Key insights

2 takeaways · ~1 min read- 01

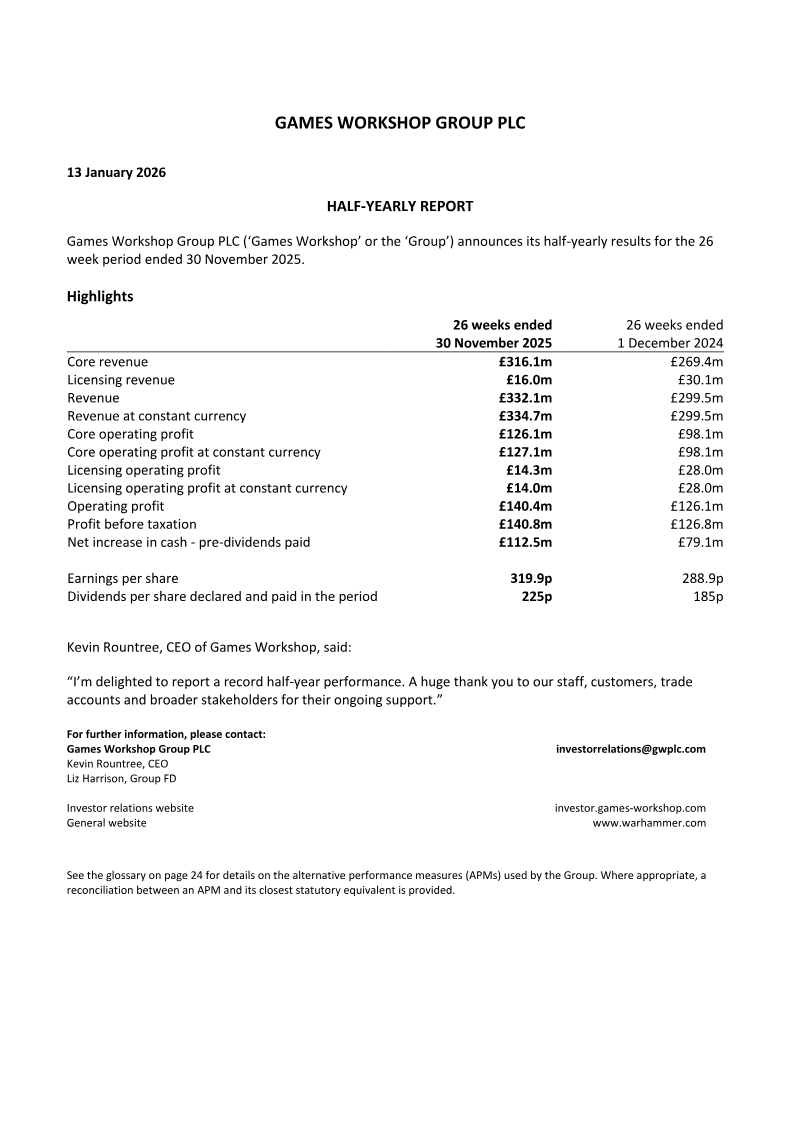

Games Workshop reported total revenue growth for the 26-week period ending 30 November 2025, driven by a core revenue increase to £316.1 million from £269.4 million in the prior year period.

See it on page 1 - 02

Licensing revenue experienced a significant decline, falling to £16.0 million for the period ending 30 November 2025 compared to £30.1 million for the period ending 1 December 2024.

See it on page 2

Summary

Games Workshop Group PLC (‘Games Workshop’ or the ‘Group’) announces its half-yearly results for the 26 week period ended 30 November 2025. 26 weeks ended 26 weeks ended 30 November 2025 1 December 2024 Core revenue £316.1m £269.4m Licensing revenue £16.0m £30.1m Revenue ...

Cite this report

Citation

Generating citation...