Related Documents

Financial

Gaming Report: VC Trends and Emerging Opportunities Q2 2023

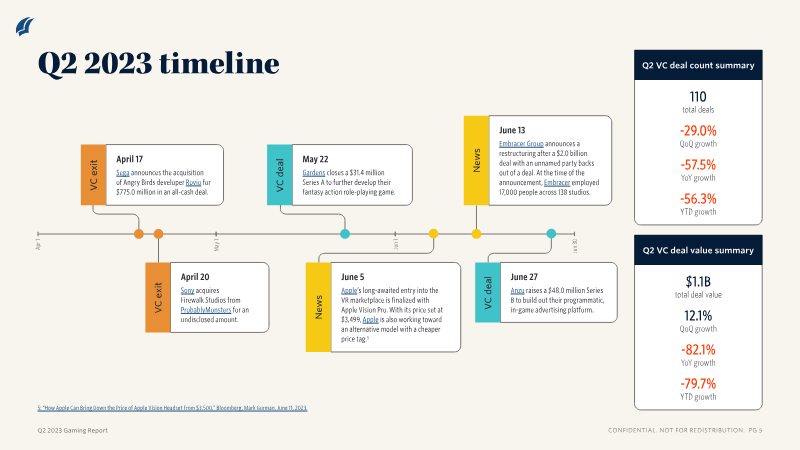

The gaming venture capital ecosystem experienced a period of significant transition in Q2 2023, characterized by a sharp decline in deal volume alongside a modest recovery in deal value. Total investment reached $1.1 billion across 110 deals, representing a 12.1% increase in value from the previous quarter but a substantial 57.5% year-over-year decrease in deal count. This data suggests a market shift toward larger, more concentrated investments in established players, even as early-stage and angel rounds continued to dominate the deal count at 71.8% of total activity. The scope of this analysis covers global gaming trends through the first half of 2023, with specific geographic focus on North America, which led with $1.3 billion in investment, followed by Asia and Europe. Industry segments analyzed include development, operations, access, content, and experience. Development and content emerged as the primary drivers of capital, nearly tied at approximately $488 million and $483 million in deal value, respectively. Notable transactions included CoreWeave’s $421.0 million Series B and Metagame’s $100.0 million early-stage round. Emerging opportunities are currently concentrated in user-generated content, cloud gaming, and novel monetization strategies. For example, Triumph Labs is highlighted for its plug-and-play SDK that enables real-money tournaments, addressing the technical and legal complexities of esports integration. While late-stage deals outperformed other categories in value for the first time since early 2022, the high volume of seed and angel activity indicates sustained investor optimism regarding long-term industry growth. The findings utilize proprietary PitchBook data and the Exit Predictor tool to estimate the likelihood of future IPOs or acquisitions for top-tier venture-backed companies like Epic Games and Niantic.

PitchBookAug 2023

Financial

Gaming Report: VC Trends and Emerging Opportunities Q3 2023

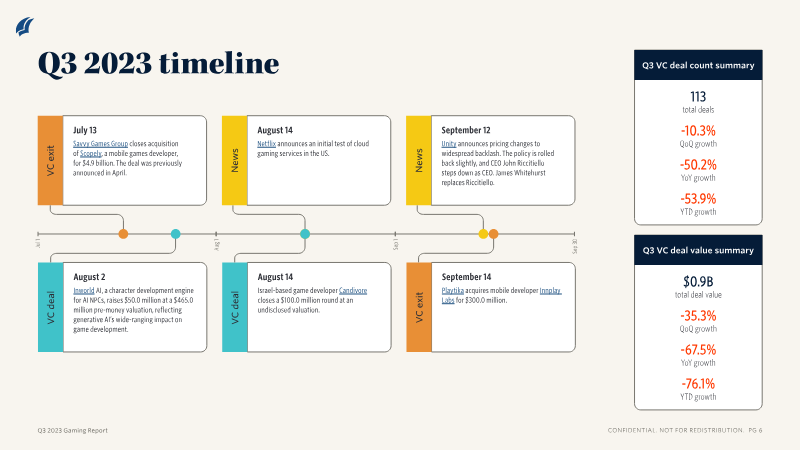

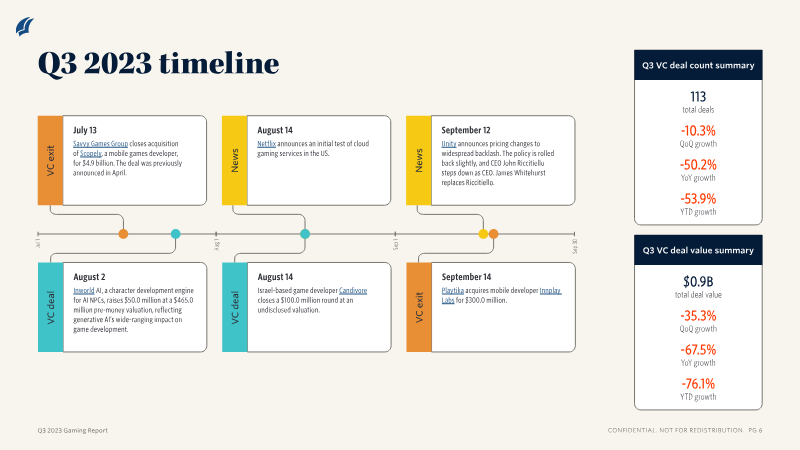

The report analyzes the state of venture‑backed gaming in the third quarter of 2023, highlighting a pronounced contraction in both deal volume and capital deployed across the global market. Total financing fell to $857 million across 113 transactions, a 10.3 % decline in deal count and a 35.3 % drop in value quarter‑over‑quarter, while year‑over‑year figures fell 50.2 % and 67.5 % respectively. Despite the downturn, cumulative investment for 2023 is projected to surpass 2019’s $3.7 billion, driven by sustained activity in the content segment, which attracted $514 million in 66 deals—more than double the next‑largest development segment. Early‑stage and seed financing accounted for $353 million, edging out late‑stage capital of $299 million and representing over 70 % of all VC activity to date. Late‑stage deals, however, grew to 46 % of YTD activity, reflecting a shift toward more mature ventures. Notable transactions included Inworld’s $50 million Series A for AI‑powered NPCs, Futureverse’s $54 million Series A in blockchain technology, and Luma AI’s $25.5 million early‑stage round for 3D asset generation. Top‑funded companies illustrate sector concentration: Epic Games leads with $5.75 billion raised, followed by Dream Sports, Voodoo, and Niantic. Exit probabilities derived from PitchBook’s proprietary VC Exit Predictor suggest a 29 % IPO likelihood for Epic Games and a 69 % chance of acquisition, underscoring the market’s M&A orientation. The analysis draws on PitchBook’s comprehensive private‑market database, covering global gaming firms up to September 30 2023, and integrates exit‑predictive modeling to assess future outcomes.

PitchBookNov 2023

Financial

Gaming Report: VC Trends and Emerging Opportunities

The gaming venture capital ecosystem experienced a notable contraction in the third quarter of 2023, with deal count and value declining significantly. Total investment fell to $857.0$ million across 113 deals, representing a 35.3% decrease in value and a 10.3% drop in volume compared to the previous quarter. On a year-over-year basis, the downturn is even more pronounced, with deal value sliding 67.5%. Despite these declines, the market appears to be stabilizing at a new baseline, with the last four quarters consistently generating between $800 million and $1.1 billion in investment. The content segment remains the primary driver of activity, securing $514.2 million in funding, which accounts for more than double the investment seen in the development segment. While early-stage deals led the quarter in total value at $353.0$ million, there has been a distinct shift in the broader market composition. Late-stage deals have increased their share of year-to-date activity to 46.1%, while venture growth deals have receded to just 5.8%. Notable transactions during this period include significant rounds for Candivore, Second Dinner, and AI-focused development platforms like Inworld and Luma AI. Emerging opportunities are increasingly concentrated at the intersection of gaming, artificial intelligence, and blockchain. Startups such as Story Protocol are gaining traction by developing open-source infrastructure to manage content provenance and intellectual property in response to the rise of generative AI. Geographically, the landscape remains global, featuring major players from the United States, France, India, and Turkey. While the industry is on pace to narrowly exceed 2019 investment levels, the current environment reflects a transition toward more disciplined, early-stage-heavy investment patterns following the volatility of previous years.

PitchBookNov 2023

Financial

Gaming Report: VC Trends and Emerging Opportunities Q4 2023

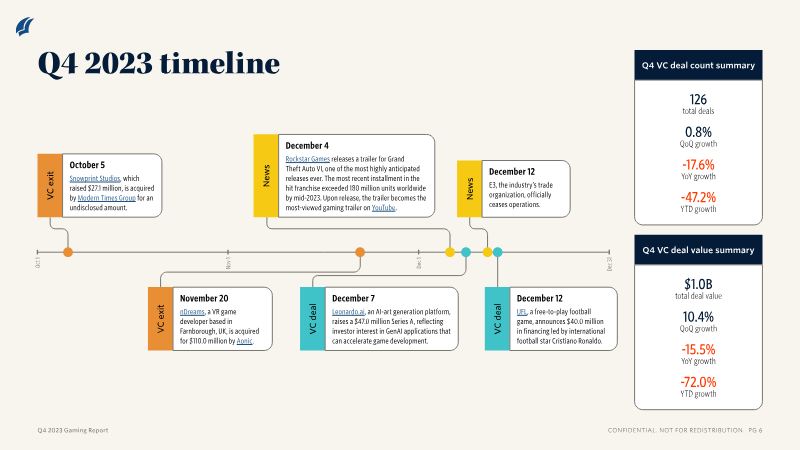

The analysis tracks global venture‑capital activity in the gaming sector for the fourth quarter of 2023, highlighting a modest rebound in deal volume and capital while underscoring a broader contraction relative to the pandemic‑driven peak years. Across the quarter, 126 deals generated roughly $1.0 billion in funding, marking a 0.8 % rise in deal count and a 10.4 % increase in value versus the previous quarter. Year‑over‑year, however, the market slipped 17.6 % in deals and 15.5 % in capital, with cumulative 2023 investment falling 47.2 % in count and 72 % in value compared with the prior twelve months. Total capital raised in 2023 reached $4.1 billion, slightly above 2019 levels but representing the second‑lowest annual total since 2017. Segment‑level allocation shows content‑focused startups attracting the largest share of funding—$438.4 million across 71 deals—followed by development firms with $288.7 million in 29 deals. The access segment recorded $150 million, driven largely by a single large transaction. Emerging opportunities identified include back‑end‑as‑a‑service platforms, anti‑toxicity and content‑moderation tools, and AI‑enhanced creation pipelines. Early‑stage highlights feature Stability AI’s $86 million development round, Leonardo.ai’s $47 million Series A, and Noice’s $21 million livestream venture, the latter projected with an 87 % probability of an M&A exit. Strategic acquisition patterns since 2019 reveal Unity, Sony Interactive Entertainment, and Tencent as the most active buyers, while venture investors such as BITKRAFT Ventures, Andreessen Horowitz, and Play Ventures dominate funding participation. The findings are derived from PitchBook’s global database of venture‑backed and growth‑stage gaming companies, employing deal‑count, valuation, and exit metrics to assess market dynamics.

PitchBookFeb 2024