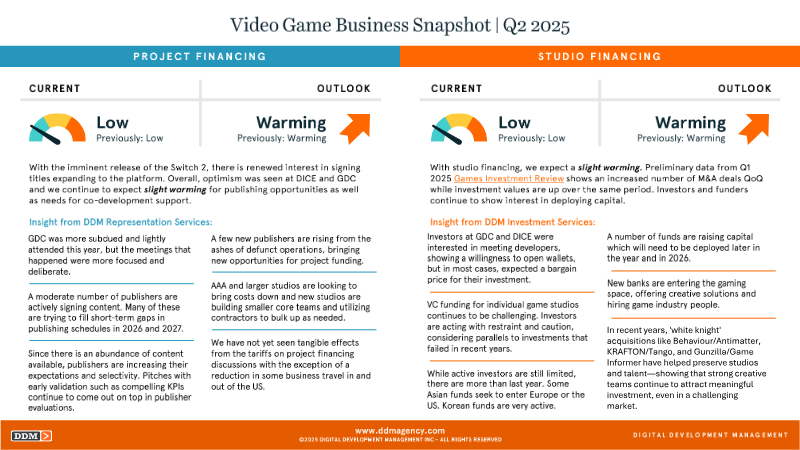

Q2 2025 is defined by a surge in 'white knight' acquisitions, where major conglomerates are purchasing studios facing closure or downsizing to preserve creative talent and intellectual property.

Notable rescue acquisitions this quarter include KRAFTON’s purchase of Tango Gameworks, Behaviour Interactive’s absorption of Antimatter, and Gunzilla Games’ involvement with Game Informer.

The industry is shifting away from speculative growth toward strategic preservation, as large publishers prioritize securing proven development teams to stabilize long-term production pipelines.

Despite a contraction in traditional venture capital and broader economic volatility, experienced human capital remains a high-value asset driving deal flow.

The current market environment is trending toward a more consolidated industry structure, where the survival of independent creative hubs is increasingly dependent on the strategic interests of larger market players.

The second quarter of 2025 highlights a strategic shift in the video game industry’s mergers and acquisitions landscape, characterized by a rise in rescue-style investments often referred to as white knight acquisitions. These transactions involve established global entities stepping in to acquire studios or media outlets that might otherwise face closure or significant downsizing. Notable examples include KRAFTON’s acquisition of Tango Gameworks, Behaviour Interactive’s absorption of Antimatter, and Gunzilla Games’ involvement with Game Informer. These moves suggest that despite broader economic volatility and a contraction in traditional venture capital, high-quality creative talent and established intellectual properties remain highly valuable assets for diversified gaming conglomerates.

The current market environment reflects a transition where strategic preservation is prioritized over speculative growth. Large-scale publishers are increasingly focused on securing proven development teams to bolster their long-term pipelines, viewing these acquisitions as opportunities to integrate specialized expertise at a time when independent sustainability is difficult. This trend underscores a broader industry sentiment that while the capital market remains challenging, the underlying value of experienced human capital continues to drive significant deal flow. These developments indicate that the industry is moving toward a more consolidated but stable structure, where the survival of key creative hubs is facilitated by the strategic interests of larger market players.