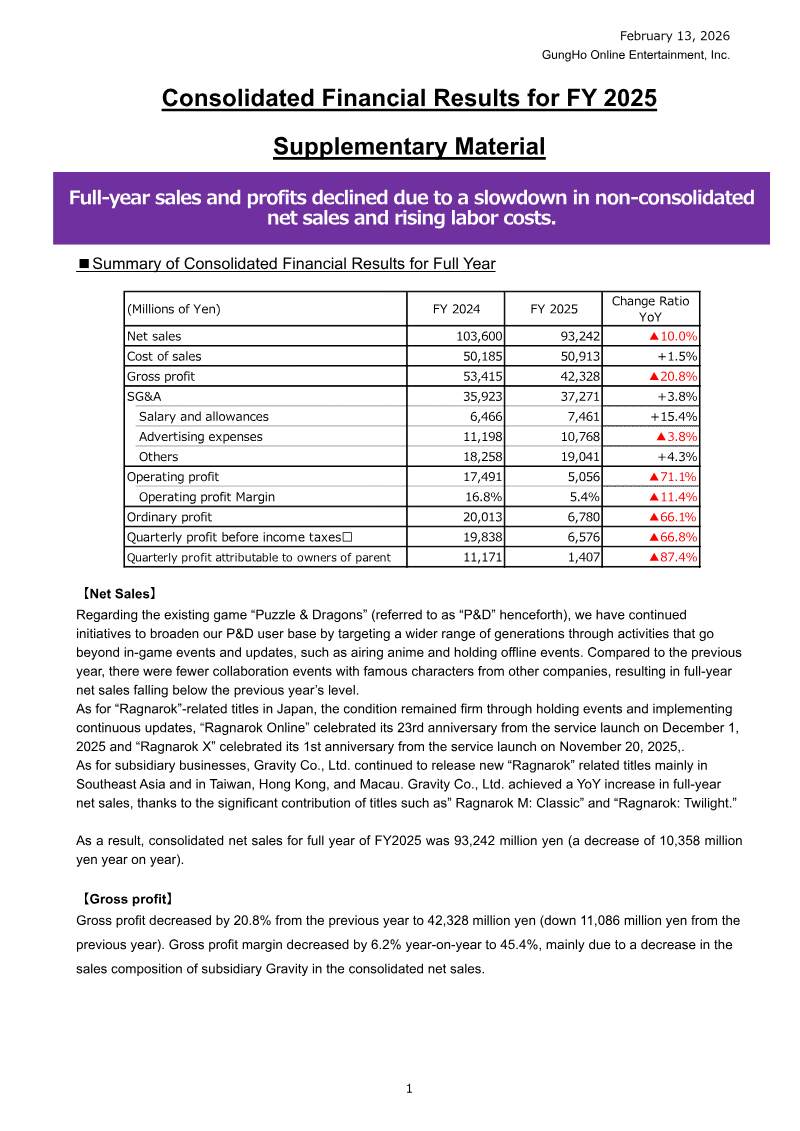

GungHo Online Entertainment · 2026

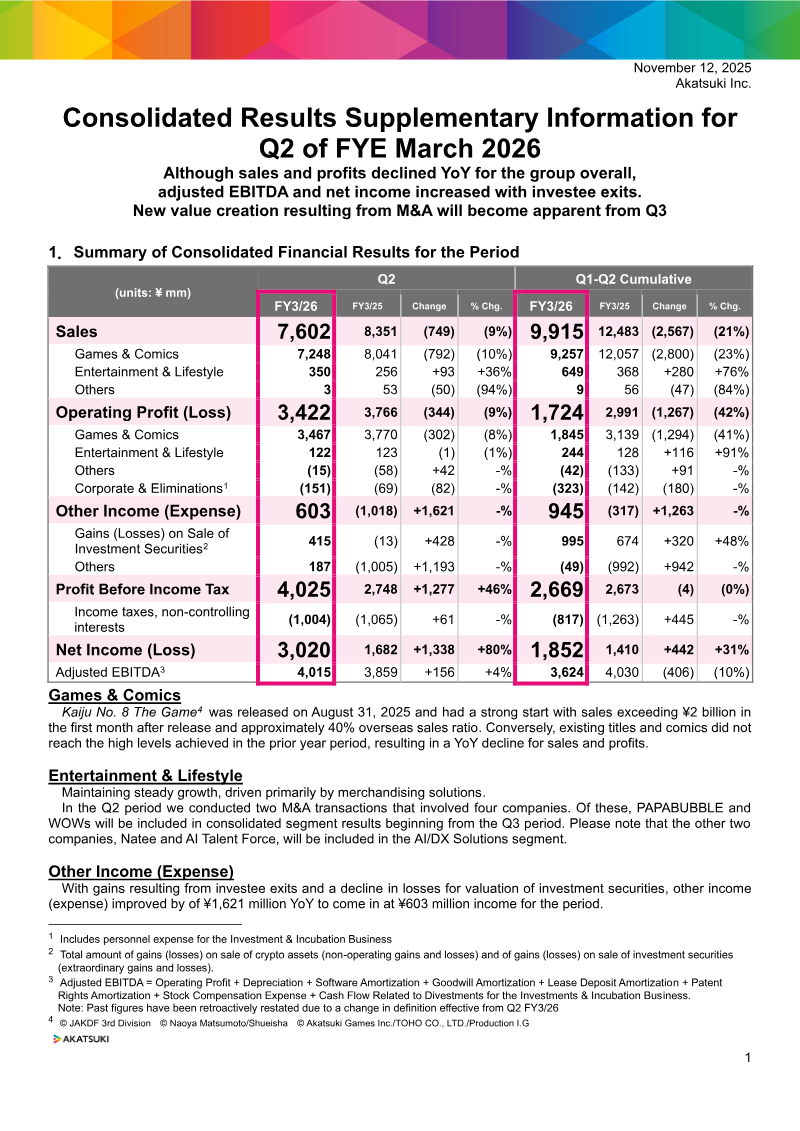

Akatsuki · 2026

Akatsuki · 2026

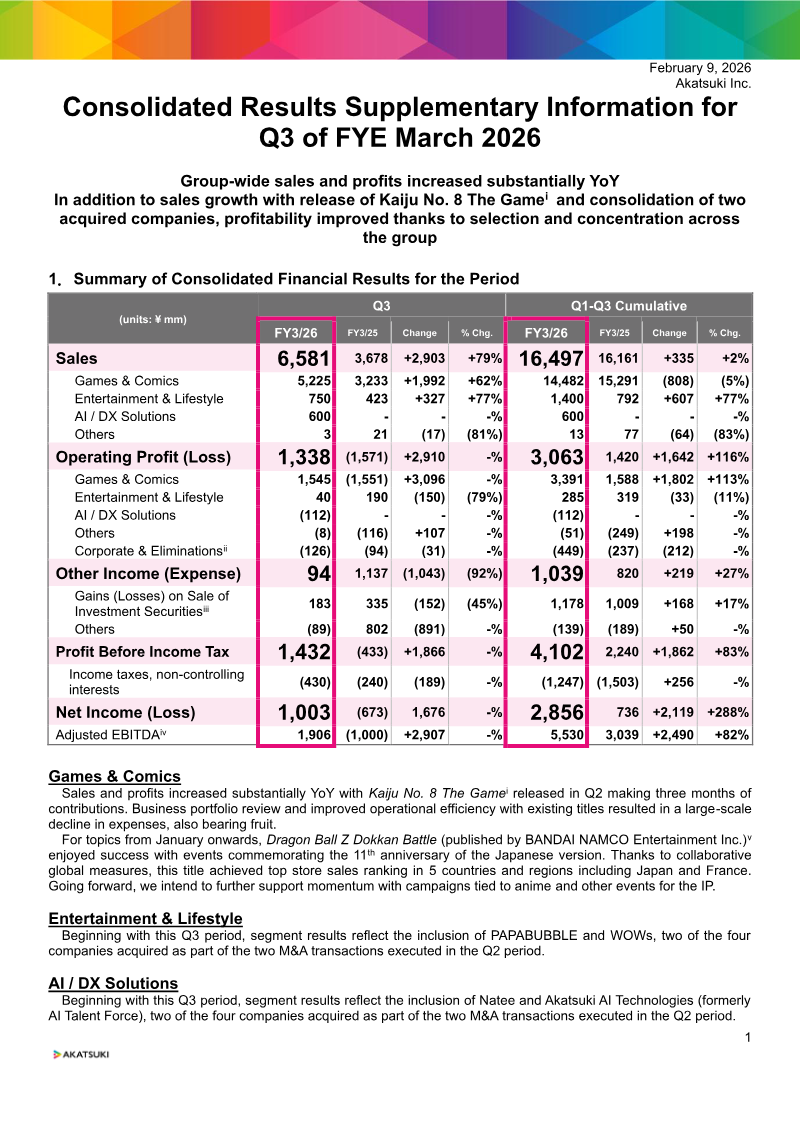

GungHo Online Entertainment · 2026

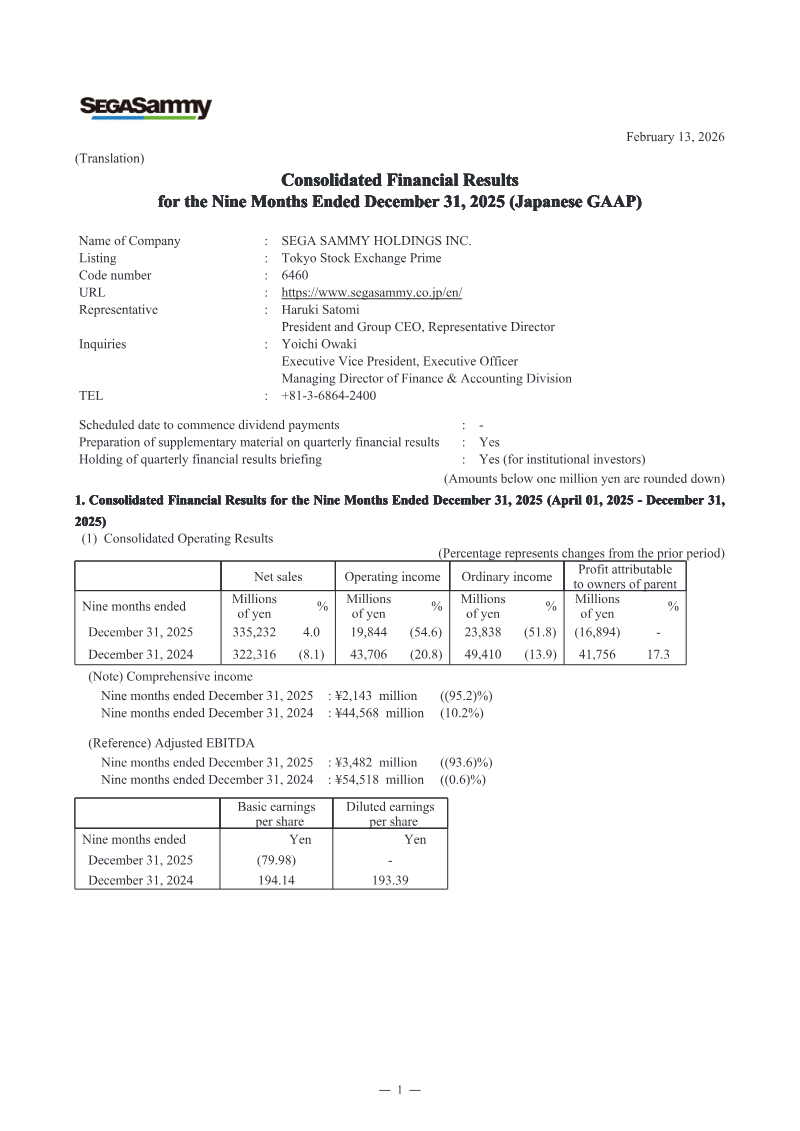

Sega Sammy Holdings · 2026

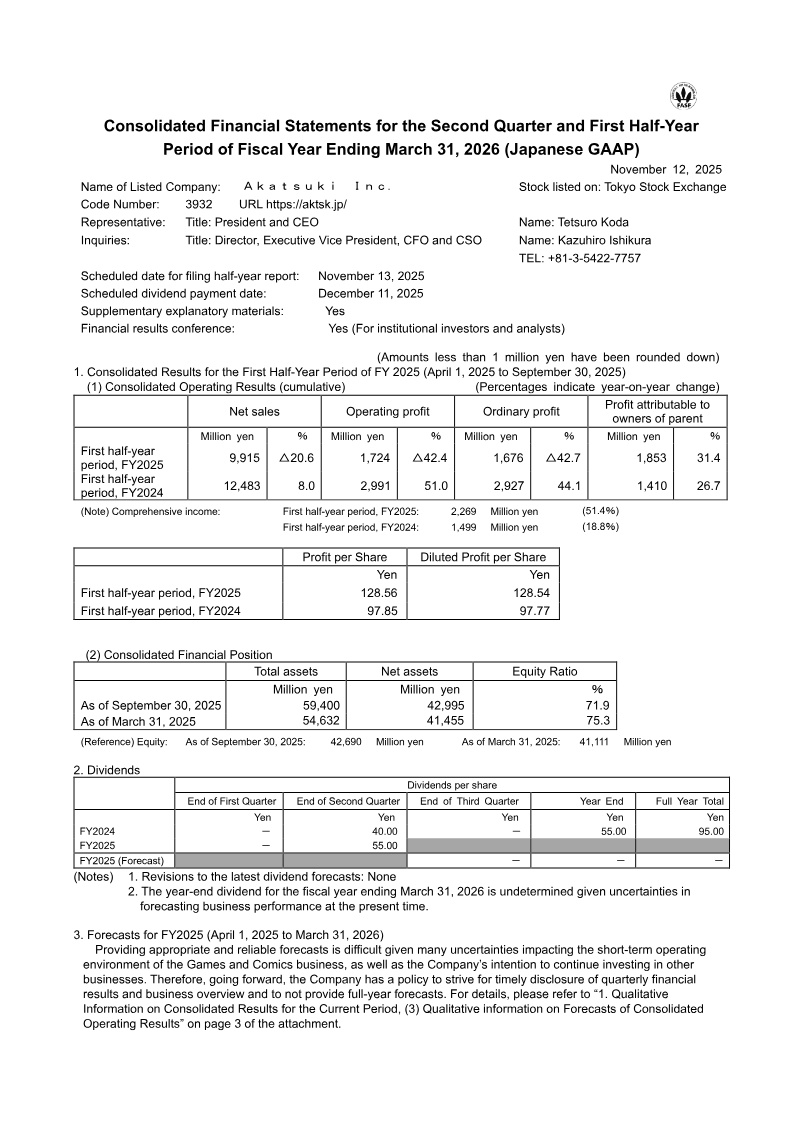

Akatsuki · 2025

Akatsuki · 2025

Akatsuki · 2025

PROEXCA · 2025

CyberAgent · 2025

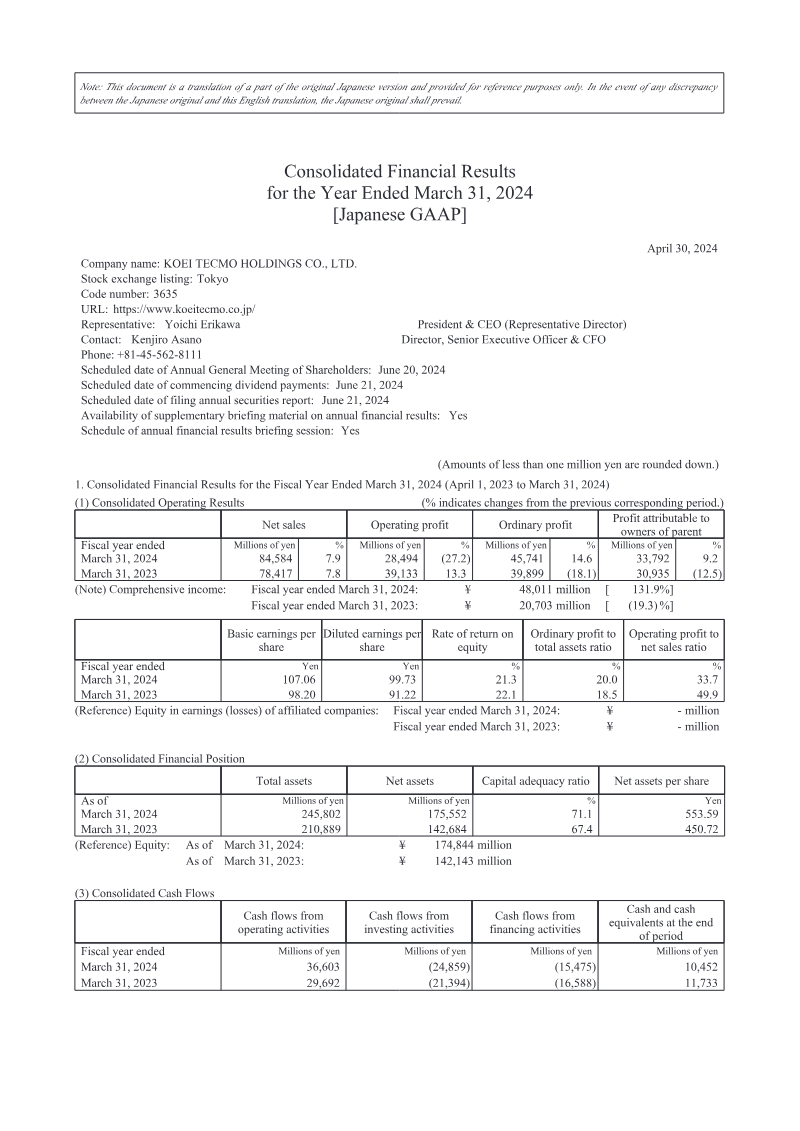

Koei Tecmo · 2025

Koei Tecmo · 2024