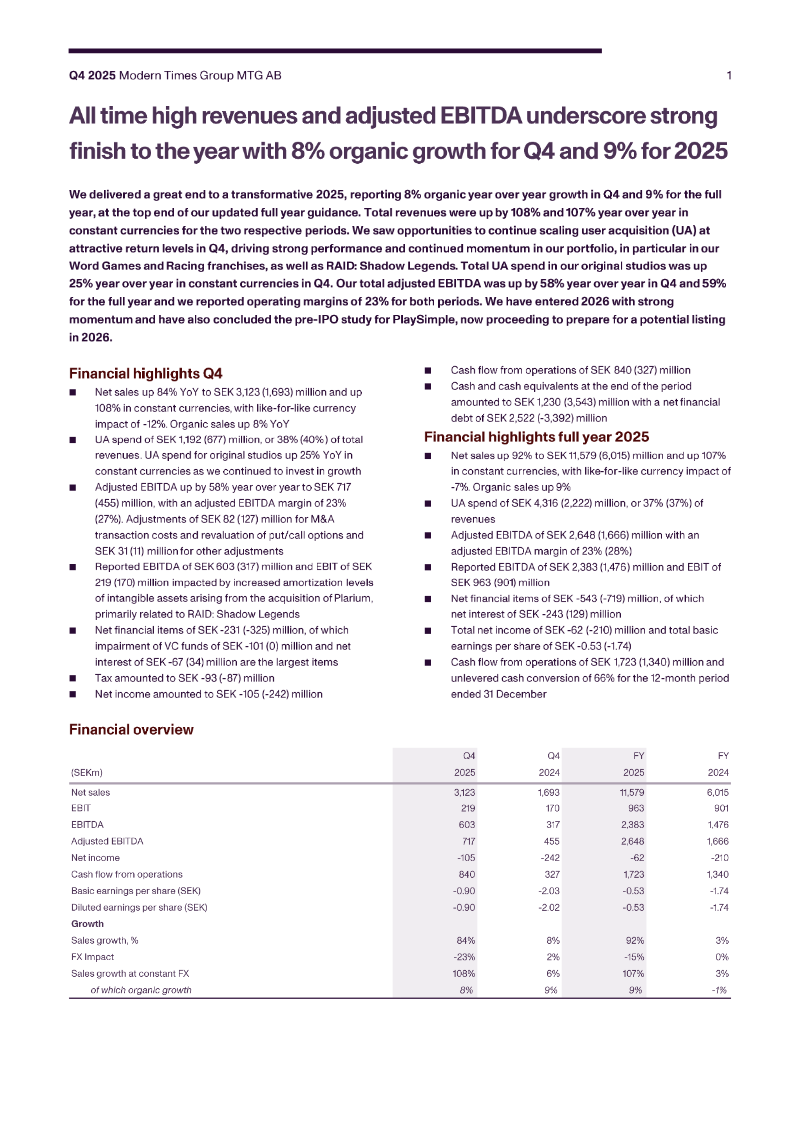

Thunderful Group reported a pronounced contraction in Q4 2024, with net revenue falling 27.6 % to 77.4 MSEK and operating loss widening to –631.5 MSEK, a 13.7 % increase in loss versus the same quarter last year. Adjusted EBITDA slipped to –10.8 MSEK, and a 560.2 MSEK write‑down of capitalised development costs—primarily acquisition‑related—further eroded profitability. The publishing division suffered the most, recording an operating loss of –865.2 MSEK and a negative EBITDA margin of 34.8 %, while the co‑development & services arm posted a modest –14.1 % margin.

Total assets collapsed from 3,151.0 MSEK to 772.9 MSEK, and cash & equivalents fell from 209.1 MSEK to 150.2 MSEK, reflecting heavy restructuring costs and the divestment of distribution operations. The group has withdrawn its previously set financial targets following the sale of its distribution arm and will announce new long‑term goals later. Share transfers, including the return of Jumpship Limited to Dino Patti and settlement of earn‑out claims, were completed with shareholder approval on 10 Feb 2025.

Gross profit declined to 53.4 MSEK, with a gross margin of 69.0 %. While the trailing‑12‑month adjusted EBITDA turned positive at 109.2 MSEK, core working capital remains high at 526.3 MSEK and interest‑bearing net debt stands at 402.1 MSEK, yielding a debt/adjusted EBITDA ratio of 3.7. These figures underscore revenue contraction but improving operating cash flow, with liquidity and leverage metrics still presenting a concern.

Modern Times Group · 2026

Modern Times Group · 2026

Stillfront · 2025

Modern Times Group · 2025

Modern Times Group · 2025

Modern Times Group · 2025

Thunderful · 2025

Starbreeze · 2025

Paradox Interactive · 2024

Modern Times Group · 2023

Stillfront · 2022

Paradox Interactive · 2022