Related Documents

Financial

Q4 2025 Interim Report

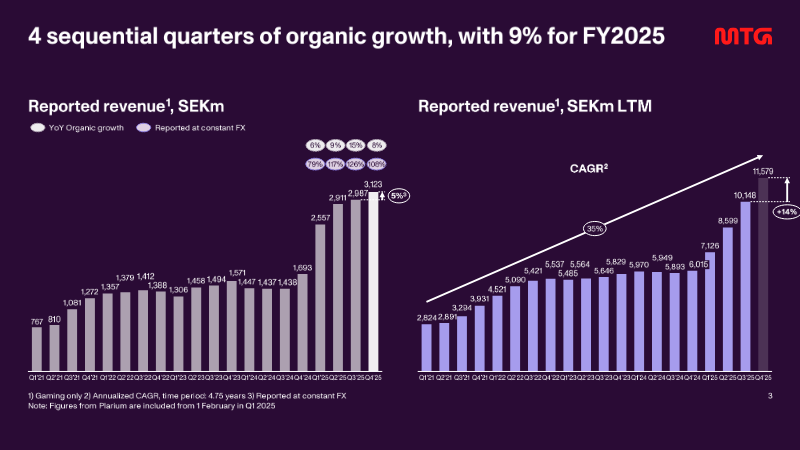

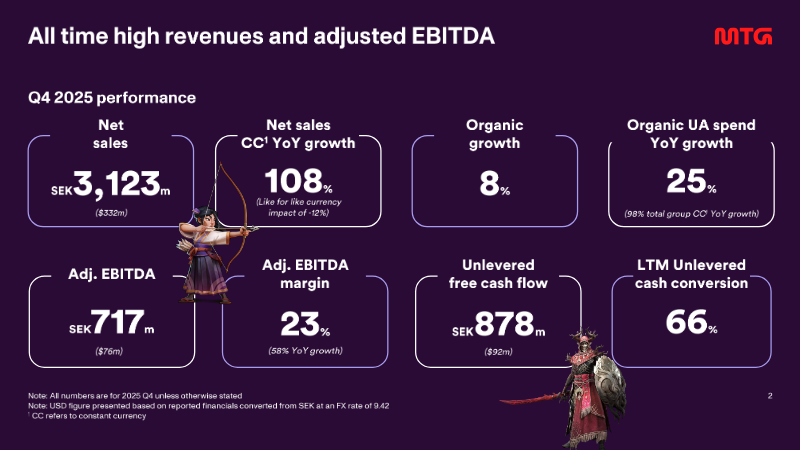

The interim filing presents the fourth‑quarter 2025 financial results for a midcore‑casual gaming group, emphasizing a record‑setting revenue run and the successful execution of a transformation agenda that includes the integration of the Plarium acquisition and the rollout of a new district structure in early 2026. Revenue reached SEK 3,123 million, reflecting 108 % organic growth year‑on‑year and a 25 % increase on a constant‑currency basis, while adjusted EBITDA rose to SEK 717 million, delivering a 23 % margin that matches the full‑year figure. Unlevered free cash flow amounted to SEK 878 million, with a cash‑conversion rate of 66 % and a leverage ratio of five times EBITDA, underscoring robust liquidity and disciplined capital management. User‑acquisition spending accelerated, representing 38 % of quarterly revenue—up from 37 % in the prior quarter—and grew 76 % on a reported basis, driven by heightened investment in original studios, new casual titles, and the racing franchise. The direct‑to‑consumer channel expanded by 600 basis points to 32 % of total revenue, reflecting a strategic shift toward higher‑margin in‑app purchases. Across the fiscal year, the company posted a 9 % organic revenue increase, with word‑games, racing, and RAID franchises delivering the strongest quarter‑end performance. Operating cash flow for the quarter stood at SEK 840 million, while adjusted net income was SEK 1,390 million, translating to an adjusted EPS of SEK 11.33. The financial outcomes exceed guidance and position the firm to meet its medium‑term outlook, with a pre‑IPO study for PlaySimple concluded and the midcore transformation progressing as planned.

Modern Times GroupFeb 2026

Report

Key Insights and Data: 2023–2025

Mobile gaming drives the global industry’s growth through 2025, accounting for more than half of worldwide revenue and over eighty percent of players. Global gaming income is projected to reach $197 billion in 2025, a 7.5 % year‑over‑year rise largely powered by mobile and PC segments, while console expansion remains modest. The sector’s resilience is most pronounced in emerging markets where Android and iOS user volumes surge, yet revenue concentration persists in Western regions—particularly the United States and the United Kingdom—where iOS dominates acquisition spend. Competitive dynamics sharpen as the top ten to fifty titles on Google Play and Apple’s App Store capture an increasing share of revenue, creating a winner‑take‑all environment. Hyper‑casual and match‑3 games concentrate U.S. spend, whereas Android strategy titles spread more evenly across Japan, Korea, and Taiwan. Sub‑genres such as chess, ludo, hidden object RPGs, and slots thrive in China, India, Brazil, and Southeast Asia, collectively commanding 15–20 % of global spend. Across most categories, day‑one retention has slipped from roughly 80 % to about 60 %, underscoring a broader challenge of sustaining early engagement. Download patterns reveal Android’s volume advantage—about 70 % of global downloads—with the United States, India, Brazil, and Indonesia leading. iOS, though smaller in volume (30 %), delivers higher per‑download revenue, especially in China and the U.S. iOS penetration is rising in emerging markets such as Brazil and Vietnam, while Android’s share in India climbs from 18.8 % to 21.3 %. Genre‑level analysis shows modest growth (10–30 %) across most mobile categories, with occasional outliers and declines in specific niches. Overall, the landscape is characterized by rapid mobile expansion, concentrated monetization power, and shifting geographic priorities that shape strategic opportunities for developers and marketers.

InvestGameJan 2026

Report

Gaming App Insights Report: 2025 Edition

The analysis tracks the state of the global mobile‑gaming market through 2024 and projects its trajectory toward 2025, emphasizing how emerging AI‑driven personalization will shape growth. It establishes that the sector is recovering from the volatility of 2023, with worldwide app installs climbing 4 % year‑over‑year in 2024, even as average session length contracted. Core user engagement metrics, however, show modest decline: day‑1 retention fell from 28 % to 27 % and median revenue per active user dropped from $0.31 to $0.28, indicating pressure on traditional monetization models. In contrast, advertising efficiency improved, reflected in higher installs per mille (IPM) and stronger ad‑performance indicators across major markets. The report’s geographic scope is global, encompassing all major mobile‑gaming regions, and its temporal frame spans the 2023‑2025 period. It integrates data from app stores, ad networks, and cross‑platform measurement tools to deliver a comprehensive view of user acquisition, retention, and revenue trends. The central thesis posits that the next wave of growth will be powered by AI‑enabled, culturally tailored experiences that adapt difficulty, blend monetization formats, and deploy live events to boost lifetime value. Developers and marketers who adopt a metrics‑focused, AI‑augmented approach—identifying pivotal in‑game moments and steering users toward optimal pathways—are projected to achieve the most scalable expansion. Cross‑platform analytics suites are highlighted as essential for delivering the visibility required to implement these strategies effectively.

AdjustJan 2025

Report

The State of Puzzle Games: An Analysis of the Puzzle Category in Mobile Gaming

The mobile puzzle game market is undergoing a significant structural evolution, characterized by a shift in product models and a notable rise in hybridcasual gaming. This analysis, covering global data from January 2018 through June 2023, examines the performance of various puzzle sub-genres, including swap, blast, chain, and pair mechanics. By leveraging store intelligence and download estimates from the Apple App Store and Google Play, the findings highlight how developers are increasingly integrating meta-features and diversified monetization strategies to sustain revenue in a maturing landscape. A central finding is the remarkable growth of the hybridcasual product model, which saw a 430% increase in revenue between early 2022 and early 2023. While traditional casual games continue to dominate overall market share through consistent operations and robust meta-features, they have experienced modest declines in both downloads and revenue. Conversely, hybridcasual titles—particularly within the pair sub-genre—have successfully captured user interest by blending accessible gameplay with more sophisticated monetization tactics, such as in-app purchases, which were previously less common in hypercasual-leaning segments. The data indicates that sub-genres like pair have emerged as high-growth areas, with hybridcasual revenue in this category rising from $7 million in the first quarter of 2022 to $40 million by the first quarter of 2023. Meanwhile, other established sub-genres, such as merge and physics, have seen download declines as their reliance on hypercasual models wanes. Successful top-tier games across all categories now frequently employ a combination of live operations, season passes, and social clans to drive engagement. Ultimately, the puzzle market is moving toward a hybrid approach, where the simplicity of casual mechanics is increasingly supported by the deeper monetization and retention frameworks typically associated with mid-core titles.

Sensor TowerJan 2025