FinancialKLab

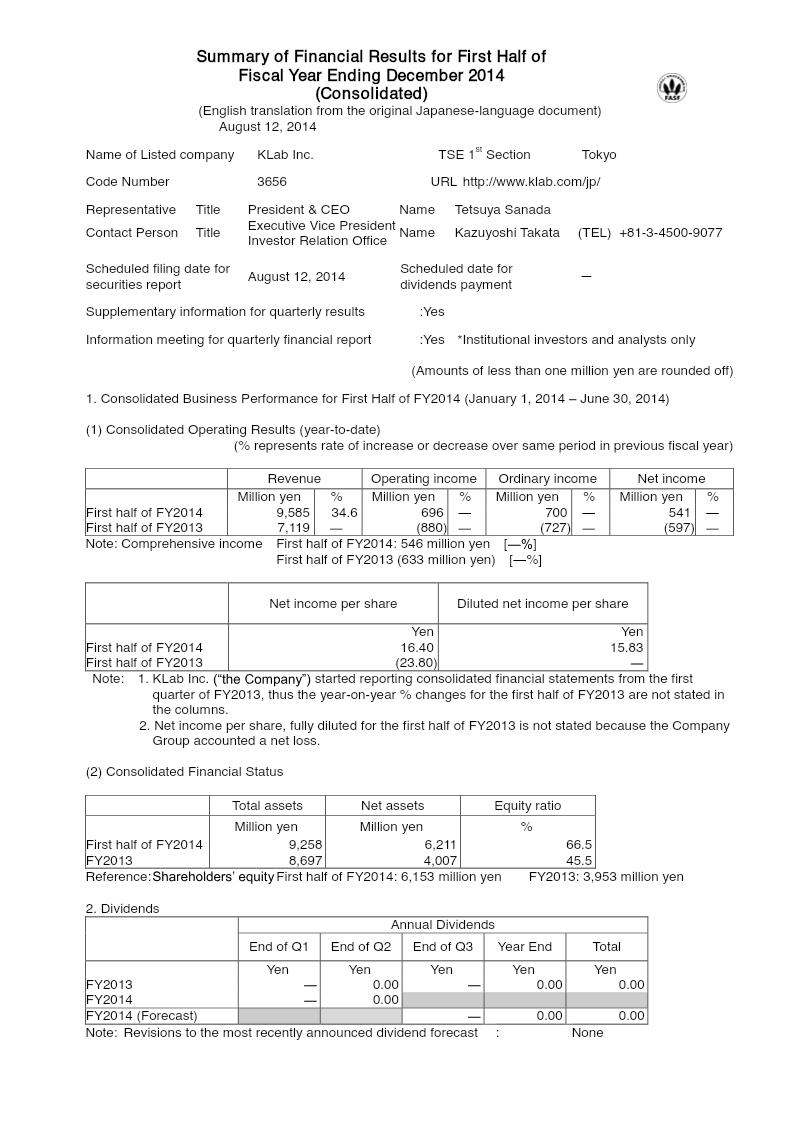

Summary of Financial Results for First Half of Fiscal Year Ending December 2014

11 pages~14 min full read

Key insights

7 takeaways · ~3 min read- 01

KLab Inc. achieved a significant financial turnaround in the first half of FY2014, reporting ¥696 million in operating income and ¥542 million in net income, compared to losses of ¥881 million and ¥598 million respectively in the same period of FY2013.

See it on page 1 - 02

Consolidated revenue grew 34.6% year-over-year to ¥9.59 billion, primarily driven by the performance of the 'Love Live! School Idol Festival' franchise and the launch of 'Celestial Craft Fleet.'

See it on page 4 - 03

Profitability was bolstered by a strategic focus on cost control, specifically the reduction of personnel and office expenses.

See it on page 4 - 04

The company’s financial position strengthened with net assets rising to ¥6.21 billion and an equity ratio of 66.5%, supported by a capital stock increase via a new subscription by Deutsche Bank London.

See it on page 10 - 05

Total liabilities decreased as the company reduced short-term loans, while total assets grew to ¥9.26 billion, largely due to an increase in accounts receivable.

See it on page 4 - 06

Management projects continued growth for the first three quarters of FY2014, forecasting revenue of ¥15.59 billion and net income of ¥1.03 billion.

See it on page 5 - 07

The company changed its fiscal year-end from August 31 to December 31 and removed the subsidiary Mediaincruise Co., Ltd. from its consolidated financial statements.

See it on page 6