ReportPCF Group

Current Report No. 20/2021: Conclusion of Series B Share Subscription and Partial Series A Sale

2 pages~2 min full read

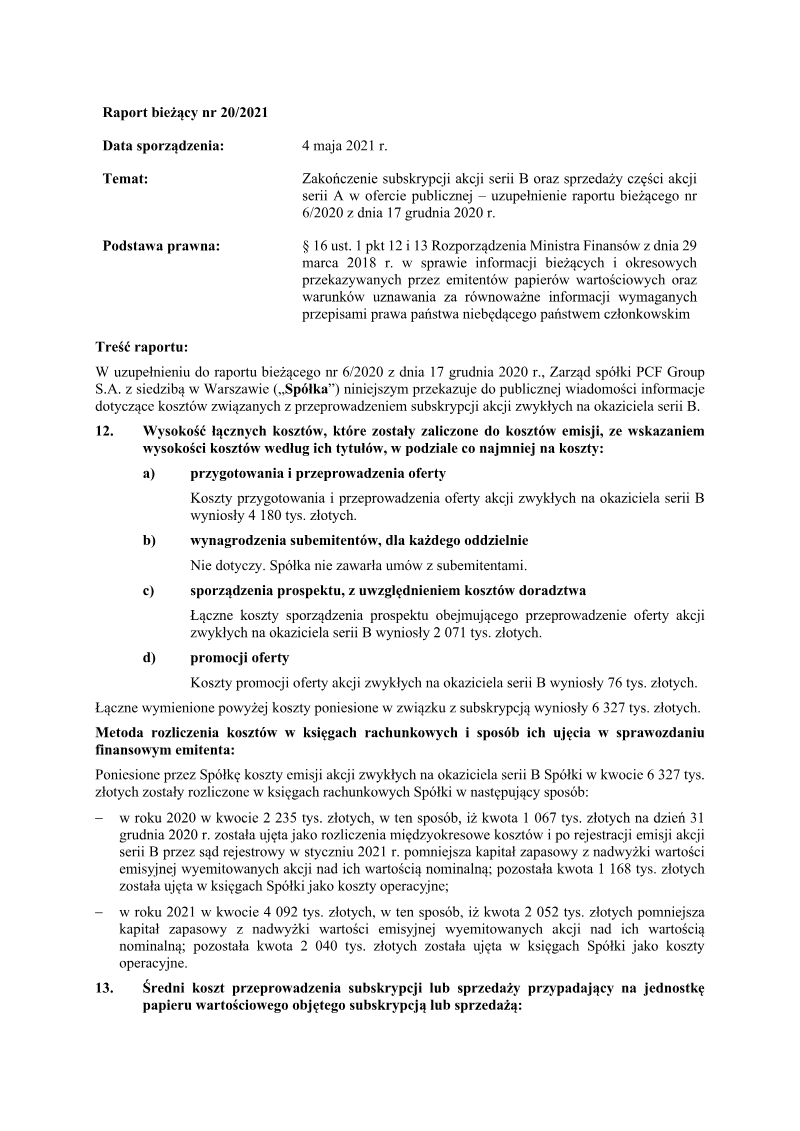

PCF Group S.A. incurred total costs of 6,327 thousand PLN for the Series B share subscription and partial Series A share sale conducted between 2020 and 2021.

See it on page 1The total issuance costs comprised 4,180 thousand PLN for offer preparation and execution, 2,071 thousand PLN for prospectus and advisory services, and 76 thousand PLN for promotional expenses.

See it on page 1The average cost per security issued or sold during the offering process was 1.53 PLN.

See it on page 2In 2020, PCF Group recorded 2,235 thousand PLN in costs, split between 1,067 thousand PLN charged to capital reserves and 1,168 thousand PLN expensed operationally.

See it on page 1In 2021, the company recorded 4,092 thousand PLN in costs, with 2,052 thousand PLN reducing the capital reserve and 2,040 thousand PLN expensed operationally.

See it on page 1The share issuance process involved no sub-emitter fees, and the financial reporting was prepared in accordance with Polish regulatory requirements.

See it on page 1The report details the completion of a Series B share subscription and partial sale of Series A shares by PCF Group S.A. The primary objective is to disclose the costs incurred during the Series B subscription, supplementing earlier information released in report No. 6/2020. Total emission costs amounted to 6,327 thousand PLN, broken down into preparation and execution of the offer (4,180 k), prospectus drafting and advisory services (2,071 k), and promotional expenses (76 k). No sub‑emitter fees applied.

Accounting treatment of these costs is outlined: in 2020, 2,235 k PLN were recorded, with 1,067 k PLN treated as inter‑period cost adjustments reducing the capital reserve from excess issue value over par, and 1,168 k PLN expensed operationally. In 2021, 4,092 k PLN were recorded similarly, with 2,052 k PLN reducing the capital reserve and 2,040 k PLN expensed.

The average cost per security issued or sold was calculated at 1.53 PLN. The report covers the Polish market, focusing on PCF Group’s public offerings during 2020–2021. No survey or external data sources are cited; the methodology relies on internal financial records and regulatory reporting requirements under Polish finance ministry regulations. The concise disclosure fulfills legal obligations for ongoing information to investors and regulators, providing transparency on the financial impact of the share issuance activities.