FinancialTowa

Consolidated Financial Results: Nine Months Ended December 31, 2025

1 Feb 202611 pages~19 min full read

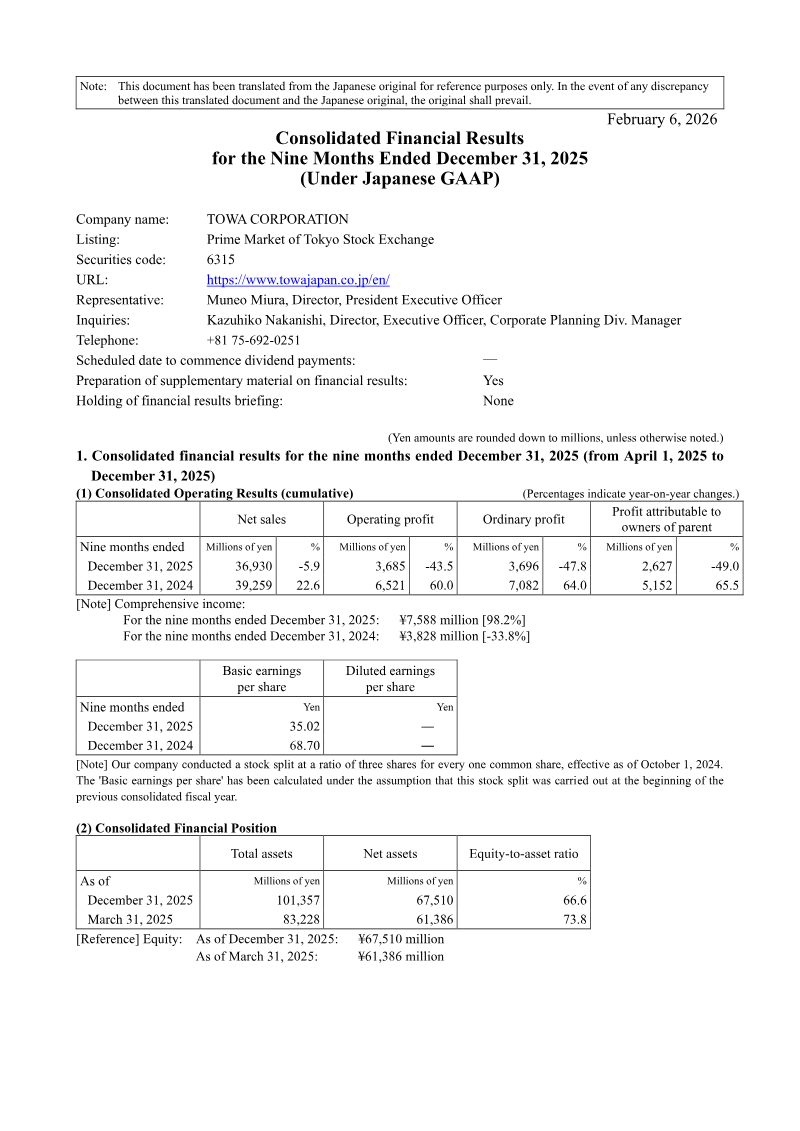

TOWA Corporation reported a significant decline in profitability for the nine months ended December 31, 2025, with operating profit falling 43.5% to 3,685 million yen and net profit dropping 49.0% to 2,627 million yen.

See it on page 1Consolidated net sales decreased by 5.9% year-on-year to 36,930 million yen, driven by a shift in product mix, increased development costs, U.S. tariff policies, and weak demand in the automotive semiconductor sector.

See it on page 5The Semiconductor Manufacturing Equipment segment, the company's primary revenue driver, saw a 6.0% decline in sales to 33,940 million yen.

See it on page 5The Laser Processing Machine business recorded a 20.0% revenue decline and an operating loss of 86 million yen, while the Medical Device segment grew by 7.8%.

See it on page 5Despite current financial headwinds, the company achieved its second-highest level of quarterly orders on record in Q3, fueled by strong demand for AI and data center-related memory applications.

See it on page 4Management has revised full-year forecasts downward due to higher initial shipment costs and delays in revenue recognition from mass production investments, though they anticipate a recovery supported by a robust order backlog.

See it on page 5TOWA Corporation’s consolidated financial results for the nine months ended December 31, 2025, reflect a challenging period characterized by a year-on-year decline in both revenue and profitability. Net sales reached 36,930 million yen, representing a 5.9% decrease compared to the same period in the previous year. Operating profit fell significantly by 43.5% to 3,685 million yen, while profit attributable to owners of the parent declined by 49.0% to 2,627 million yen. These results were primarily driven by a shift in product mix, increased development costs, and the adverse impacts of U.S. tariff policies and sluggish demand within the automotive semiconductor sector.

The company operates across three primary segments: Semiconductor Manufacturing Equipment, Medical Device, and Laser Processing Machine. The Semiconductor Manufacturing Equipment business, which constitutes the majority of total sales, saw a 6.0% decline in revenue to 33,940 million yen. While the Medical Device segment experienced a modest revenue increase of 7.8%, the Laser Processing Machine business faced a 20.0% decline in sales and an operating loss of 86 million yen. Despite these headwinds, the company reported a strong order environment, particularly for AI and data center-related memory applications, with third-quarter orders reaching their second-highest level on record.

As of December 31, 2025, the company’s financial position remains stable with total assets of 101,357 million yen and an equity-to-asset ratio of 66.6%. Looking ahead, the company has revised its full-year forecasts downward due to delayed revenue recognition from mass production investments and higher costs associated with initial shipments. However, management anticipates a recovery trend, supported by a robust order backlog and expected improvements in product mix as demand for compression equipment grows.