FinancialKoei Tecmo

Financial Results for the First Half of the Fiscal Year Ending March 2011

1 Mar 201134 pages~9 min full read

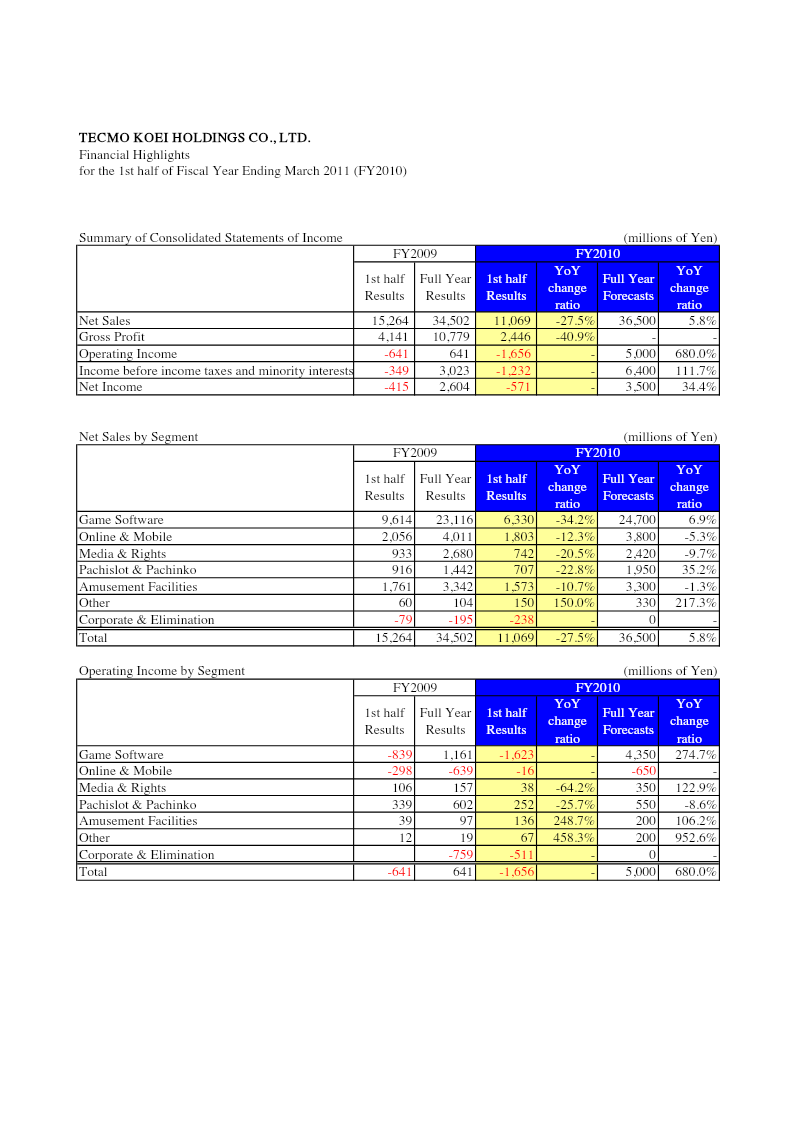

Tecmo Koei achieved its first-ever first-half operating profit of 712 million Yen for the period ending March 2011, reversing a 1.6 billion Yen loss from the previous year.

Net sales grew to 13.6 billion Yen, up from 11.1 billion Yen in the prior year, driven by disciplined resource allocation and cost-reduction measures.

The Online & Mobile segment experienced significant growth, with sales increasing from 1.8 billion Yen to 2.8 billion Yen.

Japan remains the company's primary market, accounting for 86.7% of total sales.

Strategic growth plans include expanding social gaming on platforms like Mobage, GREE, and Tencent, alongside development support for the Nintendo 3DS and PlayStation Vita.

The company is targeting 35 billion Yen in annual sales, supported by cross-IP integration and high-profile collaborations such as One Piece Kaizoku Musou.

This financial report details the performance of Tecmo Koei Holdings for the first half of the fiscal year ending March 2011. The primary thesis centers on the company’s successful transition to profitability following the merger of Koei and Tecmo, achieving its first-ever first-half operating profit. Net sales for the period reached 13.6 billion Yen, a significant increase from 11.1 billion Yen in the previous year, while operating profit swung from a 1.6 billion Yen loss to a 712 million Yen gain.

The scope of the data covers global operations, though Japan remains the dominant market, accounting for 86.7% of sales. While the Game Software segment remains the largest revenue driver, the Online & Mobile segment showed robust growth, with sales increasing from 1.8 billion Yen to 2.8 billion Yen. Management attributes this recovery to disciplined resource allocation toward profitable titles, stable contributions from the social gaming sector, and aggressive cost-reduction measures that lowered selling, general, and administrative expenses.

Strategic priorities for the remainder of the fiscal year include doubling growth in social gaming through global expansion on platforms like Mobage, GREE, and Tencent, and supporting new hardware launches such as the Nintendo 3DS and PlayStation Vita. The company is also emphasizing "group synergy" by crossing over legacy IPs, such as the integration of Tecmo’s horse racing mechanics into combined titles. Looking forward, the company plans to reach 35 billion Yen in annual sales, driven by a shift toward multiplayer-centric play styles and high-profile collaborations like the One Piece Kaizoku Musou project.