Key insights

2 takeaways · ~1 min read- 01

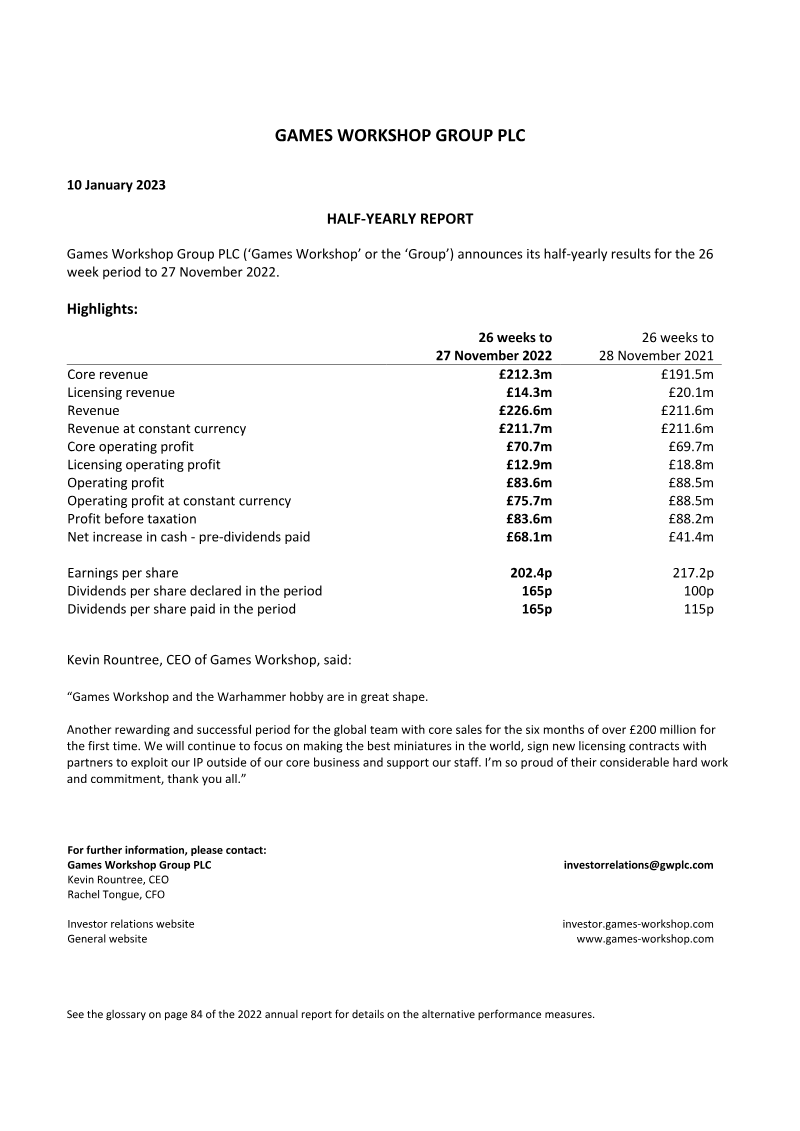

Games Workshop Group PLC reported core revenue of £212.3 million for the 26-week period ending November 27, 2022, an increase from £191.5 million in the same period of 2021.

See it on page 1 - 02

Licensing revenue declined to £14.3 million for the 26 weeks ending November 27, 2022, compared to £20.1 million during the equivalent period in 2021.

See it on page 17

Summary

Games Workshop Group PLC (‘Games Workshop’ or the ‘Group’) announces its half-yearly results for the 26 week period to 27 November 2022. 26 weeks to 26 weeks to 27 November 2022 28 November 2021 Core revenue £212.3m £191.5m Licensing revenue £14.3m £20.1m Revenue ...

Cite this report

Citation

Generating citation...