Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

GameVault System | Game Industry Library

Writers

GameVault System

Back to Writers

GameVault System

Research

1 document

Internal system writer for automated discovery sources.

Documents

Reports

Presentations

Whitepapers

Articles

Financial

Legal

Other

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

2 pages

Q1 2026 Market Themes to Watch

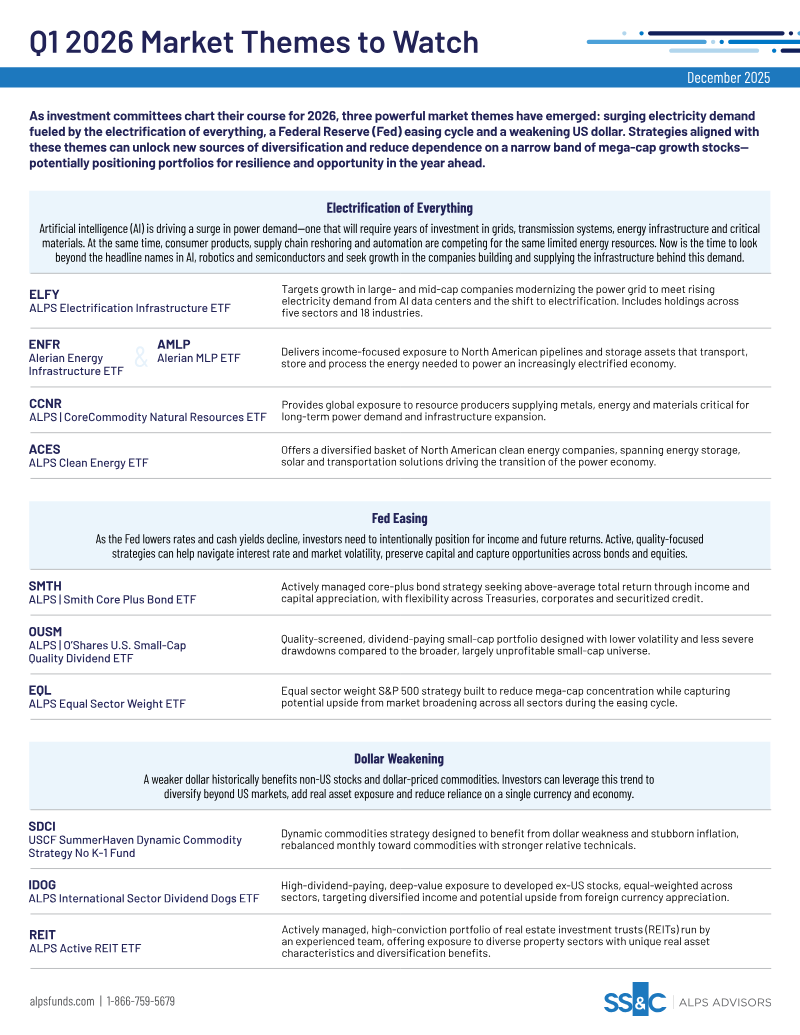

Investors should pivot from mega-cap growth stocks toward infrastructure assets that support the electrification of the economy, including grid modernization, energy transmission, and critical material supply chains.

The surge in power demand driven by AI, data centers, and industrial automation necessitates capital allocation into North American energy pipelines, clean energy solutions, and global natural resource producers.

The Federal Reserve’s interest rate easing cycle requires a shift toward quality-oriented income strategies, such as active fixed-income management and dividend-paying small-cap equities, to replace declining cash yields.

Market Analysis

Market Forecast

Investment

+2

GameVault System