FinancialKaga Electronics Co.

Summary of Consolidated Financial Results: First Half Ended September 30, 2015 (Japan)

12 pages~20 min full read

Key insights

6 takeaways · ~2 min read- 01

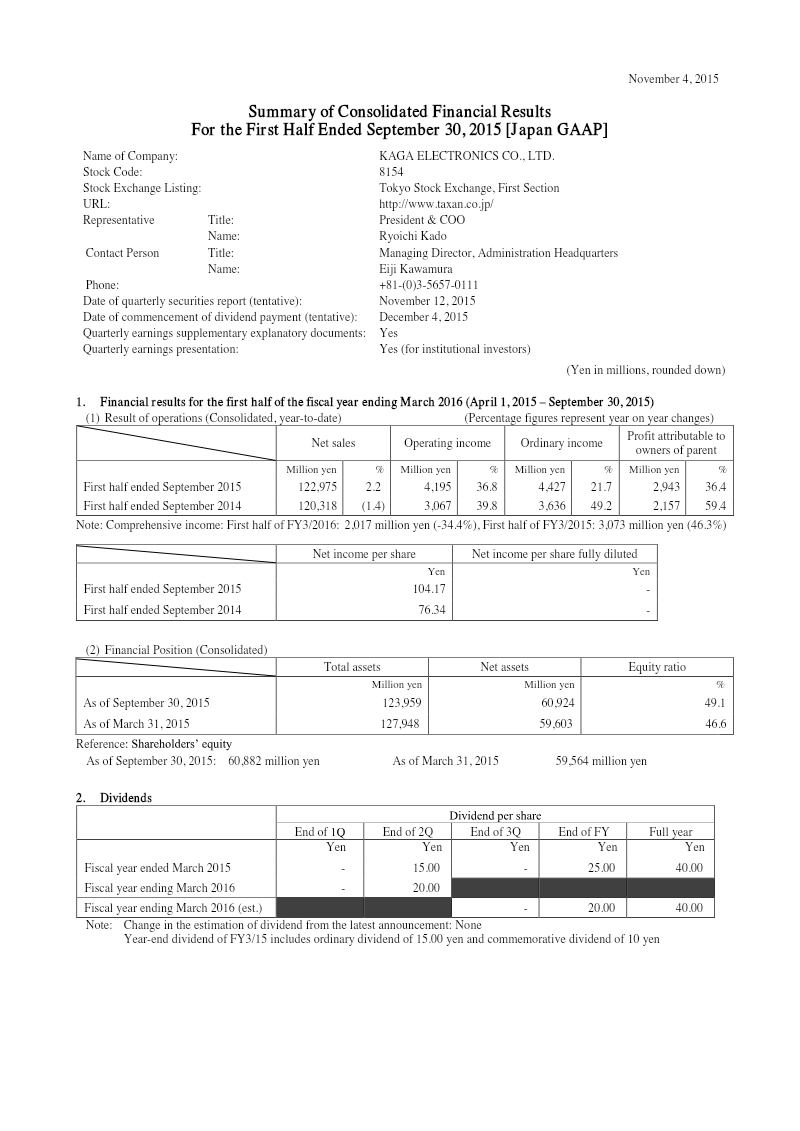

Kaga Electronics achieved a 36.8% increase in operating income to 4,195 million yen and a 36.4% rise in net profit to 2,943 million yen for the first half of the fiscal year ending September 30, 2015.

See it on page 1 - 02

Consolidated net sales grew by 2.2% year-over-year to 122,975 million yen, supported by strong performance in the electronic components segment.

See it on page 4 - 03

Growth was primarily driven by increased demand in the mobile, automotive, and healthcare sectors, alongside a strategic focus on Electronics Manufacturing Services (EMS).

See it on page 4 - 04

The information equipment segment underperformed due to weak demand for PCs and digital cameras, while the 'others' segment recorded an operating loss of 102 million yen.

See it on page 4 - 05

Management revised the full-year forecast for the fiscal year ending March 2016, lowering the net sales projection to 252,000 million yen while raising the operating income forecast to 7,200 million yen.

See it on page 2 - 06

The company maintains a stable financial position with total assets of 123,959 million yen and an equity ratio of 49.1%.

See it on page 1