FinancialKLab

Notice Concerning the Revision of Earnings Forecasts

1 Aug 20141 pages~2 min full read

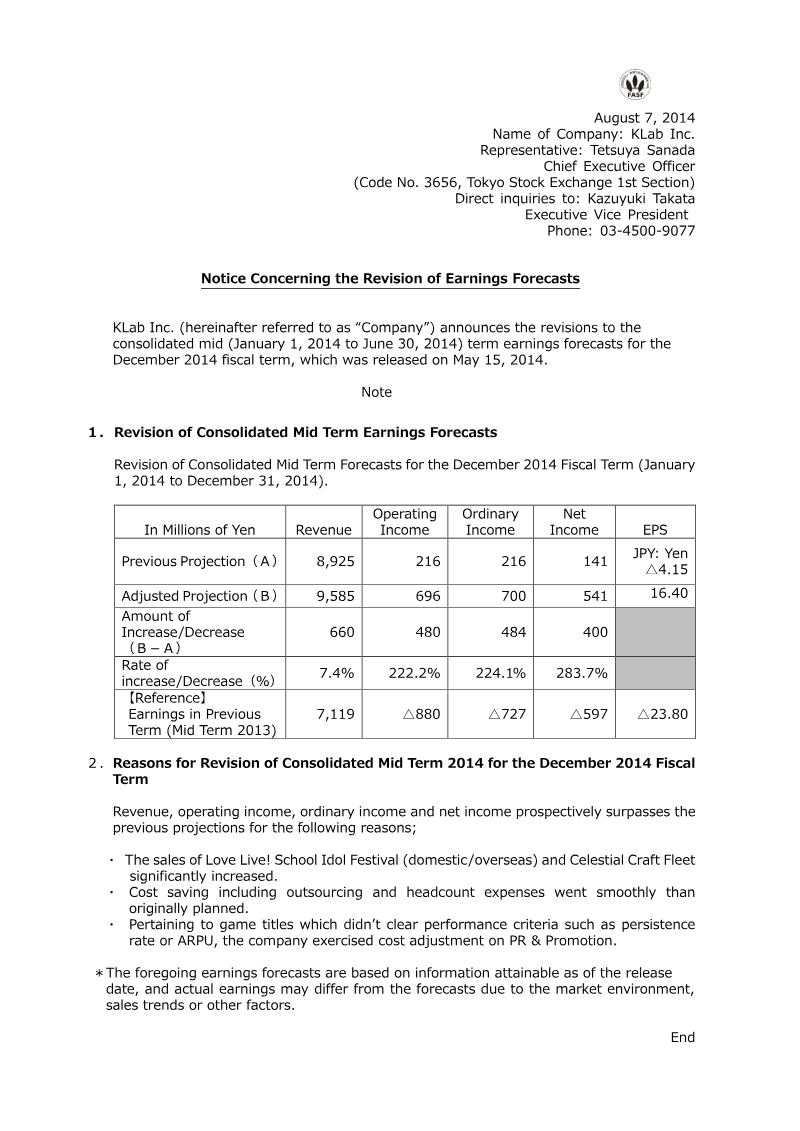

KLab Inc. revised its mid-term earnings forecast for the first half of 2014, shifting from a 597 million yen net loss in 2013 to a projected net profit of 541 million yen.

Operating income projections were increased by 222.2% and net income projections by 283.7% compared to previous guidance for the period ending June 30, 2014.

Revenue expectations for the mid-term period were raised to 9.58 billion yen, a 7.4% increase over the company's prior forecast.

The financial turnaround was primarily driven by strong sales performance from 'Love Live! School Idol Festival' (domestic and international) and 'Celestial Craft Fleet'.

Profitability was bolstered by disciplined cost management, specifically the reduction of outsourcing and personnel expenditures beyond initial targets.

Management improved margins by reallocating marketing resources away from underperforming titles that failed to meet benchmarks for player persistence and average revenue per user.

Earnings per share forecasts improved significantly, moving from a projected loss of 4.15 yen to a profit of 16.40 yen.

KLab Inc. has significantly revised its consolidated mid-term earnings forecasts for the fiscal period ending December 31, 2014, reflecting a substantial improvement in financial performance compared to previous projections. The updated guidance covers the six-month period from January 1 to June 30, 2014, and indicates a transition from the net losses recorded during the same period in 2013 to a position of profitability. Revenue expectations have been raised to 9.58 billion yen, representing a 7.4% increase over the prior forecast. More notably, operating income and net income projections have been adjusted upward by 222.2% and 283.7% respectively, with net income now expected to reach 541 million yen.

The upward revision is primarily driven by the strong market performance of key mobile gaming titles. Both the domestic and international versions of Love Live! School Idol Festival, alongside Celestial Craft Fleet, experienced significant sales growth during the period. These revenue gains were further bolstered by disciplined internal cost management. The company successfully reduced expenditures related to outsourcing and personnel beyond its initial targets. Additionally, management implemented a strategic reallocation of marketing resources by curtailing promotional spending on titles that failed to meet specific performance benchmarks, such as player persistence rates and average revenue per user.

This financial outlook demonstrates a successful turnaround for the Tokyo-based developer following a challenging 2013 mid-term period that saw a net loss of 597 million yen. By optimizing its portfolio and focusing on high-performing assets while streamlining operational costs, the company has improved its earnings per share forecast from a loss of 4.15 yen to a profit of 16.40 yen. While these figures represent the most accurate estimates available as of August 2014, actual results remain subject to fluctuations in the competitive mobile gaming market and shifting consumer trends.