Key insights

7 takeaways · ~3 min read- 01

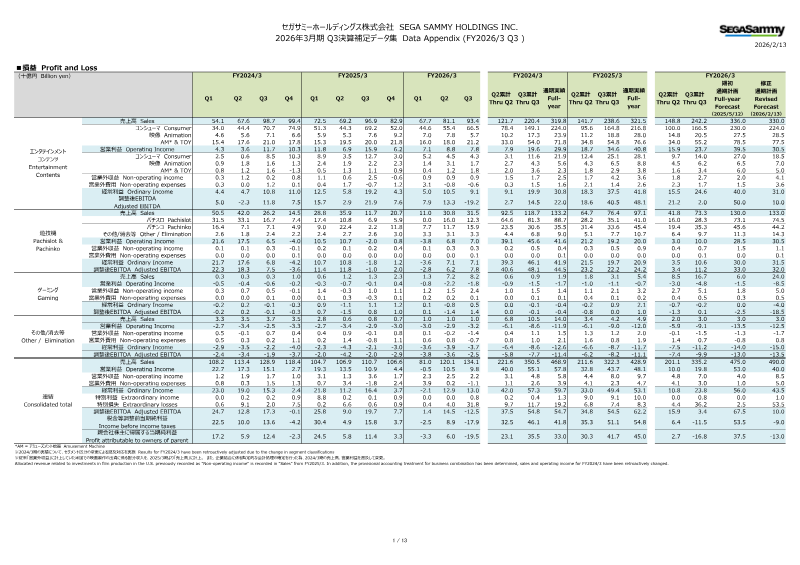

GREE Holdings met FY2025 targets with ¥53.8 billion in net sales and ¥5.3 billion in operating profit, while projecting FY2026 sales to grow to ¥58.1 billion.

See it on page 1 - 02

FY2026 operating profit is forecast to decline to ¥3.6 billion as the company prioritizes strategic investments in the Game segment over short-term margins.

See it on page 3 - 03

The Metaverse segment achieved 10% year-over-year sales growth, though profitability was impacted by one-off costs related to VTuber talent.

See it on page 5 - 04

The Game segment remains a core revenue driver, posting ¥9.1 billion in 4Q sales with an 18% operating margin, supported by titles like 'That Time I Got Reincarnated as a Slime: ISEKAI Memories'.

See it on page 3 - 05

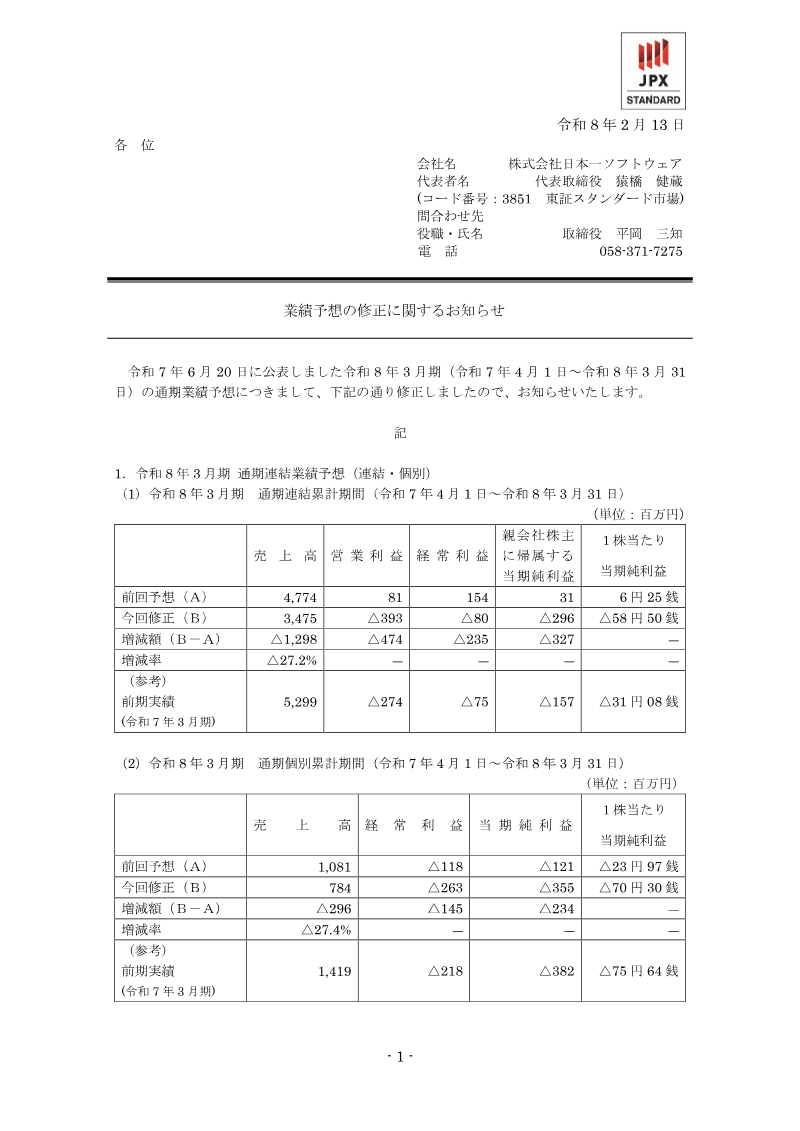

The company will issue a ¥14.5 per share dividend for FY2025, consisting of a ¥4.5 regular dividend and a ¥10 commemorative payout for its 20th anniversary.

See it on page 2 - 06

Financial stability remains high, with the company exceeding its equity ratio target of 60% and maintaining a debt-to-EBITDA ratio below 6x.

See it on page 2 - 07

Management is targeting a 10% ROIC by FY2030, supported by a balanced portfolio that includes increased LP investments and growth in the DX and IP segments.

See it on page 9