Related Documents

Financial

3rd Quarter Report: Fiscal Year Ending March 31, 2026

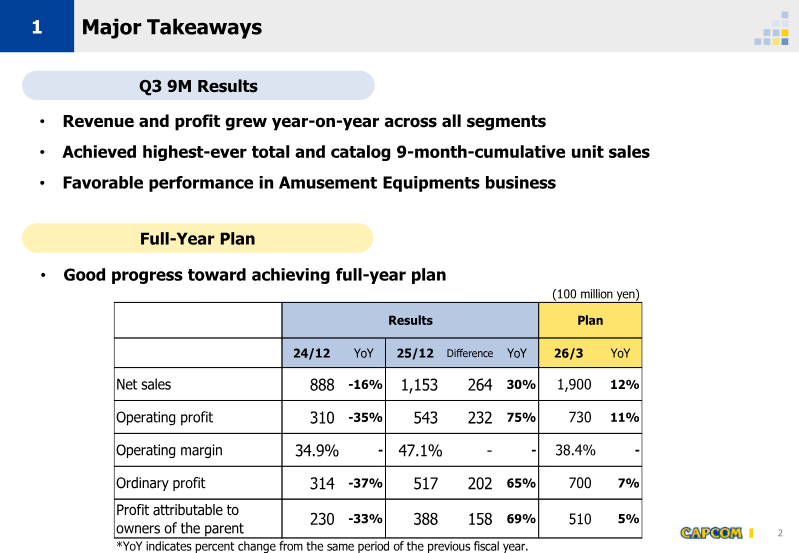

This financial report details Capcom’s consolidated performance for the third quarter of the fiscal year ending March 31, 2026. The findings indicate significant year-on-year growth in both revenue and profit across all business segments, driven primarily by the sustained performance of catalog titles and strong results in the amusement equipment division. Net sales reached 115.3 billion yen, a 30% increase over the previous year, while operating profit rose 75% to 54.3 billion yen. These results place the company on a favorable trajectory to meet its full-year targets of 190 billion yen in net sales and 730 billion yen in operating profit. The Digital Contents segment remains the primary driver of growth, with unit sales reaching a record 9-month high of 34.6 million units. Catalog titles accounted for 96.4% of these sales, underscoring the long-term value of core franchises such as Resident Evil, Monster Hunter, and Street Fighter. Notably, Monster Hunter Wilds surpassed 11 million cumulative units, while Resident Evil 4 and Street Fighter 6 continued to show steady growth. Digital sales now represent 94.1% of total units, with PC platforms alone accounting for over 55% of the volume. Geographically, overseas markets dominate the business, representing nearly 90% of total unit sales. Beyond software, the Arcade Operations and Amusement Equipments segments reported double-digit growth. Arcade sales rose 12% following the opening of new stores and the expansion of specialty formats, while Amusement Equipments saw a 74% surge in net sales due to the strong performance of smart slot titles like Shin Onimusha 3. The company’s strategic outlook remains focused on leveraging its leading brands through upcoming releases such as Resident Evil Requiem and Monster Hunter Stories 3, alongside cross-media expansions including a new Devil May Cry anime and a live-action Street Fighter film.

CapcomFeb 2026

Financial

CD Projekt Group FY 2024 Earnings

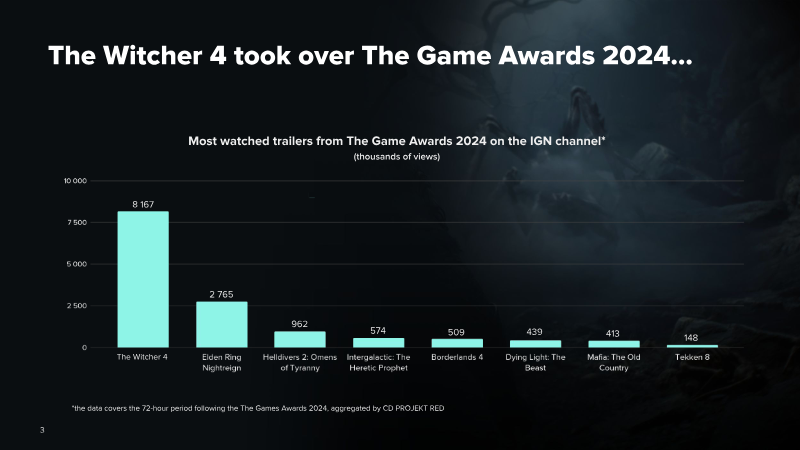

CD Projekt Group presents its FY 2024 earnings, outlining financial performance, operational milestones and a long‑term growth outlook for the studio and its portfolio. The report emphasizes the commercial impact of The Witcher 4, which captured 53 % of press coverage in the 72 hours after The Game Awards 2024, generating 2 150 articles and becoming the most discussed title among peers such as Elden Ring and Final Fantasy. Development capacity expanded to 411 staff, with 650 developers allocated across The Witcher 4, Orion, Sirius, Hadar, the Witcher Remake and several unannounced projects. Revenue for the year fell 20 % year‑on‑year to PLN 1.23 billion, while cost of sales decreased to PLN 377.9 million, delivering a gross profit of PLN 852.2 million and EBIT of PLN 469.0 million. Net profit reached PLN 481.1 million, reflecting a net‑profit margin of roughly 39 % in 2023 and an expected rise to 47.7 % in 2024, with a target of 58.5 % by

CD ProjektMar 2025

Legal

Third-Quarter 2025-26 Sales

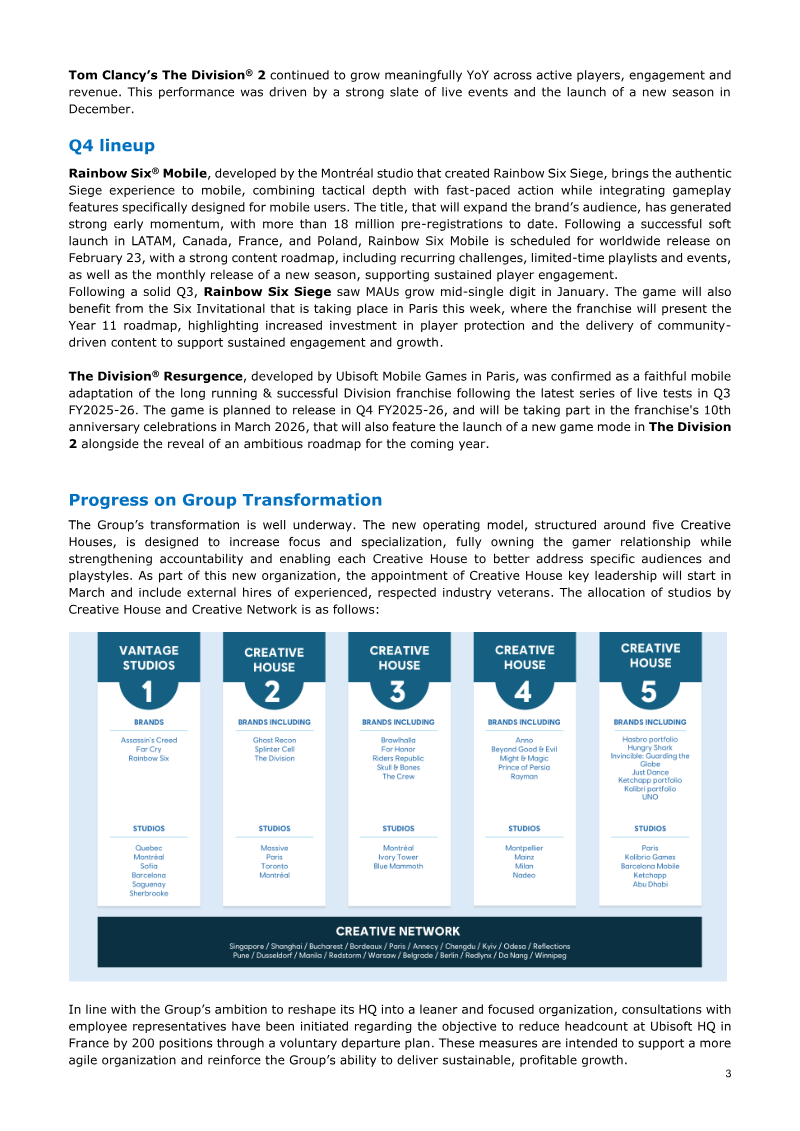

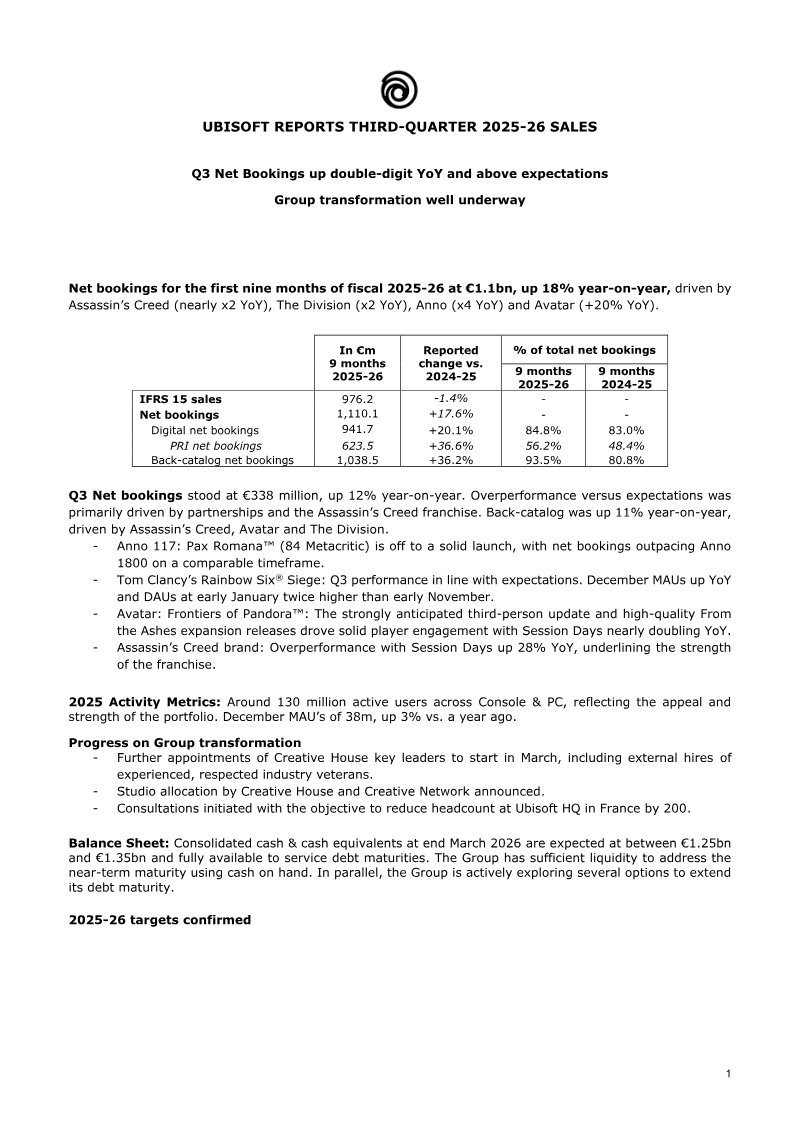

Ubisoft reported a double-digit increase in net bookings for the third quarter of fiscal year 2025-26, reaching €338 million. This 12% year-on-year growth exceeded internal expectations, primarily driven by strong performance in partnerships and the Assassin’s Creed franchise. For the first nine months of the fiscal year, net bookings totaled €1.11 billion, an 18% increase compared to the previous year. This growth was largely supported by back-catalog sales, which rose 36.2% and accounted for over 93% of total net bookings during the nine-month period. Key performance drivers included the successful launch of Anno 117: Pax Romana, which outpaced its predecessor, and significant engagement growth for Avatar: Frontiers of Pandora following a major third-person perspective update. While the first-person shooter market remained crowded, Tom Clancy’s Rainbow Six Siege performed in line with expectations, showing a recovery in daily active users by early January. Overall player activity remained robust, with approximately 130 million unique active users across PC and consoles during the 2025 calendar year. The company is currently undergoing a major structural transformation into five distinct "Creative Houses" to sharpen focus and accelerate decision-making. This reorganization includes the recent completion of a €1.16 billion investment from Tencent into Vantage Studios, which manages the Assassin’s Creed, Far Cry, and Rainbow Six brands. Additionally, Ubisoft is streamlining its headquarters in France, initiating consultations to reduce headcount by 200 positions. Looking ahead, Ubisoft confirmed its full-year targets, including net bookings of approximately €1.5 billion and a non-IFRS EBIT of around -€1 billion. The fourth-quarter pipeline features the global mobile launches of Rainbow Six Mobile and The Division Resurgence. The group maintains a solid liquidity position, with cash equivalents expected between €1.25 billion and €1.35 billion by March 2026, providing the flexibility to address upcoming debt maturities.

UbisoftJan 2025

Financial

Financial Results for the First Half of the Fiscal Year Ending March 2026

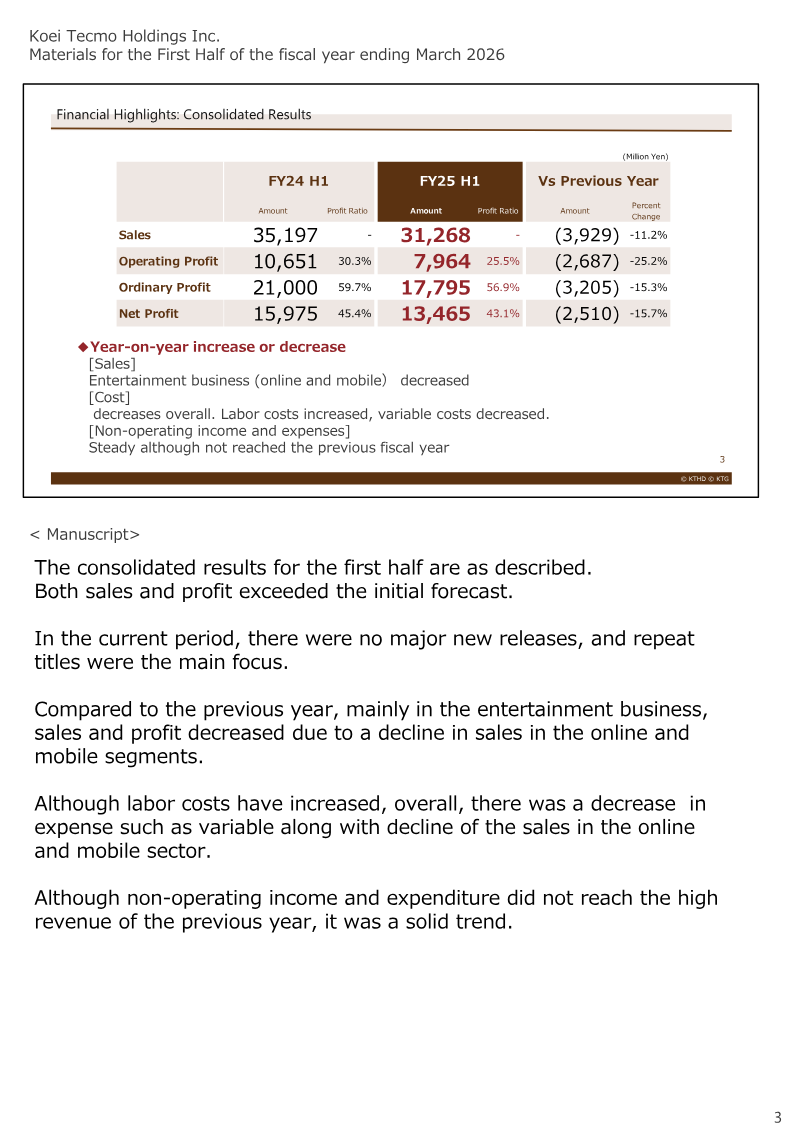

Koei Tecmo experienced a year-on-year decline in financial performance during the first half of the fiscal year ending March 2026, with sales dropping 11.2% and operating profit falling 25.2%. This downturn resulted primarily from a sparse release schedule and lower revenue within the online and mobile segments. However, the company outperformed its internal forecasts due to resilient back-catalog sales and disciplined expense management. Full-year guidance remains unchanged as management anticipates a significant recovery in the second half, driven by a concentrated launch window for major titles such as Dynasty Warriors: Origins. The strategic focus for the remainder of the fiscal year involves a robust pipeline of eleven console and PC titles alongside two mobile releases. By prioritizing high-profile remakes like Romance of the Three Kingdoms 8 and Fatal Frame II, the company seeks to secure stable profit margins while transitioning toward a global, digital-first marketing infrastructure. This shift includes a move toward in-house publishing for large-scale projects and a concerted effort to expand market share in North America, Europe, and emerging regions such as the Middle East and North Africa. Long-term objectives are anchored by the Fourth Medium-Term Management Plan, which targets a cumulative three-year operating income of 100 billion yen. To achieve this, the company is balancing the maintenance of established franchises with the development of new intellectual properties and cross-media expansions into anime and merchandise. Furthermore, corporate governance milestones were met through a treasury share offering that increased the tradable share ratio to 37.3%, ensuring continued compliance with Tokyo Stock Exchange Prime Market listing criteria.

Koei TecmoJan 2025