The quarterly report for the first quarter of 2026 demonstrates that 11 Bit Studios achieved a 13.5 % increase in revenue, reaching PLN 19.8 million (EUR 4.67 m), largely driven by the commercial success of proprietary titles such as Frostpunk 2 and The Alters, and the publishing hit Death Howl. Despite this top‑line growth, operating profit swung to a loss of PLN 5.48 m (EUR 1.29 m) from a profit in the same period last year, primarily due to a sharp rise in depreciation and amortisation expenses (PLN 11.36 m versus PLN 4.58 m). EBITDA, however, improved to PLN 5.88 m (EUR 1.39 m), supported by a significant increase in finance income, largely from exchange‑rate gains and fair‑value movements on financial instruments.

Cash generation remained robust; net cash from operating activities rose to PLN 15.43 m (EUR 3.64 m), while investing cash outflows increased to PLN 6.40 m, resulting in a net cash inflow of PLN 8.67 m (EUR 2.04 m). Liquidity, however, weakened slightly as cash and cash equivalents fell by 24 % to PLN 52.5 m, driven by higher short‑term bond holdings and lower bank balances. Trade receivables grew markedly to PLN 14.26 m, accompanied by a higher allowance for credit losses reflecting ageing receivables.

The balance sheet shows modest increases in property, plant and equipment (to PLN 21.40 m) and intangible assets (to PLN 261.56 m), driven by new machinery investments and development work in progress. Deferred tax assets rose to PLN 7.93 m, while liabilities increased marginally to PLN 0.82 m. The company’s contract liabilities declined as advances for Frostpunk 2 add‑ons were settled, indicating progress in monetising its IPs.

Geographically, the company’s revenue is heavily weighted toward the United States (≈ 77 % of total sales), exposing it to exchange‑rate risk as the Polish złoty strengthens against the U.S. dollar. Management highlighted upcoming DLC releases and continued investment in new IPs as key growth drivers, while noting the need to manage depreciation impacts on operating profitability.

11 bit studios · 2026

11 bit studios · 2025

11 bit studios · 2025

11 bit studios · 2025

11 bit studios · 2025

PCF Group · 2025

11 bit studios · 2025

11 bit studios · 2025

11 bit studios · 2025

11 bit studios · 2025

11 bit studios · 2025

11 bit studios · 2025

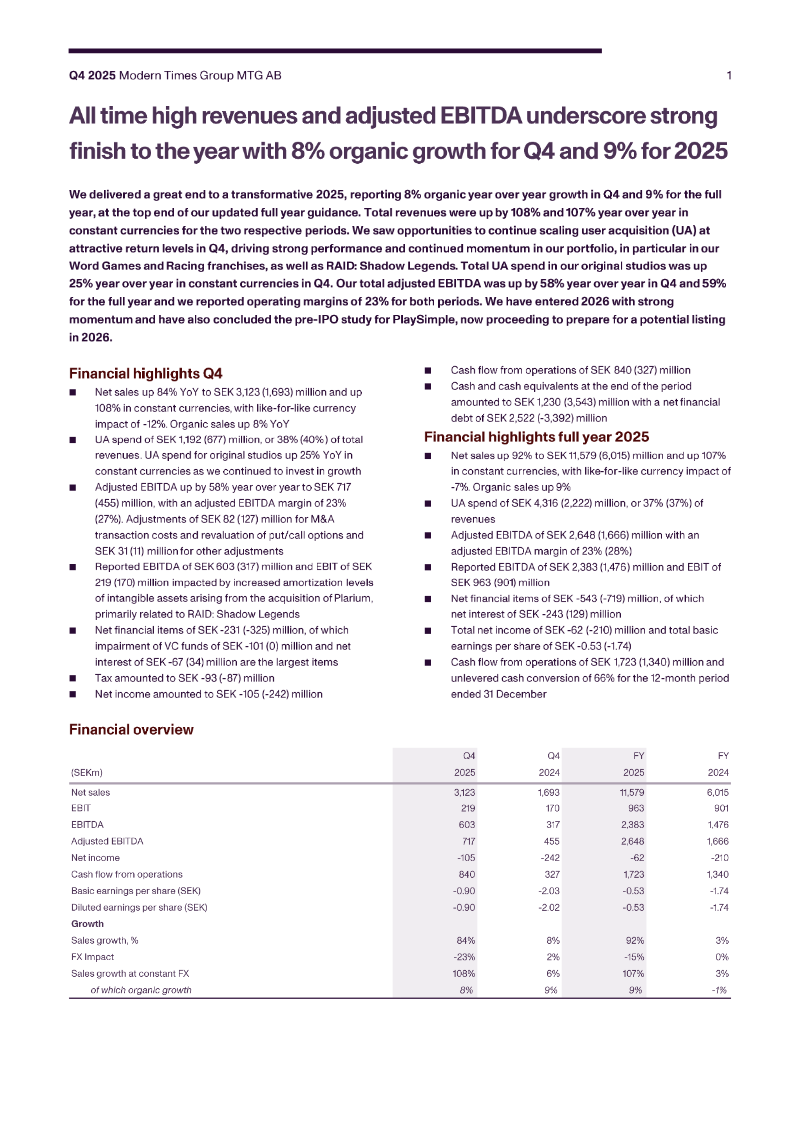

Modern Times Group · 2026

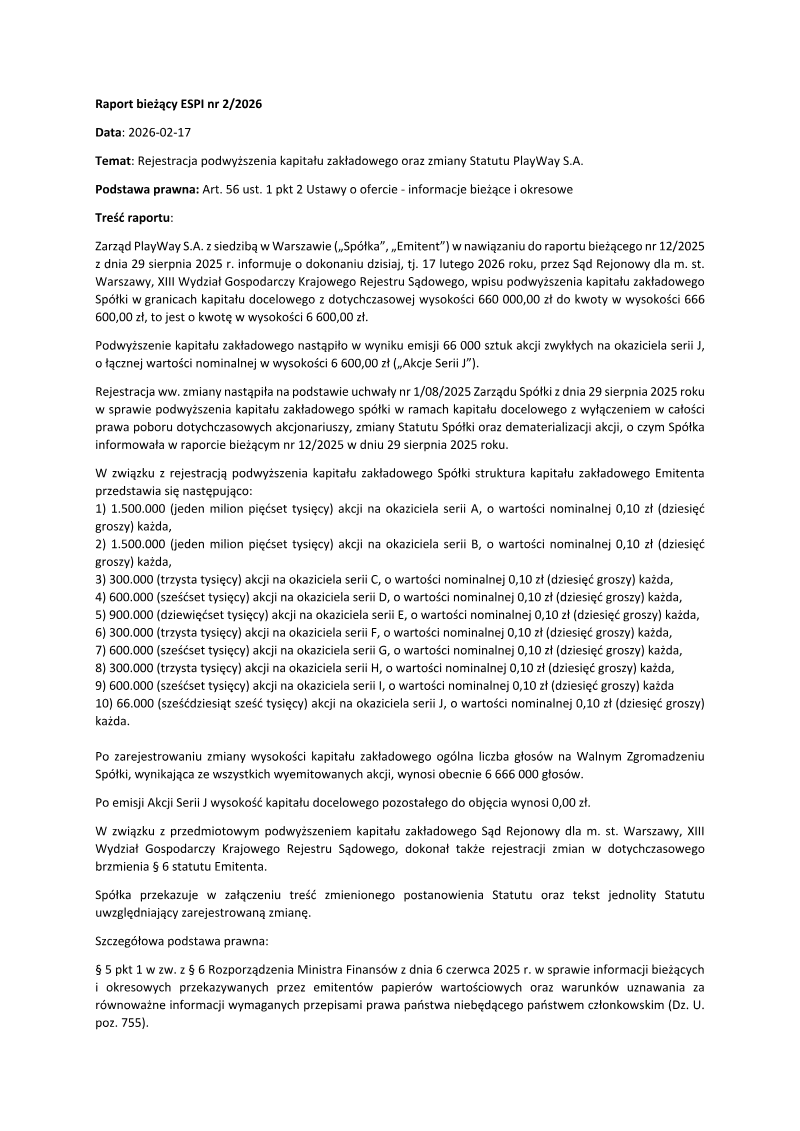

PlayWay · 2026

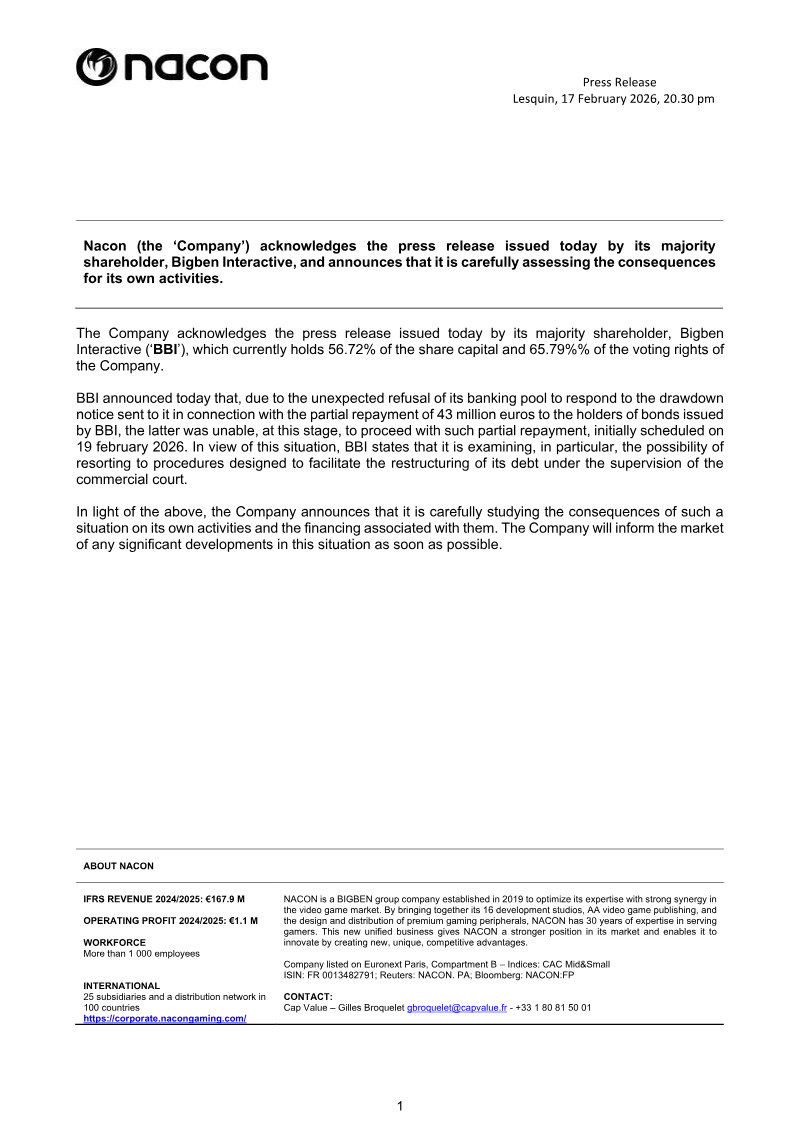

Nacon · 2026

Stillfront Group · 2026

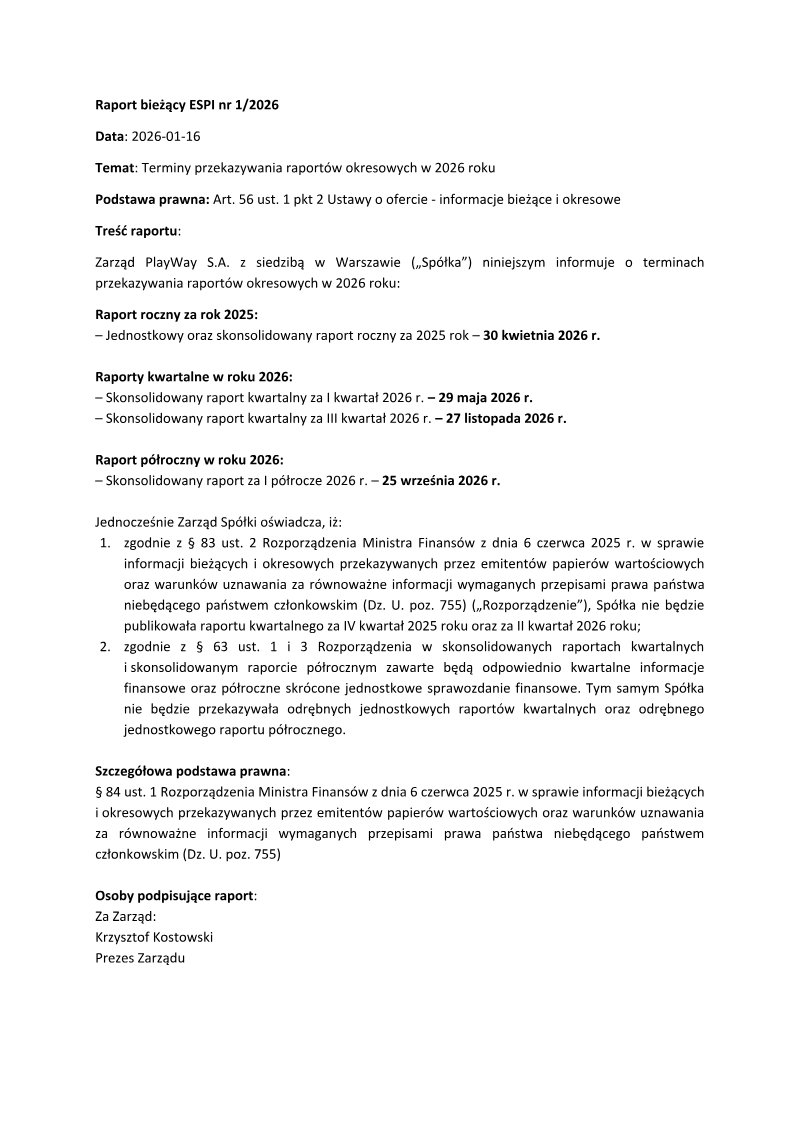

PlayWay · 2026

PCF Group · 2025

PCF Group · 2025

Video Games Europe · 2025

PCF Group · 2025

PCF Group · 2025

PCF Group · 2025

PCF Group · 2025