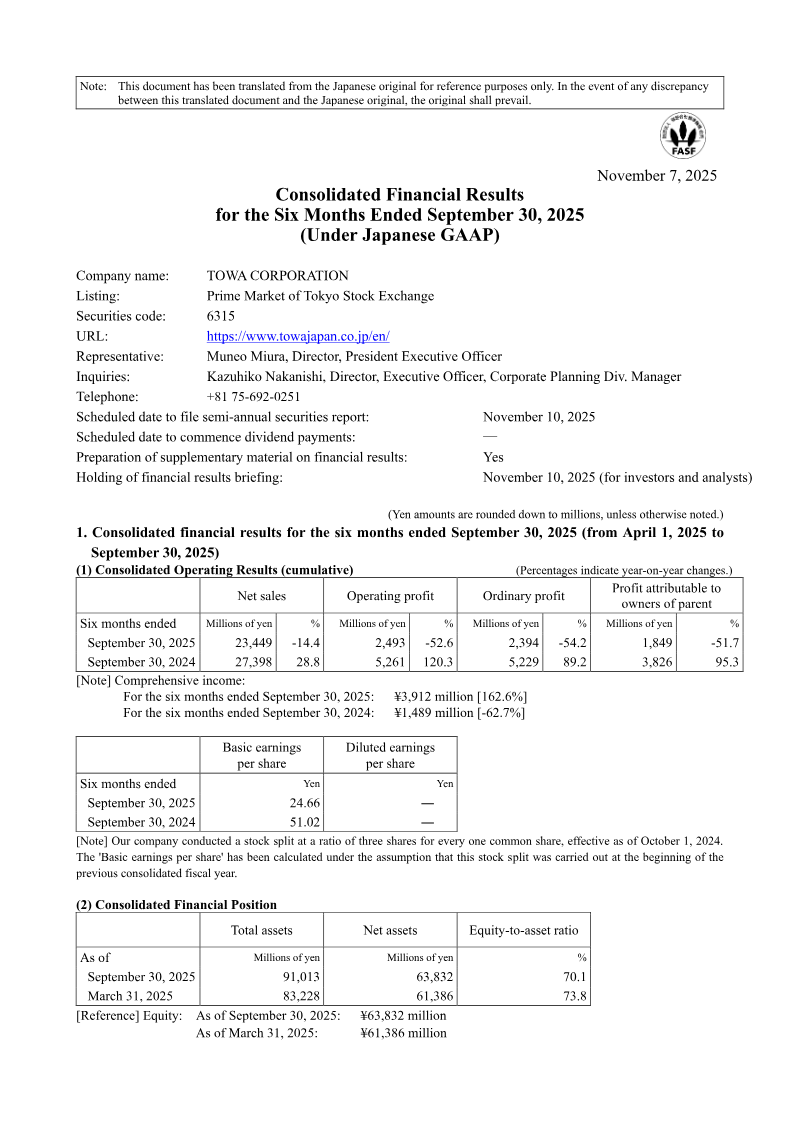

FinancialTowa

Consolidated Financial Results: Three Months Ended June 30, 2025

1 Aug 202513 pages~17 min full read

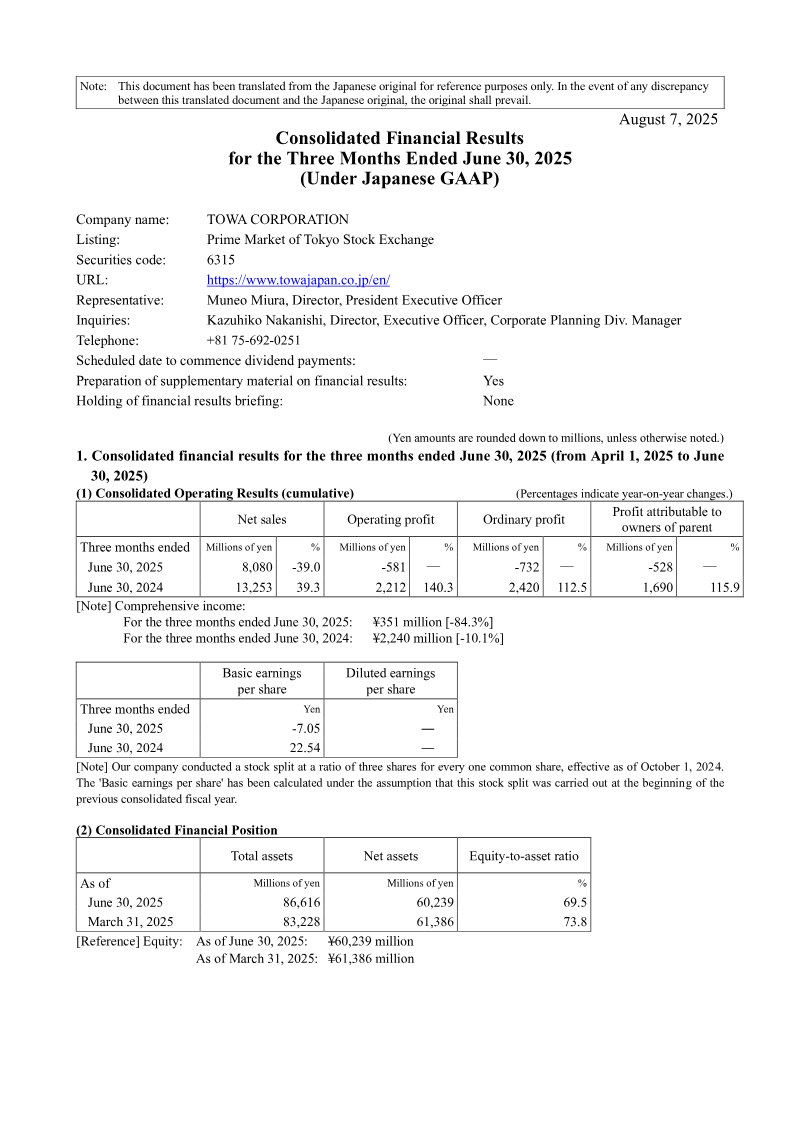

TOWA Corporation reported a 39.0% year-on-year decline in net sales to 8,080 million yen for the first quarter ended June 30, 2025.

See it on page 1The company shifted from an operating profit of 2,212 million yen in Q1 2024 to an operating loss of 581 million yen in Q1 2025.

See it on page 6The semiconductor manufacturing equipment business, the company's primary segment, saw sales drop 41.2% and incurred an operating loss of 607 million yen due to customer caution regarding U.S. tariff policies.

See it on page 6Net sales in the laser processing machine business fell by 33.2% year-on-year, while the medical device business remained stable with a 4.3% increase.

See it on page 7Management has maintained its full-year earnings forecasts, citing a recovering order environment in China and expanding demand for generative AI-related molding equipment.

See it on page 5The net loss attributable to owners of the parent company for the quarter was 528 million yen, compared to a profitable position in the same period last year.

See it on page 10TOWA CORPORATION’s consolidated financial results for the first quarter ended June 30, 2025, reflect a period of significant contraction compared to the same period in the previous fiscal year. The company reported net sales of 8,080 million yen, representing a 39.0% year-on-year decline. Profitability metrics also shifted into negative territory, with an operating loss of 581 million yen, an ordinary loss of 732 million yen, and a loss attributable to owners of the parent of 528 million yen. This performance stands in stark contrast to the first quarter of 2024, which saw an operating profit of 2,212 million yen.

The primary driver of this downturn was the semiconductor manufacturing equipment business, which experienced a 41.2% decrease in net sales, resulting in an operating loss of 607 million yen. Management attributes this decline to heightened uncertainty regarding U.S. tariff policies, which prompted customers to adopt a cautious approach to capital investment and led to the rescheduling of equipment deliveries. While the medical device business maintained steady performance with a 4.3% increase in net sales, the laser processing machine business also saw a decline, with net sales falling 33.2% year-on-year.

Despite these results, the company maintains a neutral outlook for the remainder of the fiscal year. Management reports that the order environment is showing signs of recovery, particularly in China, and notes that the customer base for its generative AI-related molding equipment is expanding. Consequently, the company has not revised its previously announced consolidated earnings forecasts for the second quarter or the full fiscal year, anticipating a return to profitability as capital investment and demand recover across key Asian markets.