Financialmixi

Consolidated Financial Results for the Six Months Ended September 30, 2017

1 Nov 20178 pages~13 min full read

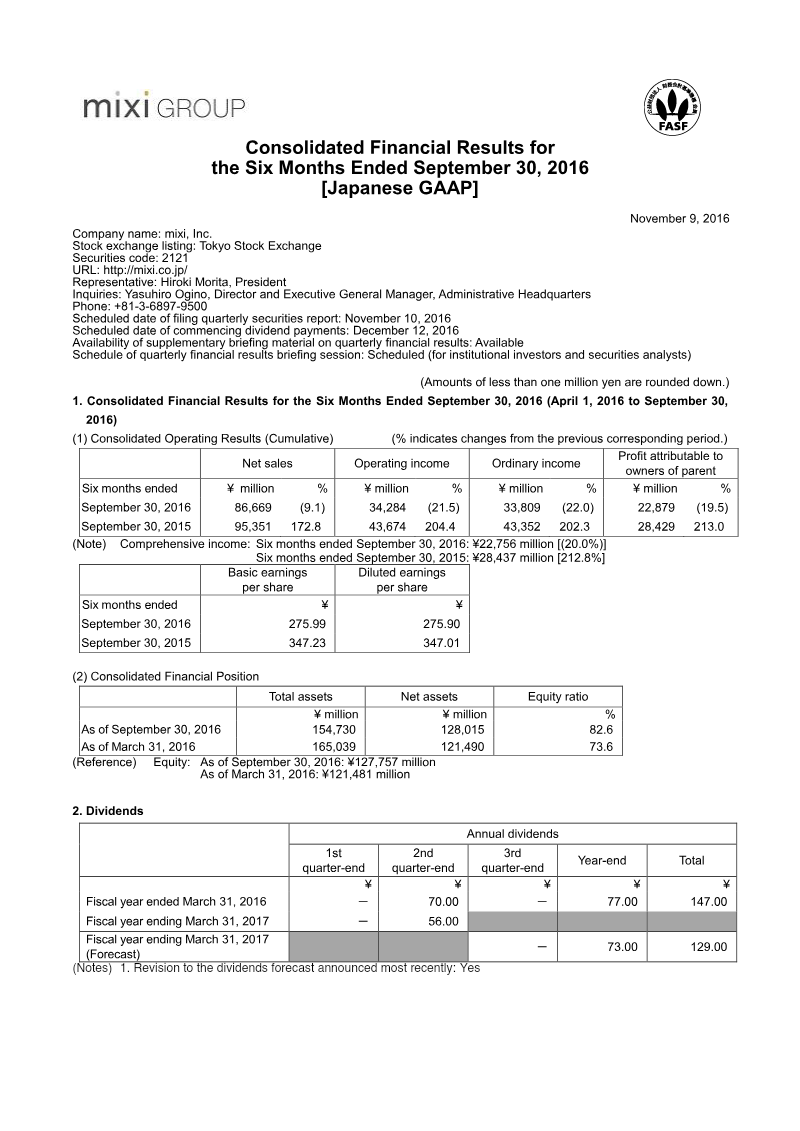

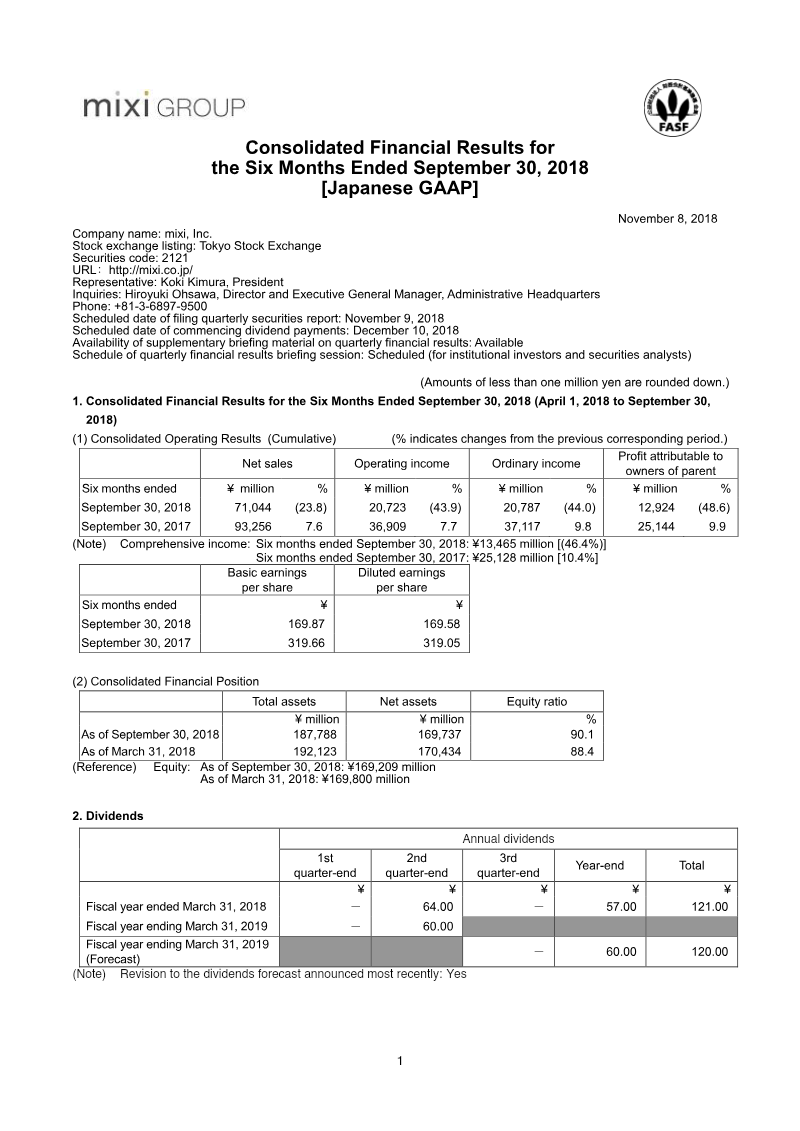

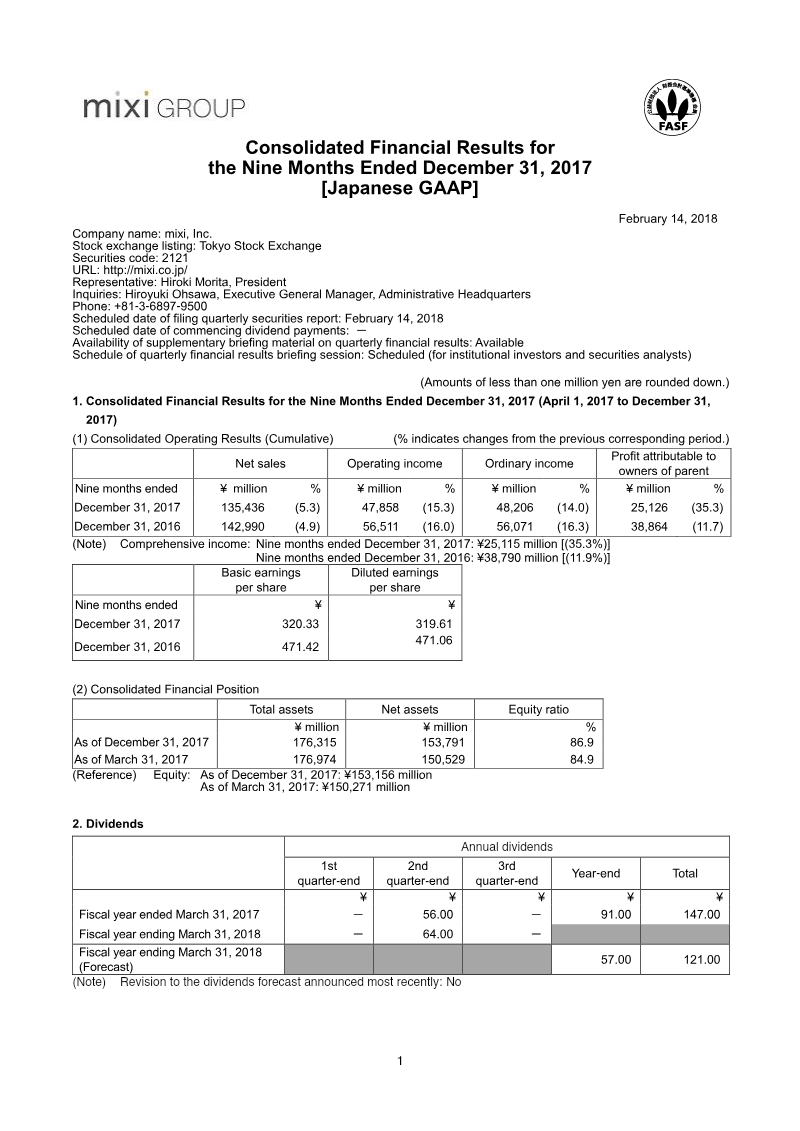

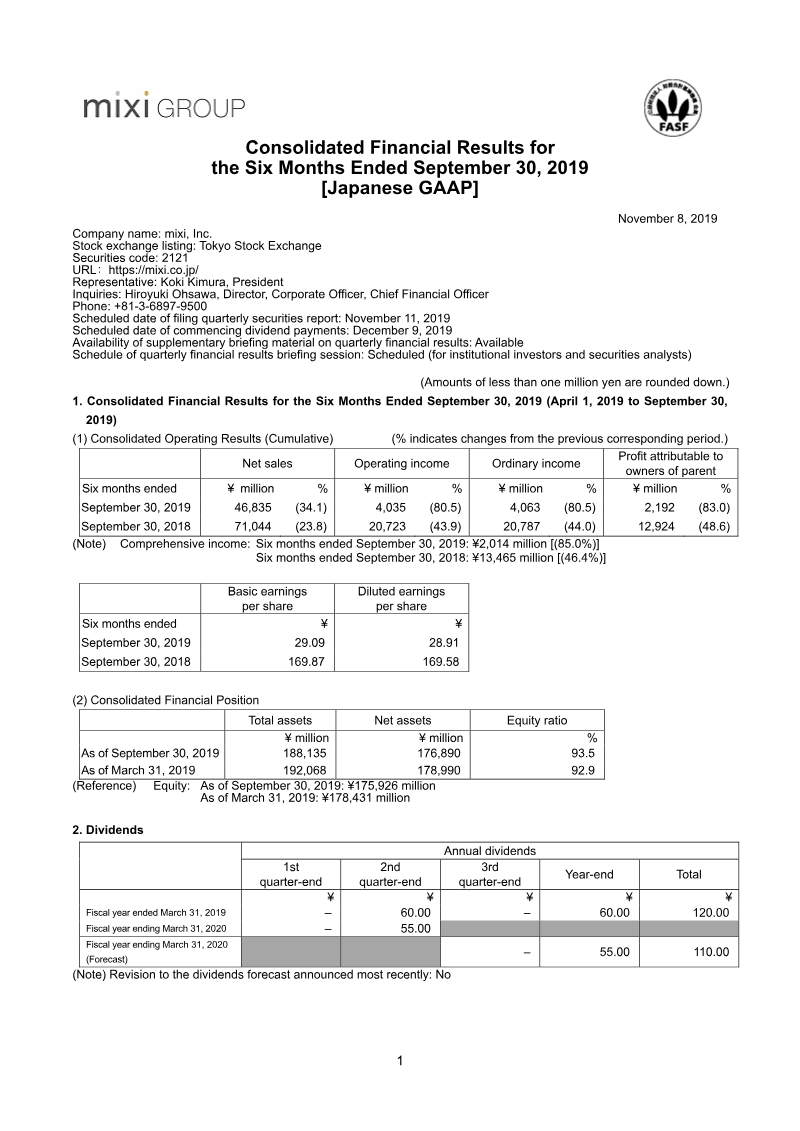

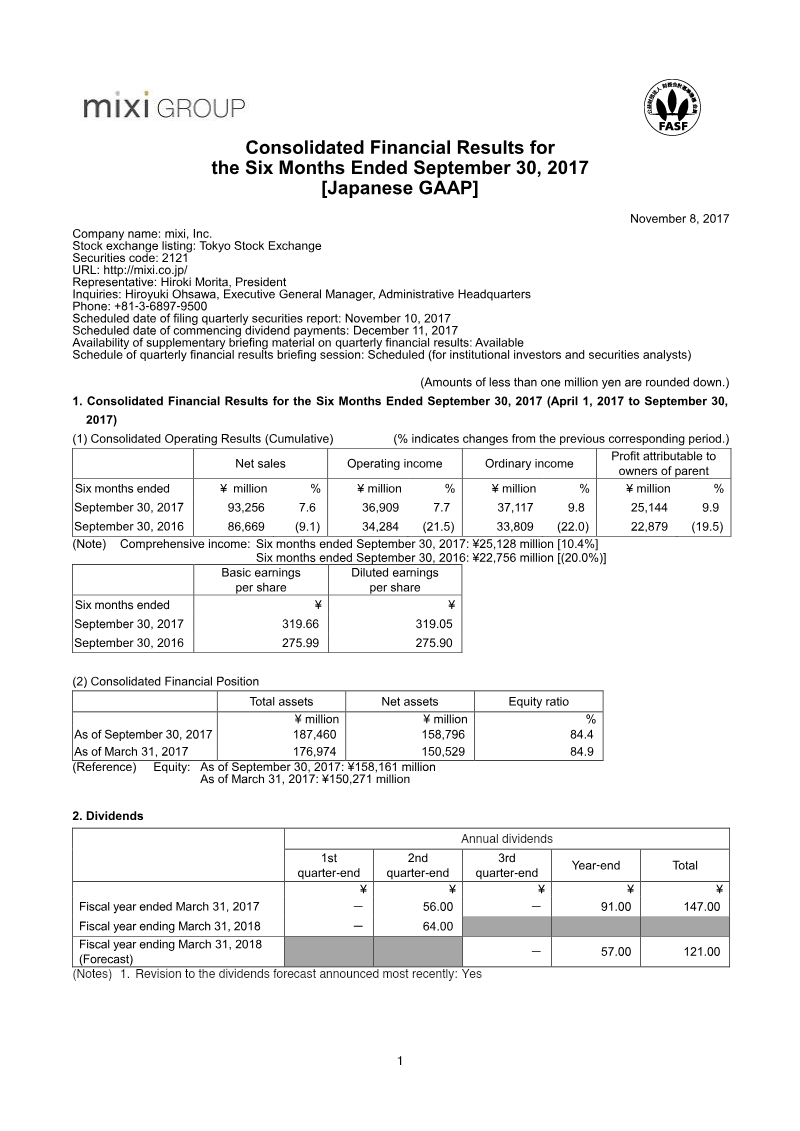

Mixi, Inc. reported strong H1 growth for the fiscal year ending March 31, 2018, with net sales rising 7.6% to ¥93,256 million and operating income increasing 7.7% to ¥36,909 million.

See it on page 1The Entertainment Business segment remains the primary driver of performance, generating ¥86,252 million in external sales and ¥39,087 million in segment profit.

See it on page 7Despite positive mid-year results, the company projects a conservative full-year outlook with anticipated declines in annual net sales of 3.5% and operating income of 21.4%.

See it on page 2The forecasted decline in annual profitability is attributed to rising SG&A expenses, including costs related to the company's planned 2019 head office relocation to Shibuya Scramble Square.

See it on page 8Profit attributable to owners of the parent grew 9.9% year-over-year to ¥25,144 million, supported by robust operating cash flow of ¥29,553 million.

See it on page 5The company maintains a strong balance sheet with an equity ratio of 84.4% and total assets valued at ¥187,460 million.

See it on page 3Strategic capital management during the period included the retirement of over 3.6 million treasury shares, the repurchase of 1.5 million shares, and a revised annual dividend forecast of ¥121.00 per share.

See it on page 7Mixi, Inc. reported consolidated financial results for the first half of the fiscal year ending March 31, 2018, covering the period from April 1, 2017, to September 30, 2017. During this six-month window, the company experienced growth across all primary financial metrics compared to the previous year. Net sales rose 7.6% to ¥93,256 million, while operating income increased 7.7% to ¥36,909 million. Profit attributable to owners of the parent reached ¥25,144 million, representing a 9.9% year-over-year increase. The company maintained a strong financial position with an equity ratio of 84.4% and total assets valued at ¥187,460 million.

Performance was driven largely by the Entertainment Business segment, which accounted for ¥86,252 million in external sales and ¥39,087 million in segment profit. The Media Platform Business contributed ¥7,003 million in sales and ¥1,675 million in profit. Despite the positive mid-year results, the full-year forecast suggests a conservative outlook, with anticipated declines in annual net sales and operating income of 3.5% and 21.4%, respectively. This outlook factors in rising selling, general, and administrative expenses, including costs associated with the planned relocation of the head office to Shibuya Scramble Square scheduled for 2019.

Strategic financial activities during the period included significant treasury share transactions, including the retirement of over 3.6 million shares and the repurchase of 1.5 million shares. Cash flow remains robust, with net cash provided by operating activities increasing significantly to ¥29,553 million. The company also revised its dividend forecast, projecting a total annual dividend of ¥121.00 per share. These results, prepared under Japanese GAAP, reflect a period of operational stability and strategic consolidation as the company prepares for future infrastructure changes and business expansion.