Related reports

Legal1 pages

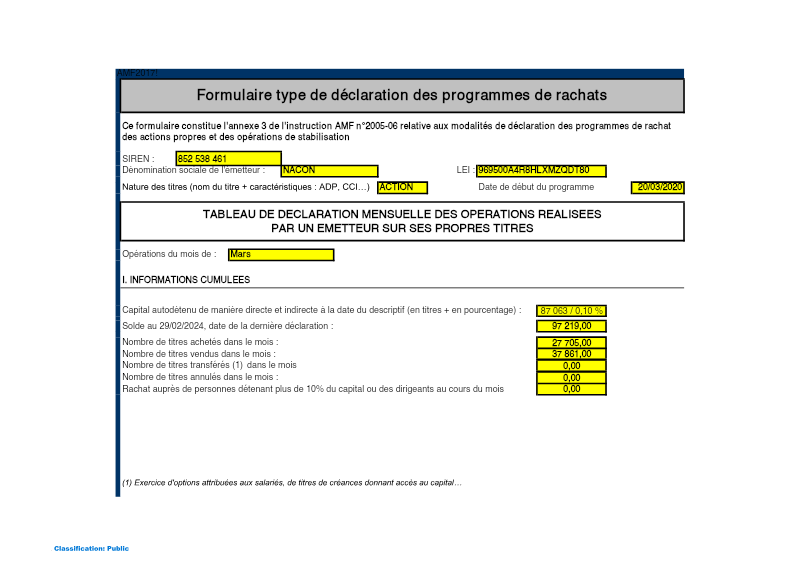

Monthly Disclosure of Share Buyback Operations: March 2024

- As of March 31, 2024, Nacon held 87,063 treasury shares, representing approximately 0.10% of the company's total share capital.

- Nacon executed a net reduction in treasury shares during March 2024, decreasing its holdings from 97,219 shares at the end of February to 87,063 shares.

- The company acquired 27,705 shares and sold 37,861 shares throughout the month of March 2024.

NaconMar 2024

Legal1 pages

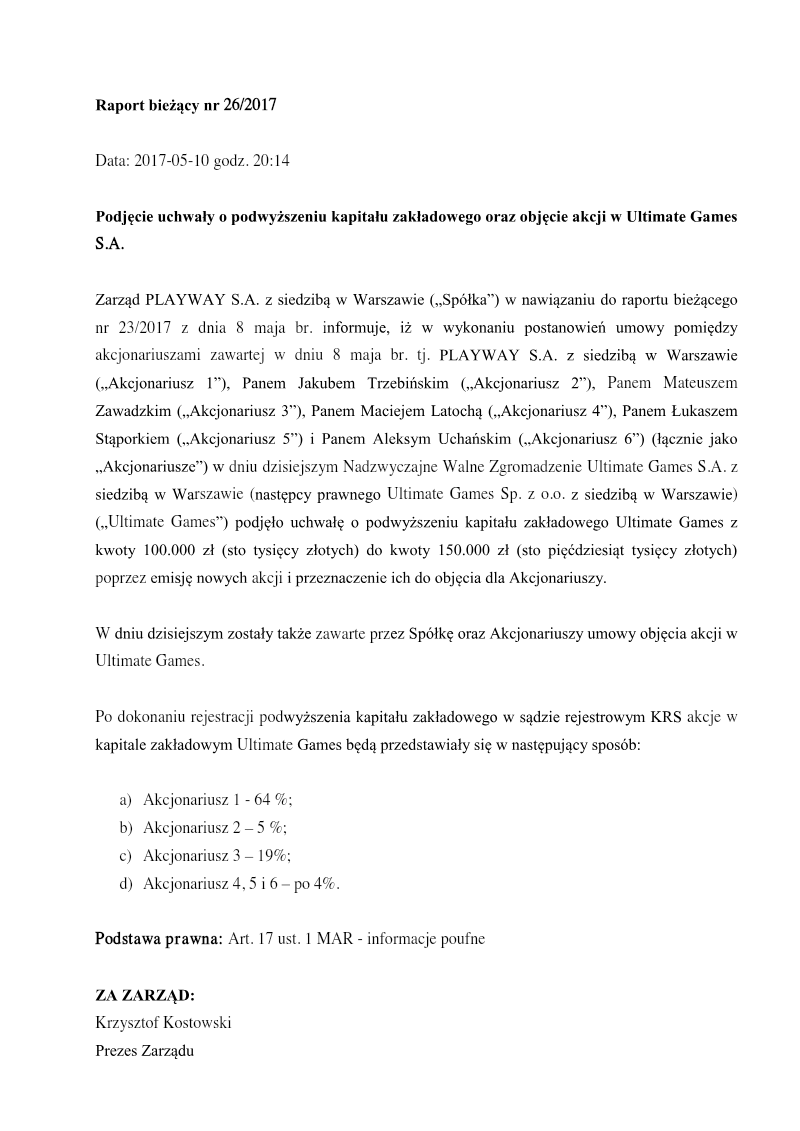

Podjęcie Uchwały o Podwyższeniu Kapitału Zakładowego oraz Objęcie Akcji w Ultimate Games S.A.

- PlayWay S.A. solidified its control over Ultimate Games S.A. by maintaining a 64% majority stake following a corporate restructuring finalized on May 10, 2017.

- Ultimate Games S.A. increased its share capital by 50%, raising the total from 100,000 PLN to 150,000 PLN through the issuance of new shares.

- The capital increase was part of a formal transition for Ultimate Games S.A. from a limited liability company to a joint-stock company.

PlayWayMay 2017

Financial16 pages

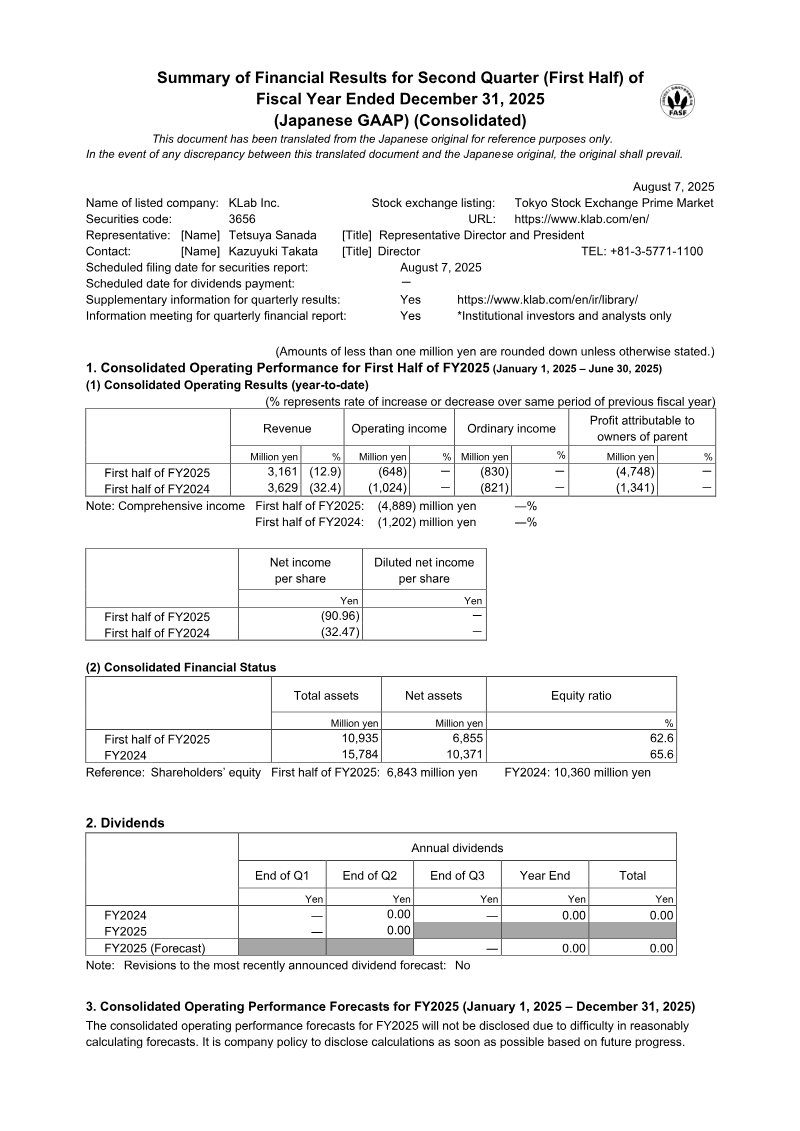

Summary of Financial Results for Second Quarter (First Half) of Fiscal Year Ended December 31, 2025

- KLab Inc. reported a net loss of 4,748 million yen for the first half of fiscal year 2025, driven largely by a 4.43 billion yen impairment charge on software in progress.

- Revenue declined 12.9% year-over-year to 3,161 million yen, while total assets dropped from 15.7 billion yen to 10.9 billion yen.

- The company has suspended interim dividends and declined to provide a full-year financial forecast due to ongoing performance volatility and four consecutive years of operating deficits.

KLabAug 2025

Legal1 pages

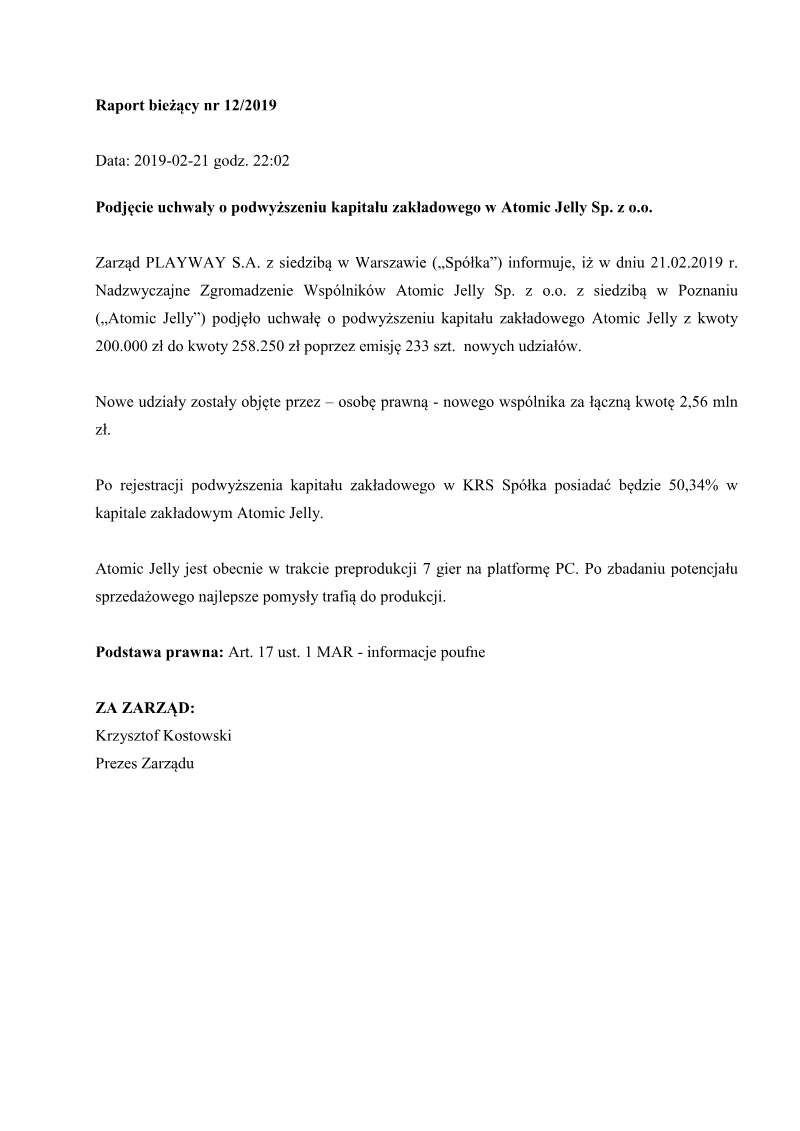

Raport Bieżący Nr 12/2019

- PlayWay S.A. increased the share capital of its subsidiary Atomic Jelly Sp. z o.o. from 200,000 PLN to 258,250 PLN via the issuance of 233 new shares.

- A new investor acquired the 233 new shares for a total investment of 2.56 million PLN, resulting in PlayWay S.A. retaining a 50.34% majority stake in the studio.

- The capital injection is intended to strengthen Atomic Jelly’s financial base to support the development of seven PC titles currently in the pre-production phase.

PlayWayFeb 2019