Back to Library

Report

Consolidated Financial Results for the Six Months Ended September 30, 2024

By mixi

12 pages3,595 words

Summary

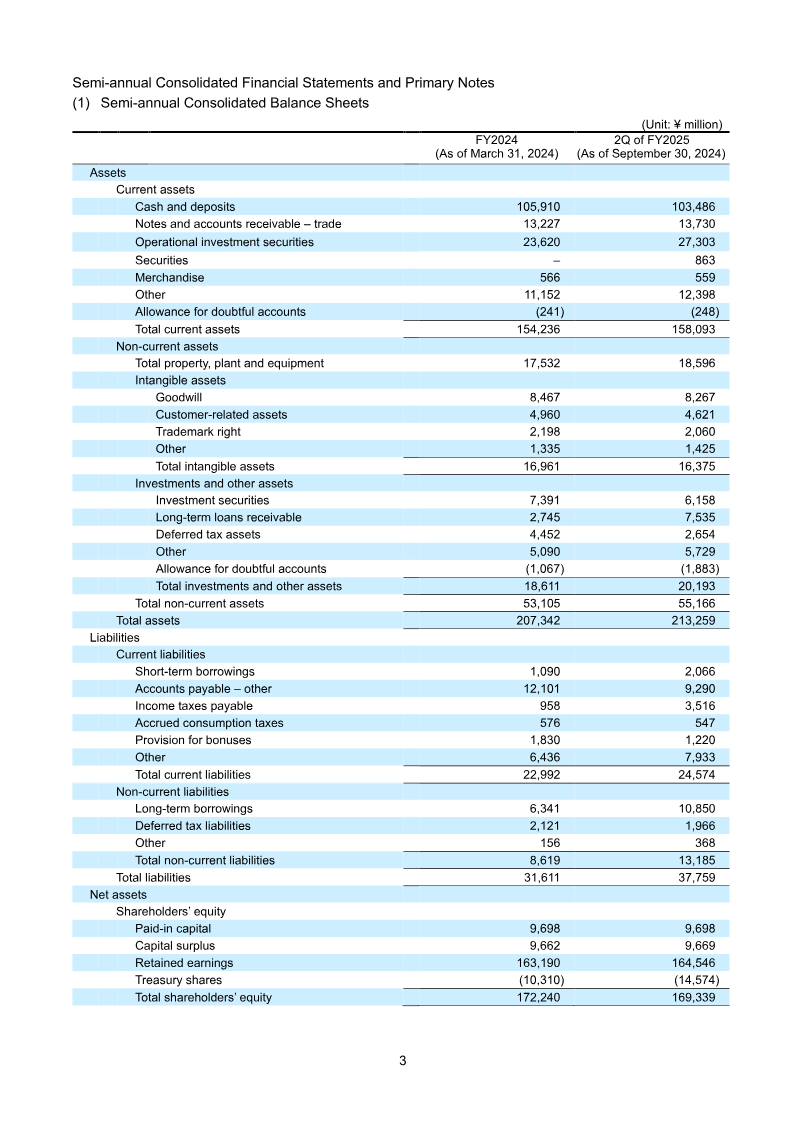

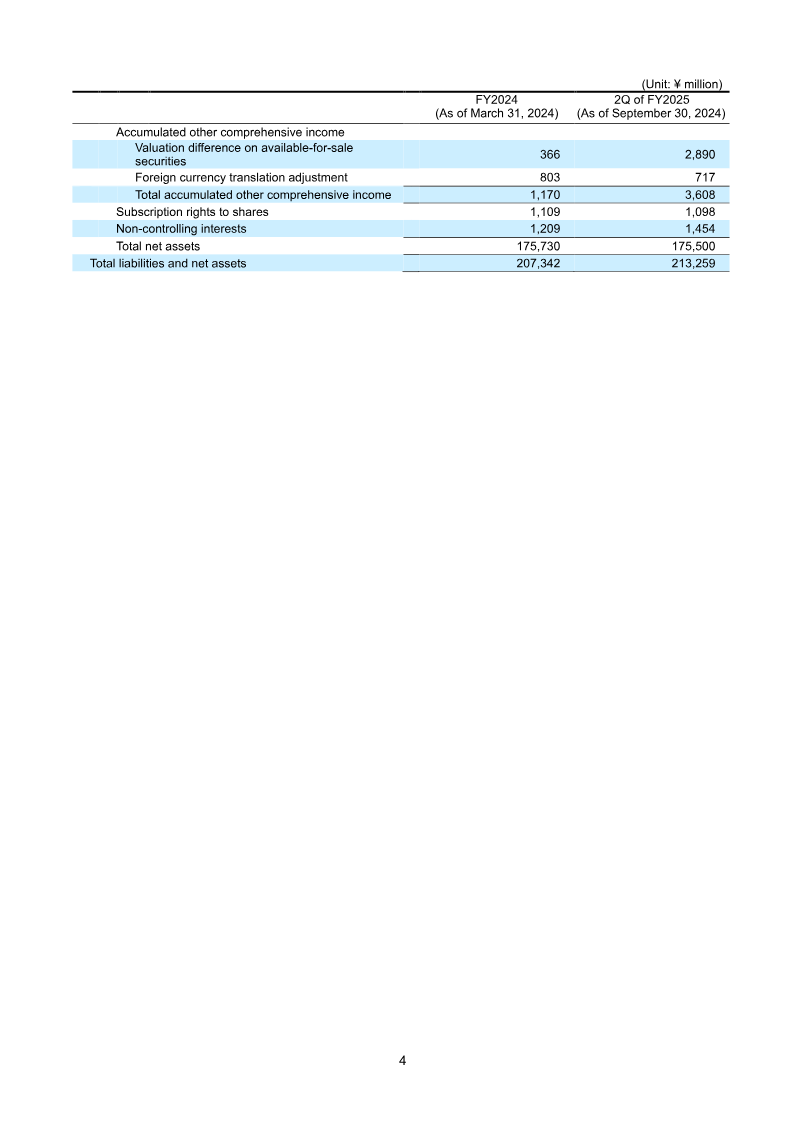

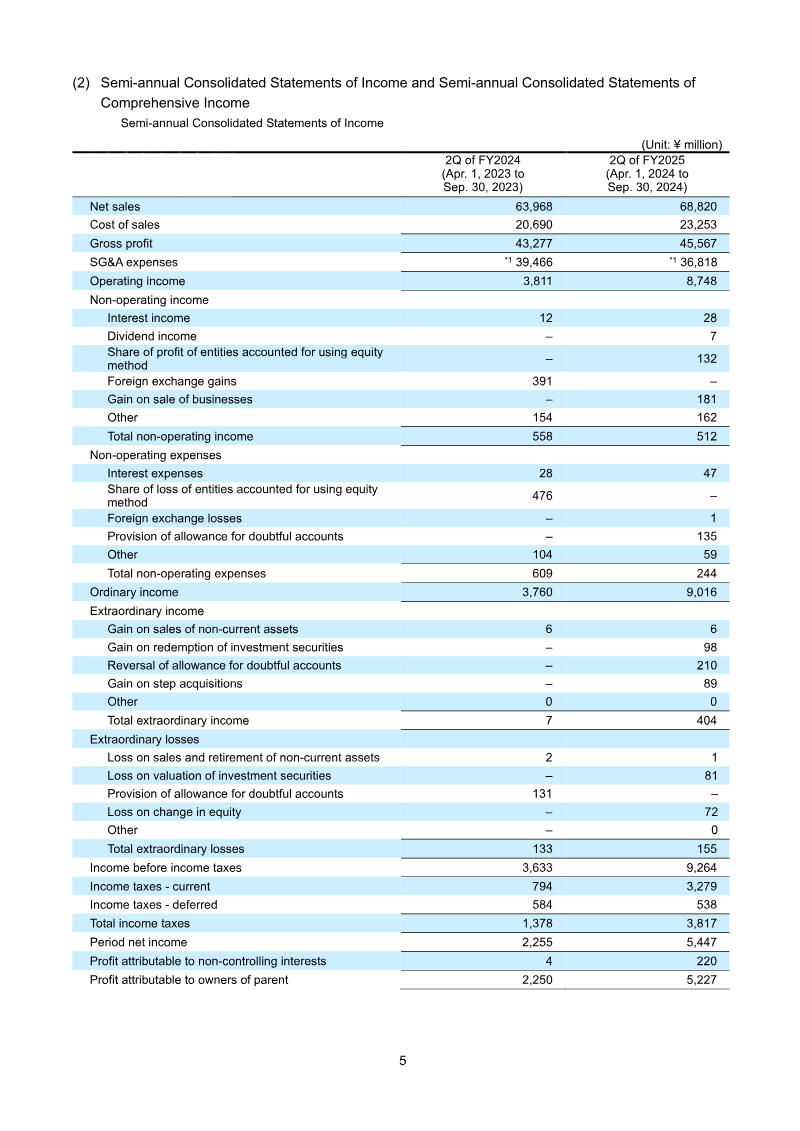

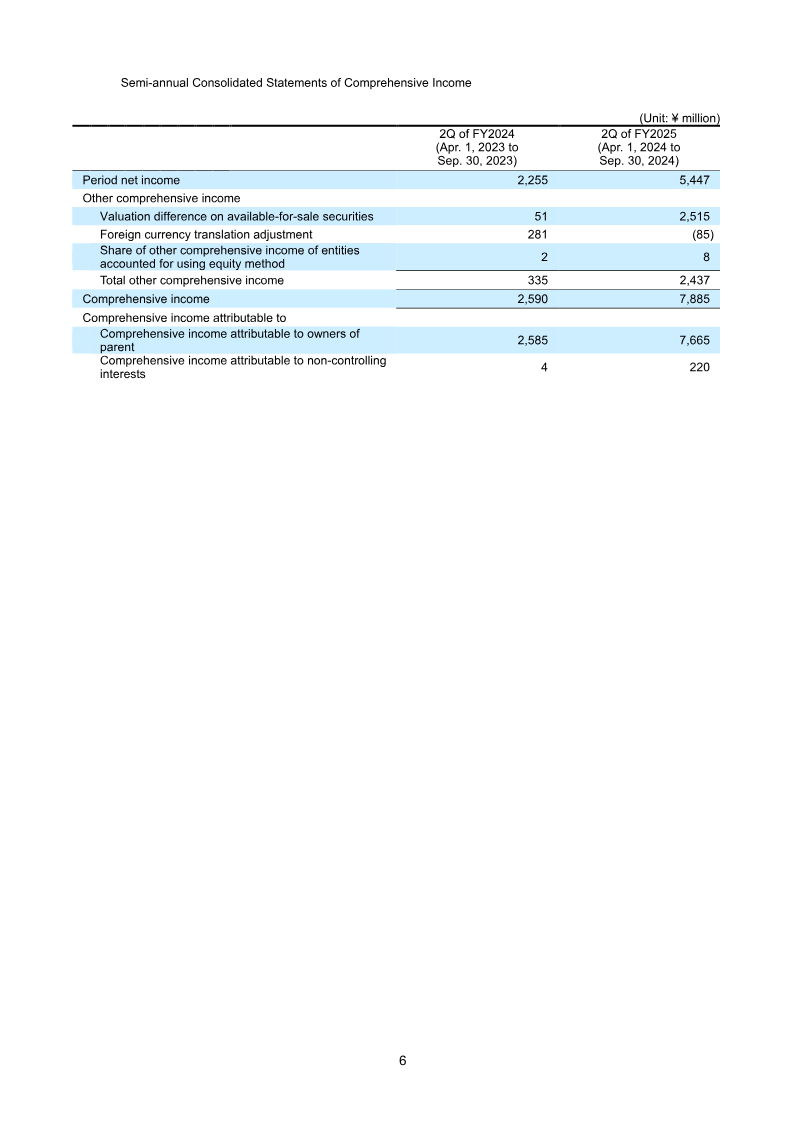

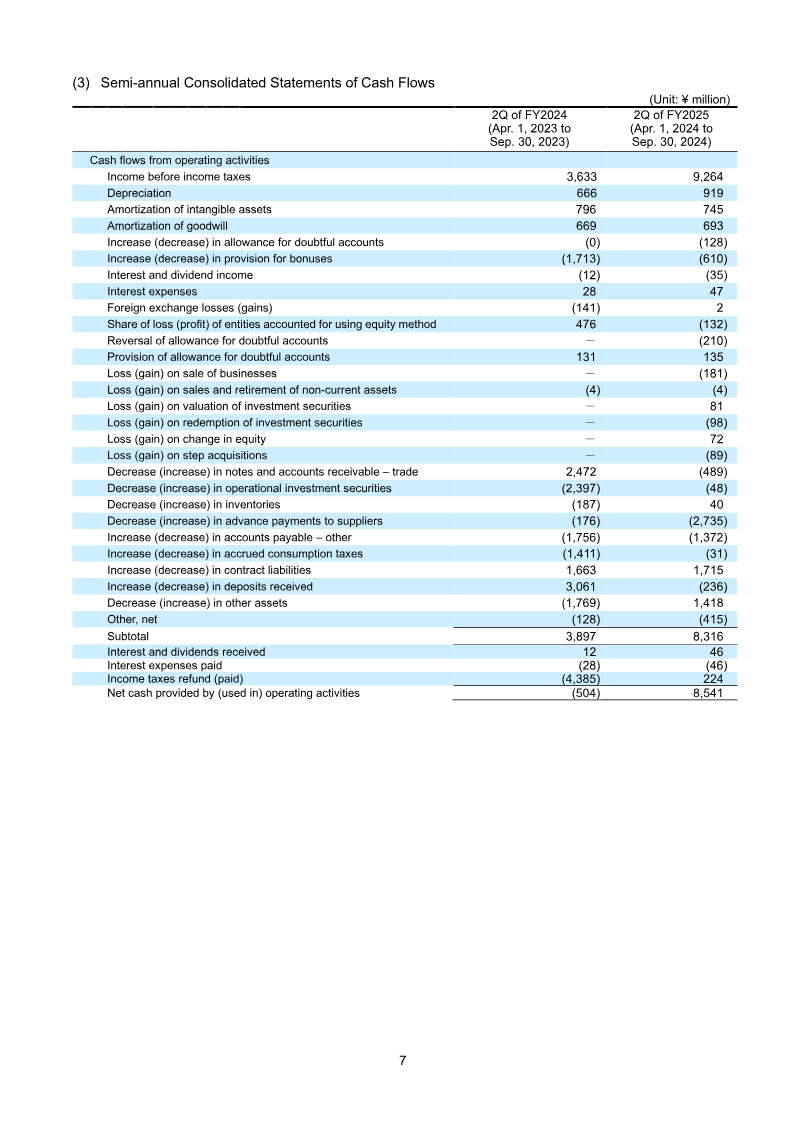

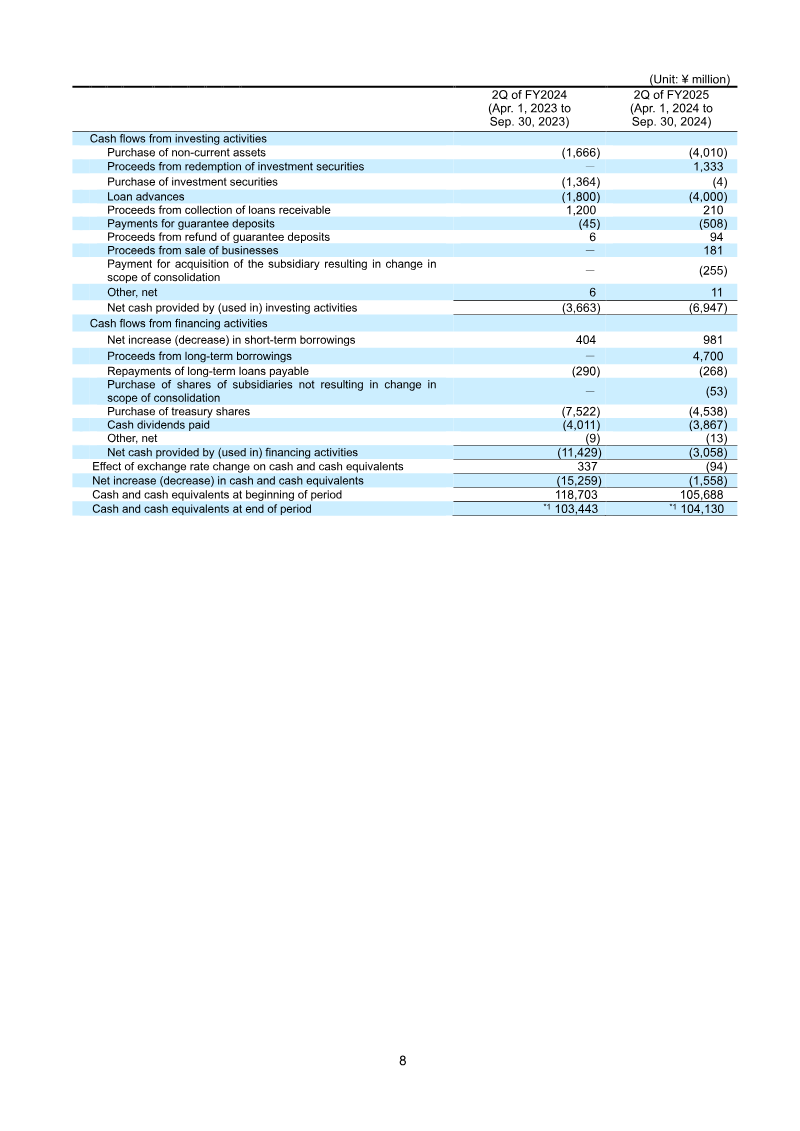

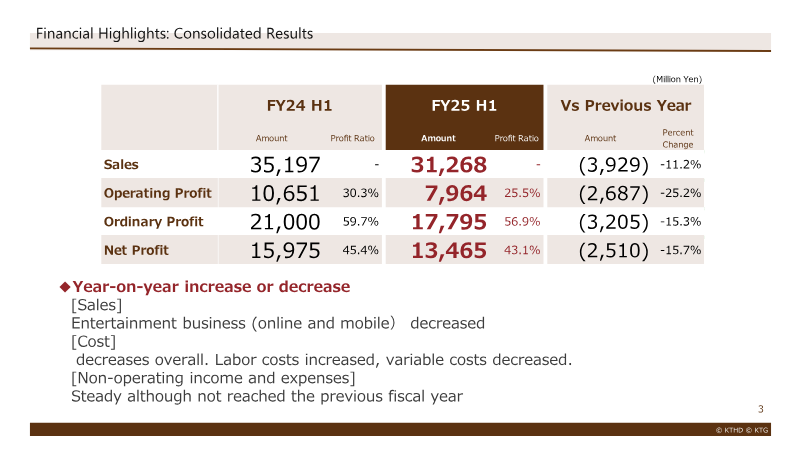

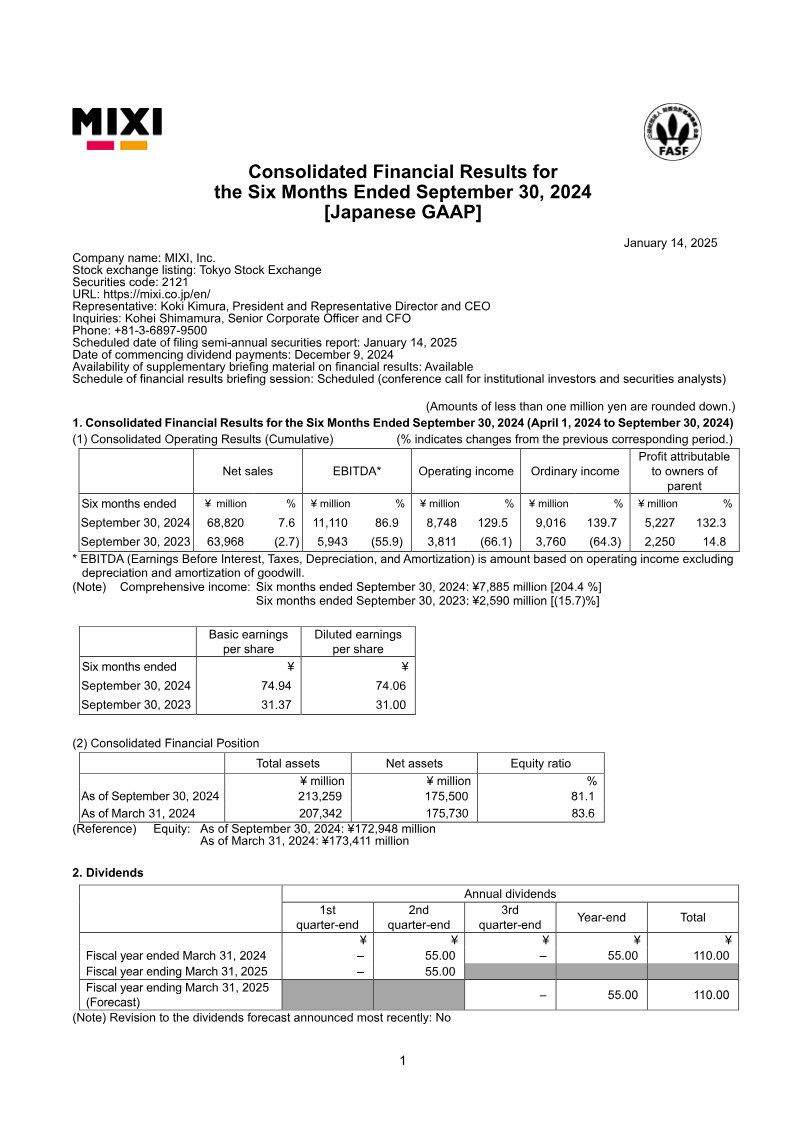

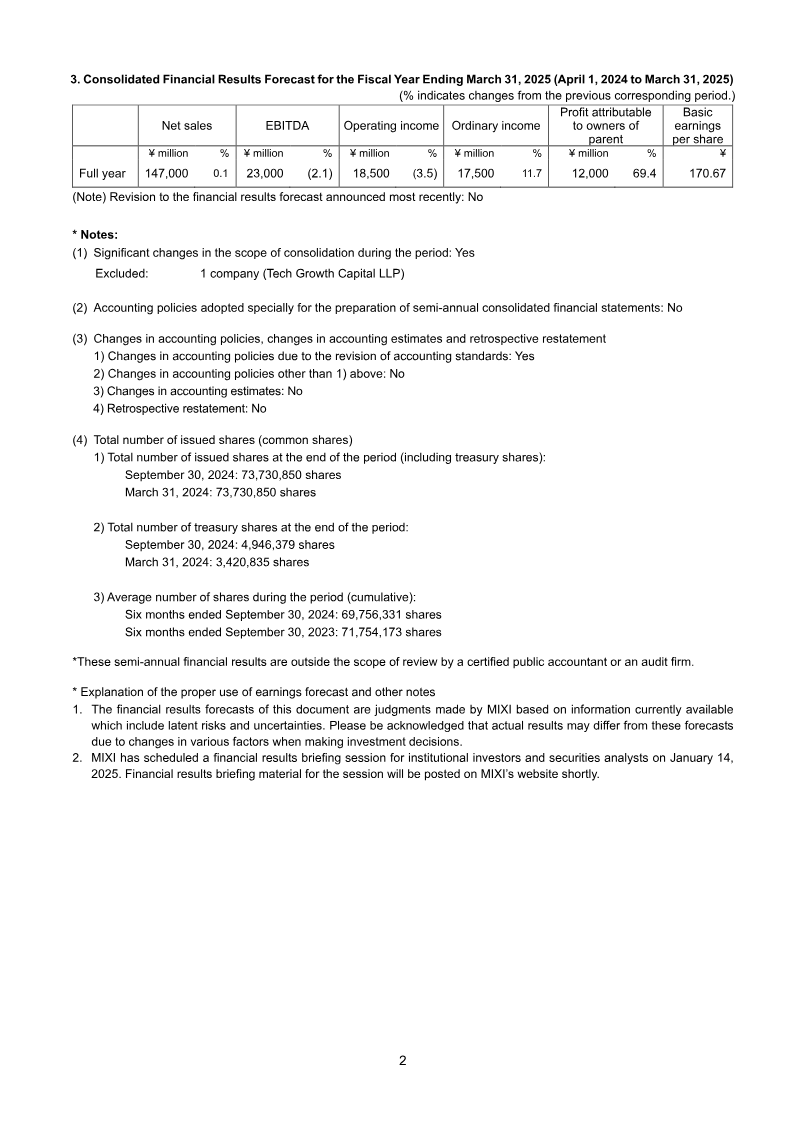

MIXI, Inc. reports a strong six‑month performance for April 1 to September 30 2024, with net sales rising 7.6 % to ¥68.8 billion and operating income increasing 129.5 % to ¥8.75 billion, driven largely by its Digital Entertainment segment featuring Monster Strike. EBITDA surged 86.9 % to ¥11.1 billion, and ordinary income attributable to owners of the parent climbed 139.7 % to ¥9.02 billion, reflecting improved profitability and cost management. Comprehensive income for the period reached ¥7.9 billion, a 204.4 % increase over the prior year, largely due to gains on available‑for‑sale securities and foreign currency translation adjustments. Basic earnings per share rose from ¥31.4 to ¥74.9, while diluted EPS increased similarly. Total assets grew to ¥213.3 billion, with net assets at ¥175.5 billion and an equity ratio of 81.1 %. Treasury share repurchases increased, raising treasury shares to ¥14.6 billion and reducing retained earnings by ¥13.7 billion during the period. Cash flow from operating activities turned positive, generating ¥8.5 billion in net cash, offset by significant investing outflows for non‑current assets and a substantial purchase of treasury shares. The company forecasts full‑year 2025 results with net sales at ¥147 billion, operating income of ¥18.5 billion, and ordinary income of ¥17.5 billion, projecting a 3.5 % decline in operating income versus the prior year but maintaining robust profitability. No material accounting policy changes are expected to affect these forecasts. The report covers Japan‑based operations under Japanese GAAP for the first half of FY 2025, with a focus on digital entertainment and related services.

Tags

Pages

View all

Citation

Citation

Generating citation...

Similar Documents

Report

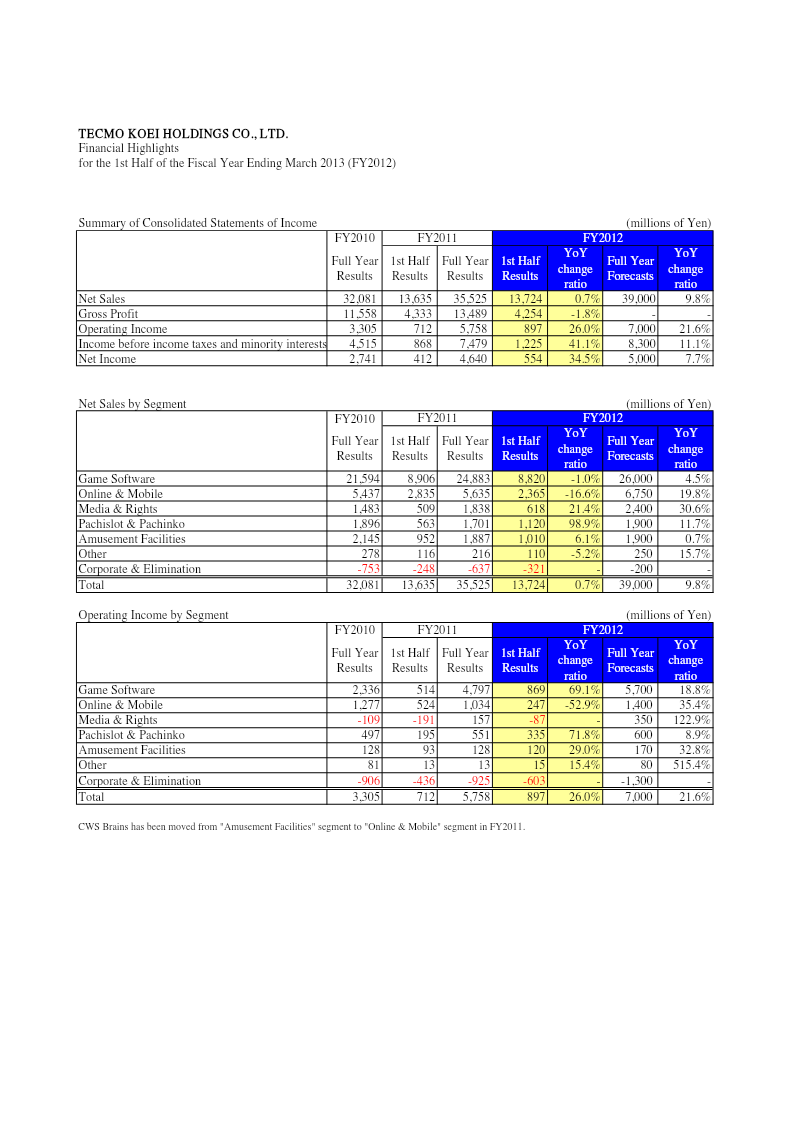

Financial Highlights: 1st Half of FY2013

Financial highlights for the first half of fiscal year 2012 (ending March 2013) show a modest increase in consolidated net sales of 0.7 % to ¥13,724 million compared with the same period in FY2011, while full‑year sales for FY2012 were forecast at ¥39 000 million, up 9.8 % from FY2011. Gross profit rose 1.8 % to ¥4,254 million, and operating income surged 26.0 % to ¥897 million, reflecting a strong rebound in the Game Software and Pachislot & Pachinko segments. Income before taxes increased 41.1 % to ¥1,225 million, and net income grew 34.5 % to ¥554 million, both well above the 7.7 % forecasted growth. Segment analysis reveals that Game Software sales declined slightly by 1.0 % to ¥8,820 million but operating income from this segment jumped 69.1 % to ¥869 million, driven by higher gross margins. Online & Mobile sales fell 16.6 % to ¥2,365 million; operating income from this segment dropped 52.9 % to ¥247 million, partly due to the relocation of CWS Brains from Amusement Facilities to Online & Mobile in FY2011. Media & Rights sales increased 21.4 % to ¥618 million, with operating income turning positive at ¥157 million after a loss of ¥191 million the previous year. Pachislot & Pachinko sales rose 98.9 % to ¥1,120 million, with operating income up 71.8 %. Amusement Facilities and Other segments showed modest growth in sales (6.1 % and –5.2 %, respectively) but maintained stable operating income. The data cover the Japanese market, covering all business segments of Tecmo Koei Holdings. Figures are presented in millions of yen and compare FY2010, FY2011, and FY2012 results with forecasts for the full year. The report relies on consolidated financial statements prepared under Japanese GAAP, providing a comprehensive view of the company’s performance during the first half of FY2012.

Koei Tecmo

Report

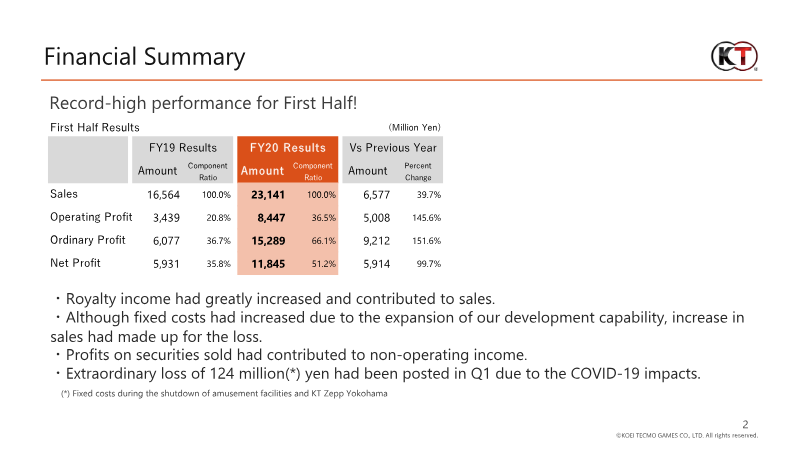

Financial Results for the First Half of the Fiscal Year Ending March 2021

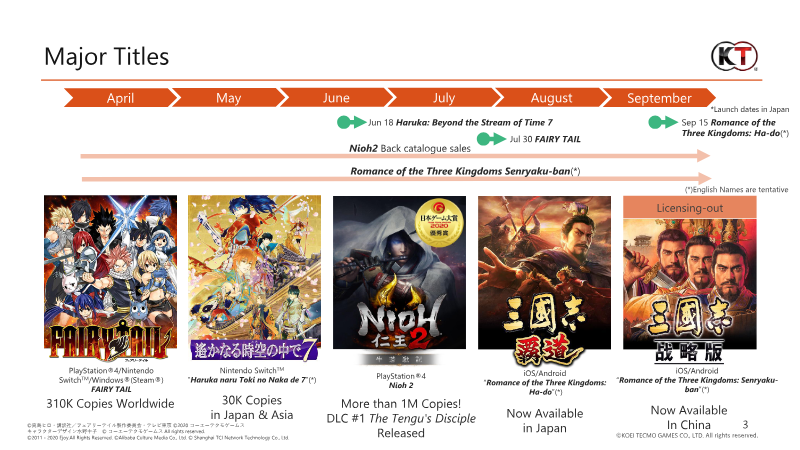

The first‑half financial results for the fiscal year ending March 2021 demonstrate a record‑setting performance, with sales rising 39.7 % to ¥23.141 billion and operating profit increasing 145.6 % to ¥8.447 billion. Net profit nearly doubled, reaching ¥11.845 billion, driven largely by a sharp rise in royalty income and gains from securities sales. Fixed costs expanded due to development‑capability growth, but the higher revenue offset these expenses; an extraordinary loss of ¥124 million in Q1 was attributed to COVID‑19 shutdowns of amusement facilities and the KT Zepp Yokohama venue. Segment analysis shows entertainment sales accounting for 93 % of total revenue, with a 45.8 % increase to ¥21.683 billion. Amusement and real‑estate segments experienced modest declines, while other operating profits fell by 18 %. Geographic revenue shifted toward overseas markets: overseas sales grew from ¥5.814 billion to ¥11.609 billion, representing 50.2 % of total sales, and overseas units sold rose by 99.7 %. Digital sales declined overall, with a 42.2 % drop in console units and a 50.4 % reduction in digital copies, reflecting the impact of pandemic‑related store closures. The company’s FY 2020 full‑year plan targets ¥51 billion in sales and ¥17 billion in operating profit, an upward revision from the mid‑term plan. Planned capital expenditures focus on real‑estate expansion and new office facilities, while a 50 % dividend payout policy is maintained. Overall, the results underscore strong IP licensing performance, robust back‑catalogue sales, and a strategic shift toward higher overseas revenue streams.

Koei Tecmo