Related Documents

Financial

Half-Yearly Report: 27 November 2016

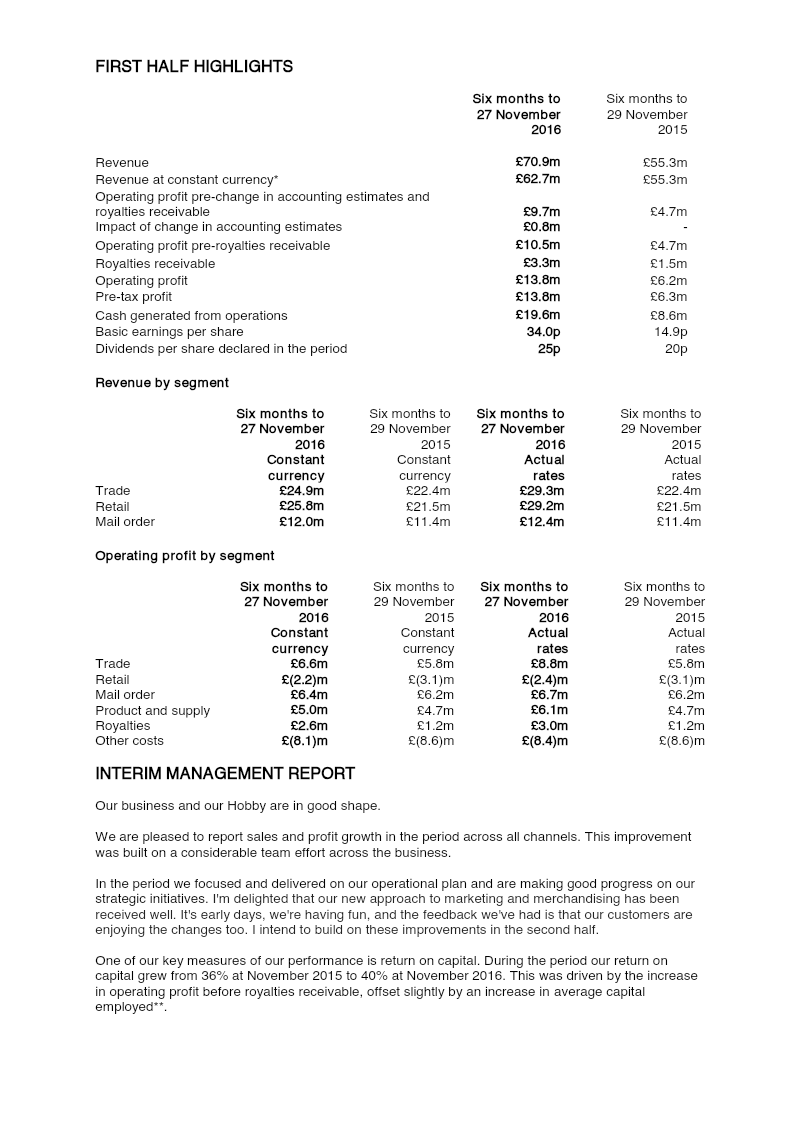

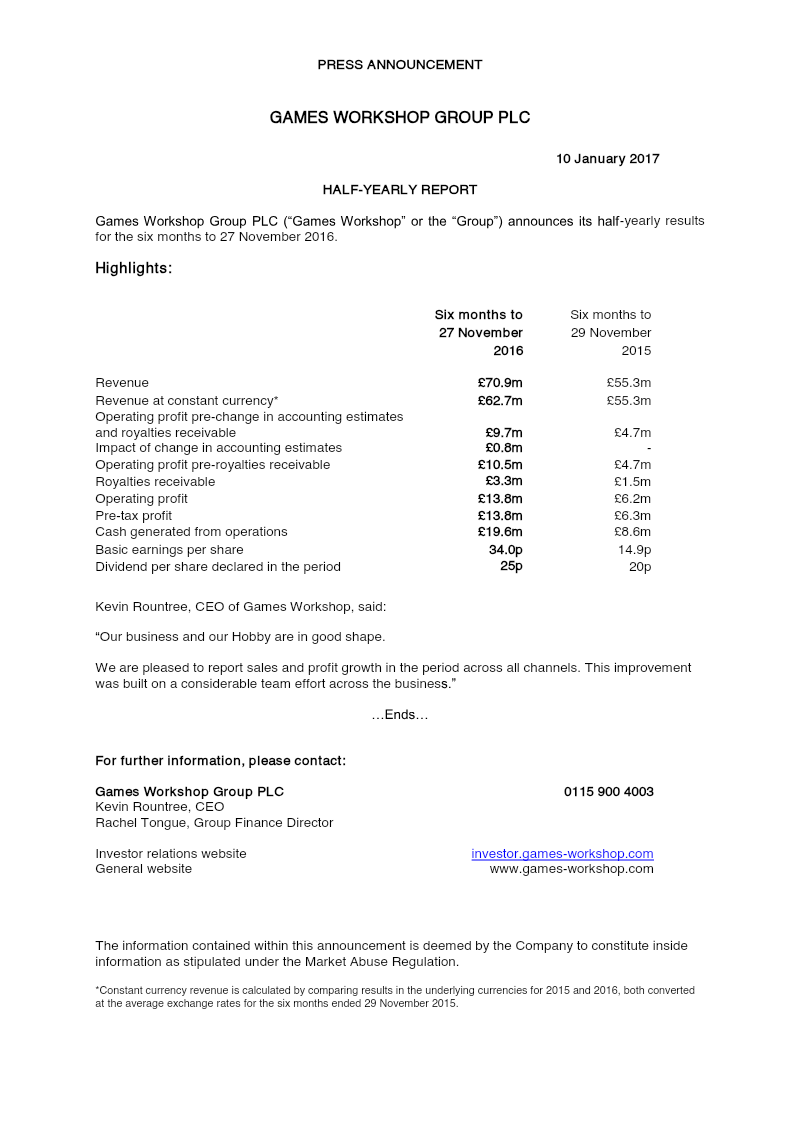

Games Workshop achieved substantial financial growth during the six months ending November 27, 2016, characterized by a 28% increase in revenue to £70.9 million and a more than doubling of pre-tax profit to £13.8 million. This performance reflects broad-based success across all primary sales channels, including Retail, Trade, and Mail Order. A significant driver of this profitability was a 120% surge in royalties receivable, which reached £3.3 million, alongside a robust return on capital of 40%. The period was marked by strong operational cash generation of £19.6 million, allowing for increased dividend payments of 25p per share and continued investment in the business. The financial results were further bolstered by strategic adjustments to accounting estimates regarding the amortization of development costs and the depreciation of moulding tools. These changes, designed to better align expenditures with product revenue cycles, contributed an additional £0.8 million to the operating profit. Consequently, basic earnings per share rose to 34.0p, up from the previous year’s performance. The Group’s net cash position remained healthy, supporting £8.0 million in dividend distributions and £6.8 million in capital investments. The overall trajectory indicates a period of high operational efficiency and market expansion for the tabletop gaming manufacturer. By leveraging strong performance in the Trade and Royalties segments, the company successfully translated increased external revenue into significant bottom-line growth. This fiscal period demonstrates a successful alignment of product development cycles with financial reporting, ensuring that the Group maintains a high level of liquidity while rewarding shareholders through consistent capital returns.

Games Workshop GroupJan 2017

Financial

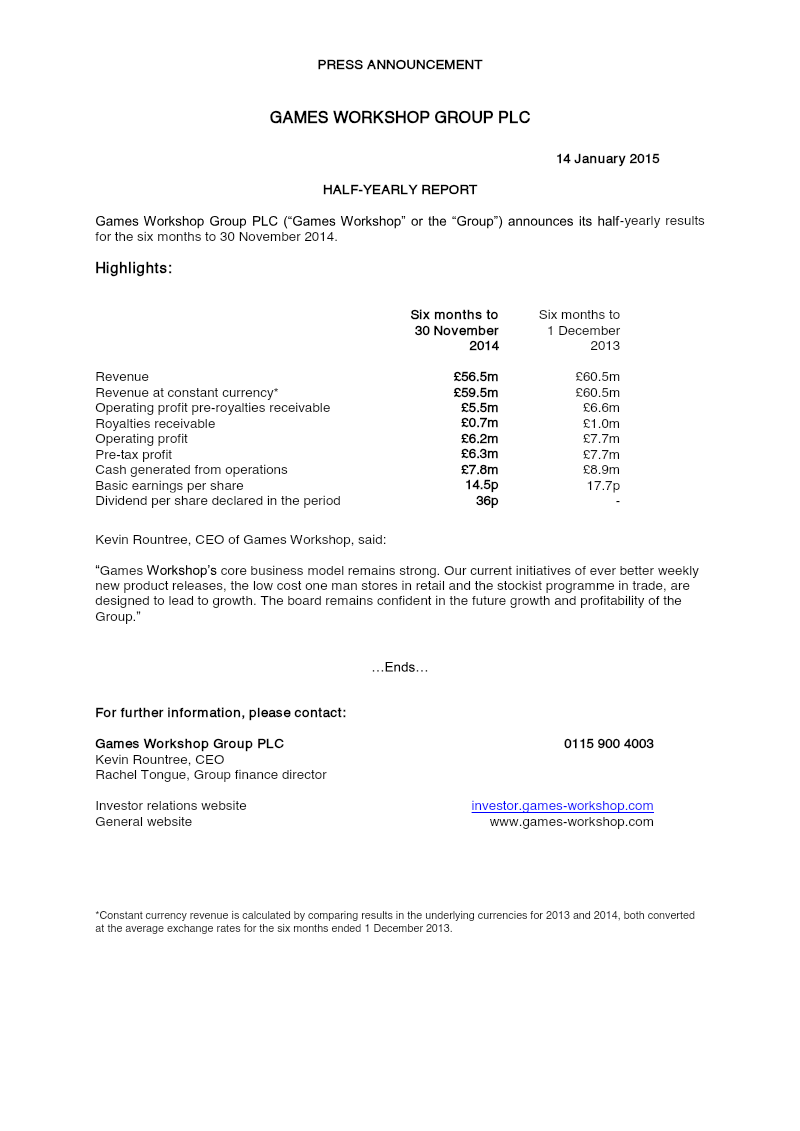

Half-Yearly Report: Six Months to 30 November 2014

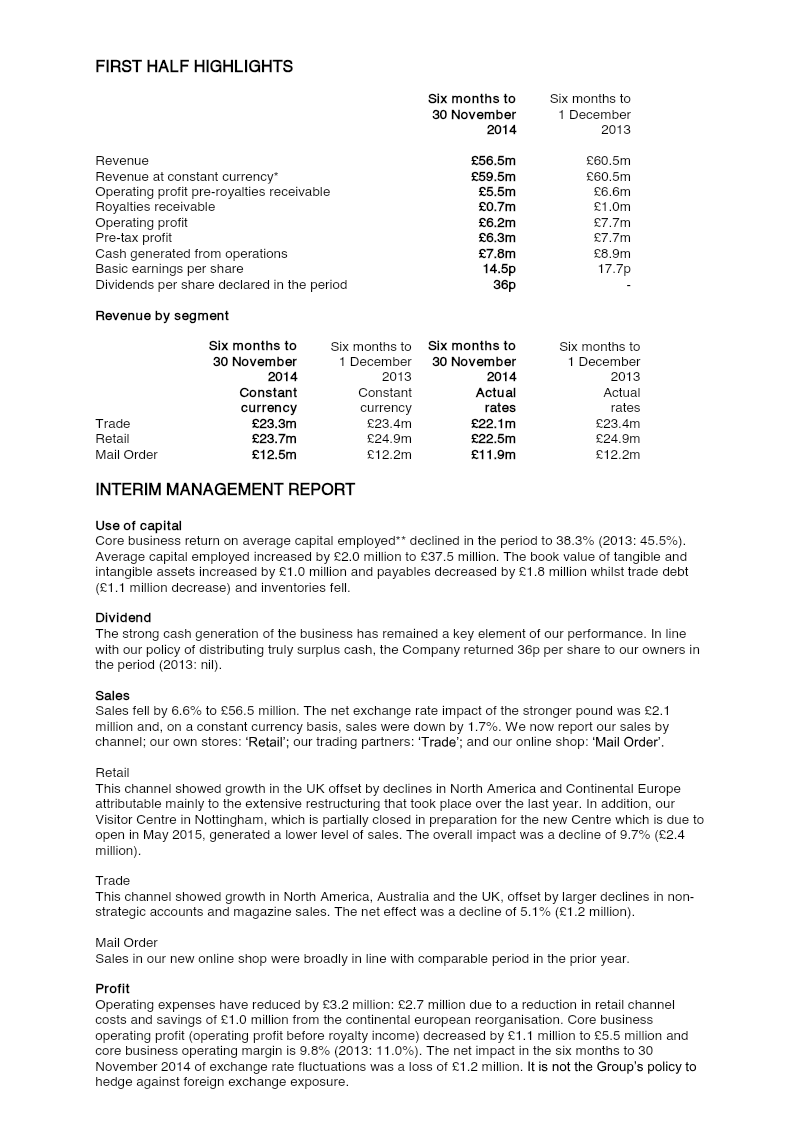

Games Workshop experienced a contraction in financial performance during the six months ending November 30, 2014, characterized by a 6.6% decline in revenue to £56.5 million and a 19% drop in pre-tax profit to £6.3 million. These results reflect a period of significant structural reorganization and the impact of unfavorable currency fluctuations. While the Mail Order segment remained highly profitable, the Retail channel recorded an operating loss of £1.3 million, largely due to redundancy costs and the ongoing transition toward a low-cost, one-man store model. Despite these challenges, the Group maintained sufficient cash generation to issue a dividend of 36p per share, though total cash and cash equivalents decreased by £9.3 million following these distributions. The strategic focus during this period centered on operational efficiency and long-term infrastructure investment. Capital commitments rose to £3.3 million, directed toward enhancing the digital web store and renovating visitor facilities. Intangible assets and physical property reached a combined net book value of nearly £30 million following steady investment in production and intellectual property. Furthermore, the Group successfully reduced its total provisions from £3.53 million to £1.85 million as it utilized funds previously set aside for exceptional restructuring items. Management remains focused on a high-frequency product release cycle to drive future growth, leveraging weekly launches to maintain consumer engagement. Although the retail landscape faced headwinds during the first half of the fiscal year, the stabilization of the store footprint and the utilization of seasonal sales peaks in December are expected to bolster the Group’s position. The transition toward a leaner retail estate and improved digital integration serves as the primary mechanism for recovering margins and ensuring long-term sustainability across global trade and retail channels.

Games Workshop GroupJan 2015

Financial

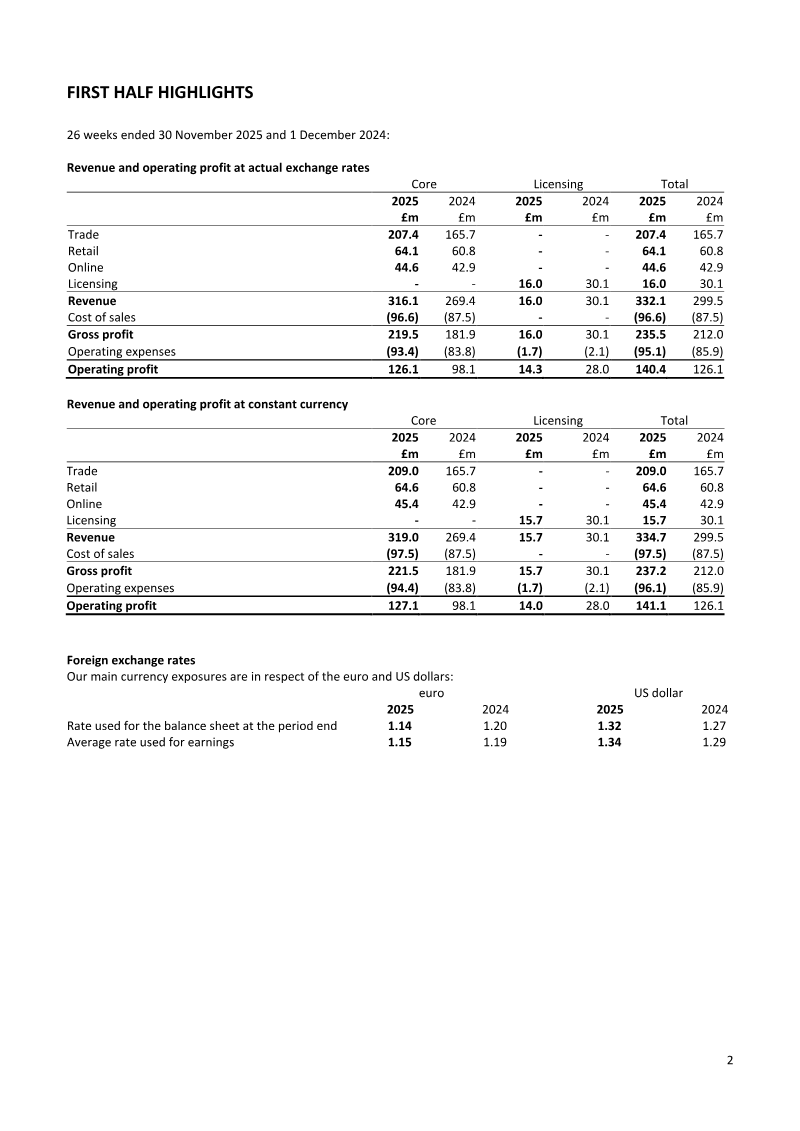

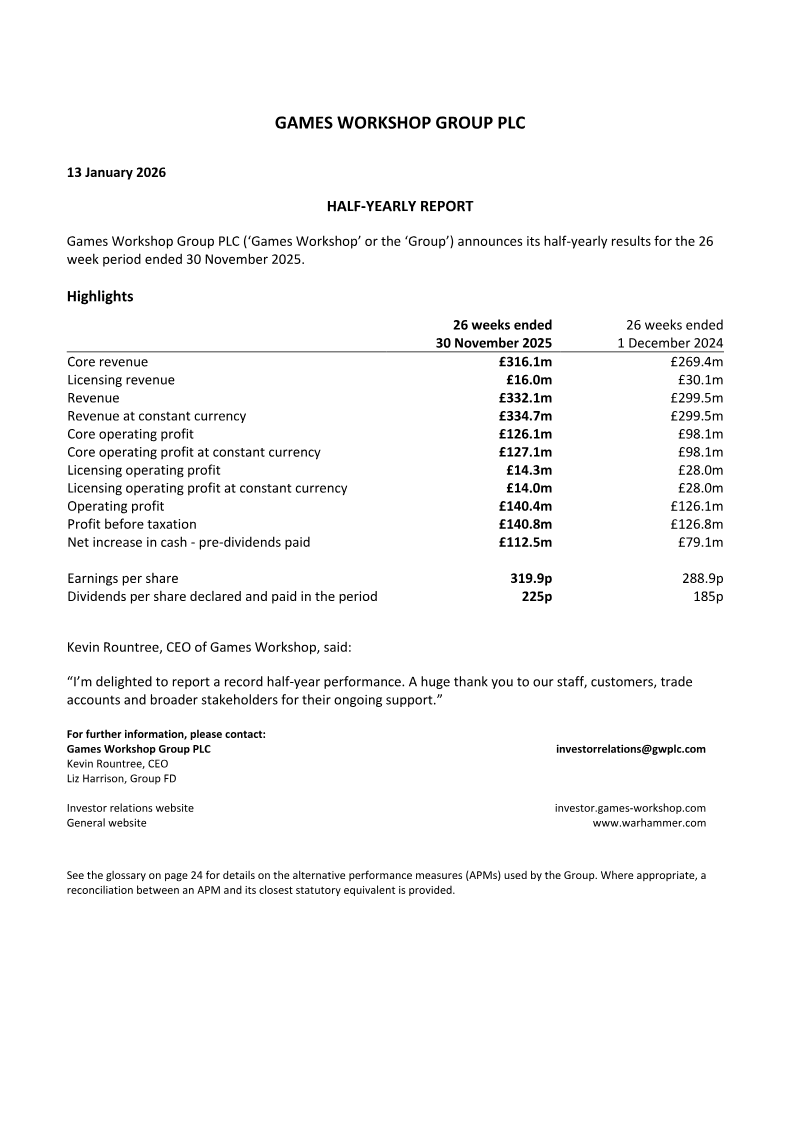

Half-Yearly Report: 26 Weeks Ended 30 November 2025

Games Workshop achieved record financial performance for the 26-week period ending November 30, 2025, characterized by robust core revenue growth and significant operational expansion. Total revenue rose to £332.1 million, a 10.9% increase over the previous year, while profit before tax climbed to £140.8 million. This growth was primarily fueled by the core business, particularly the trade channel, which saw a 25.2% increase to £207.4 million. High-profile product launches, including the record-breaking Space Wolves army box and new iterations for Horus Heresy and Age of Sigmar, underpinned this success. While core operations flourished, licensing revenue experienced a contraction, falling from £30.1 million to £16.0 million. This decline is attributed to high prior-year comparatives following the major release of Space Marine 2, though long-term media prospects remain strong through ongoing development with Amazon MGM Studios. To protect margins against external pressures, such as £6.0 million in US tariff costs, the company implemented a 3.5% price increase and achieved a gross margin of 69.4%. Management also reaffirmed a strict policy against utilizing artificial intelligence in creative processes to preserve the brand's artistic integrity. The company is aggressively investing in its global infrastructure to support future demand, with a fourth factory scheduled for 2026 and a robotic warehouse in the UK planned for 2027. Digital engagement continues to scale, with Warhammer+ reaching 248,000 subscribers and active digital users nearing 800,000. Supported by a strong cash position of £171.1 million and a global retail footprint of 575 stores, the Group remains a highly liquid going concern, returning £74.2 million to shareholders in dividends while maintaining progress toward its 2032 carbon emission targets.

Games Workshop GroupJan 2025

Financial

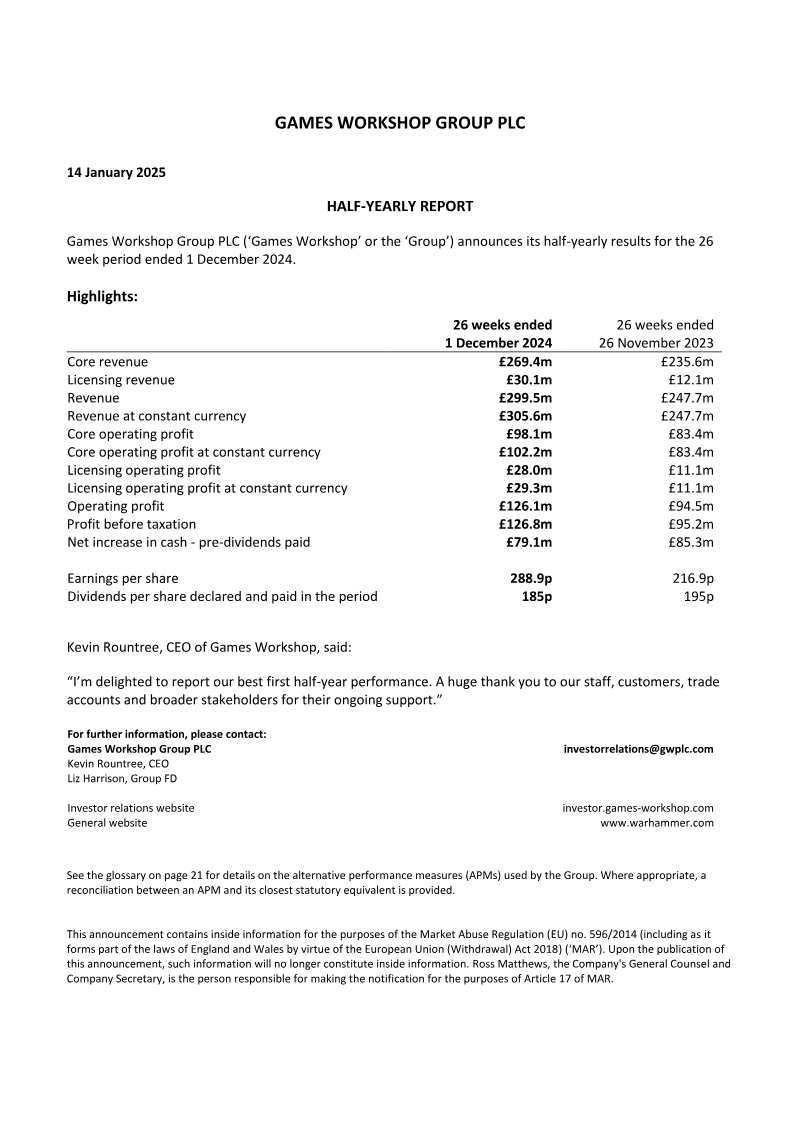

Half-Yearly Report: 26 Week Period Ended 1 December 2024

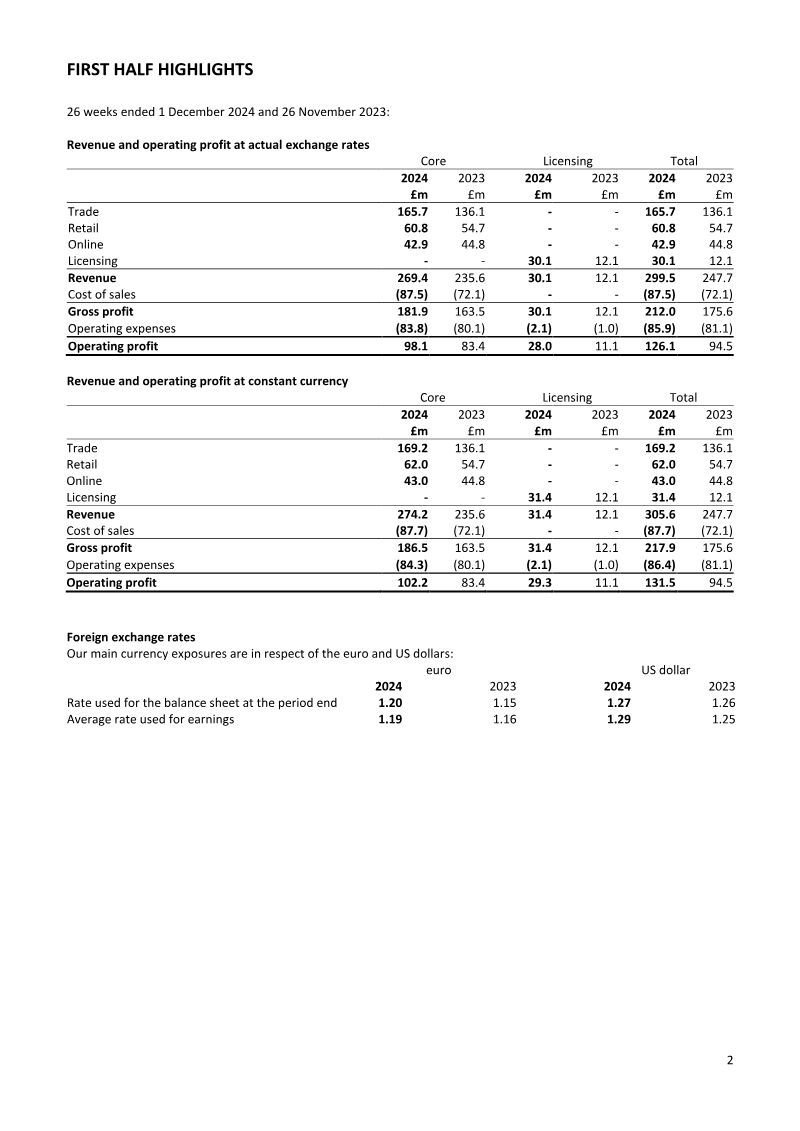

Games Workshop achieved record-breaking financial results for the 26-week period ended December 1, 2024, characterized by substantial growth in both core operations and intellectual property monetization. Total revenue reached £299.5 million, a significant increase from £247.7 million in the prior year, while profit before taxation rose to £126.8 million. This performance was underpinned by a 14.3% rise in core revenue, primarily driven by the Trade channel, which contributed £165.7 million. Licensing income experienced a dramatic surge, rising from £12.1 million to £30.1 million, largely due to the commercial success of the video game Space Marine 2 and the finalization of a major media deal with Amazon for film and television adaptations. Geographic expansion remains a central strategic pillar, with a particular focus on North America and Asia. The company is on track to reach 200 profitable stores in North America by May 2025 and has identified over 30 potential locations for development in Japan over the next five years. While physical retail and trade channels showed robust growth across the UK, Europe, and North America, online sales saw a slight decline of 4.2% against difficult year-on-year comparisons. To support this global scale, capital investment increased to £14.3 million, directed toward expanding manufacturing and warehousing capacity in the UK, North America, and Australia, alongside critical upgrades to IT infrastructure. The financial position remains strong with a net cash balance of £125.8 million, even after the distribution of £61 million in dividends. Despite these record results, the outlook includes careful monitoring of external risks such as potential US tariffs and ongoing cost inflation. Leadership transitions, including the appointment of a new Group Finance Director and Non-Executive Chair, coincide with a period of high digital engagement across community platforms and subscription services. The vertically integrated business model continues to demonstrate resilience, successfully converting increased global demand for the Warhammer brand into significant shareholder value.

Games Workshop GroupJan 2025