Financialmixi

Consolidated Financial Results for the Nine Months Ended December 31, 2017

1 Feb 20189 pages~13 min full read

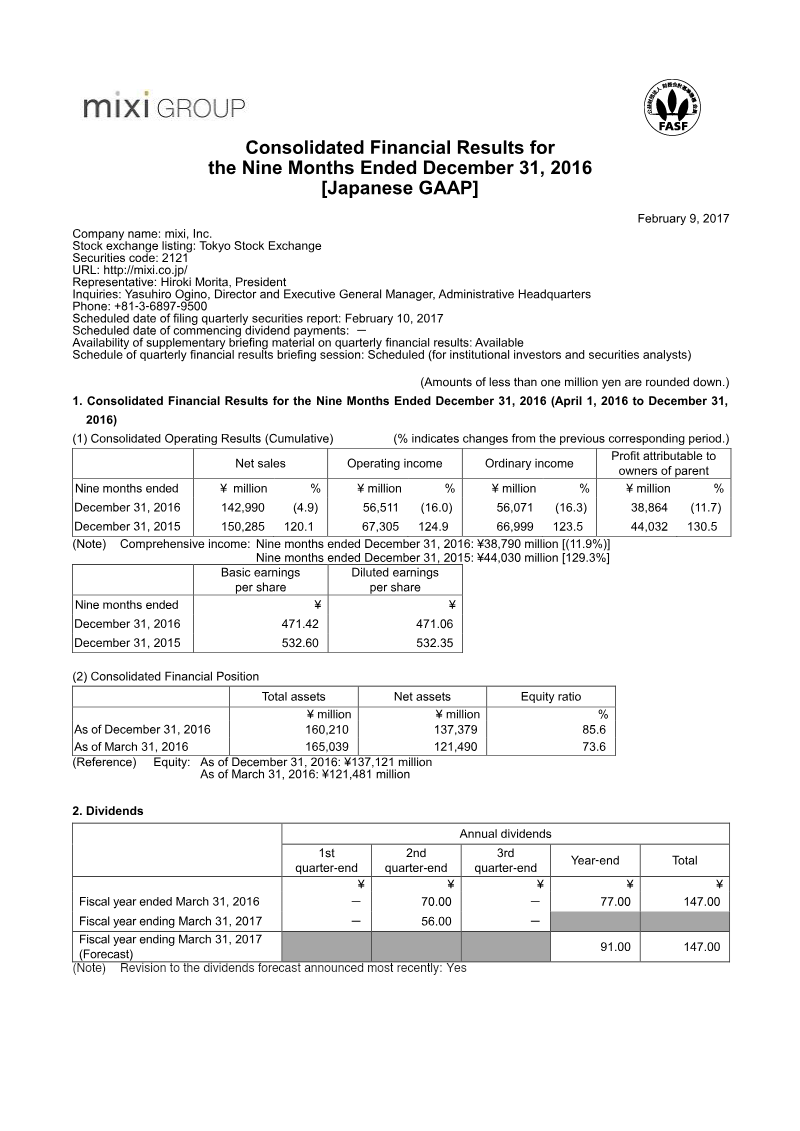

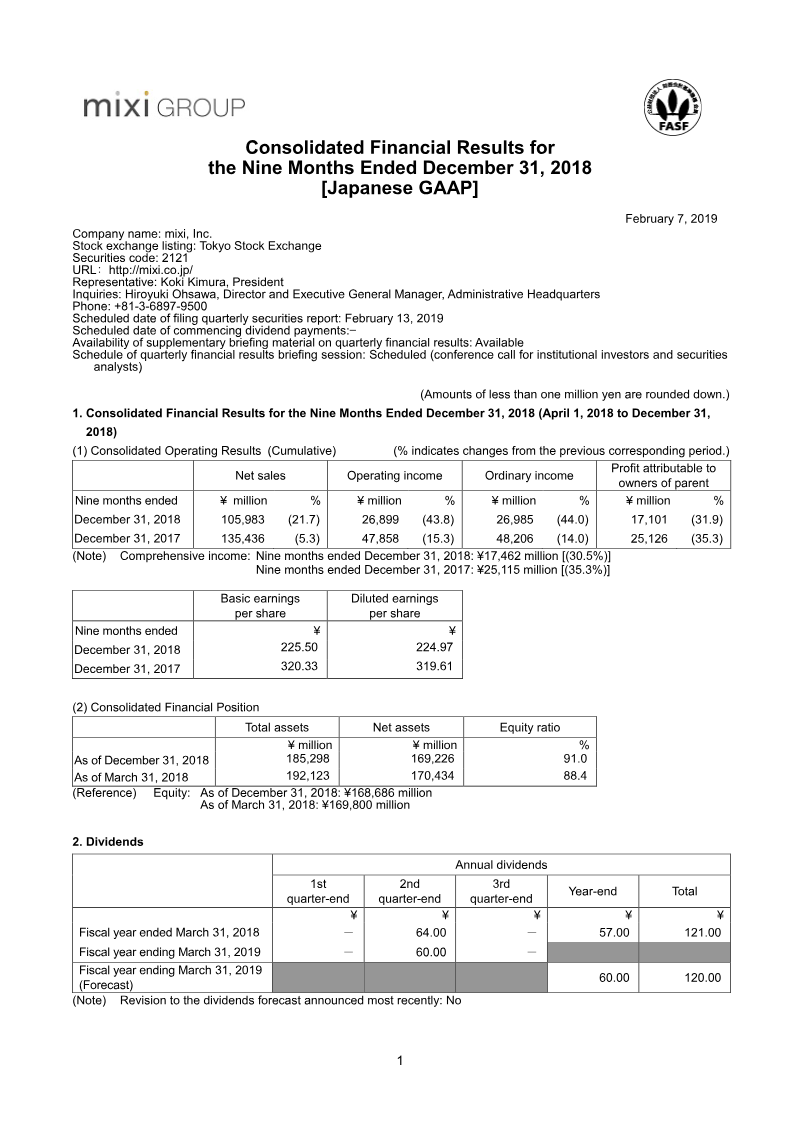

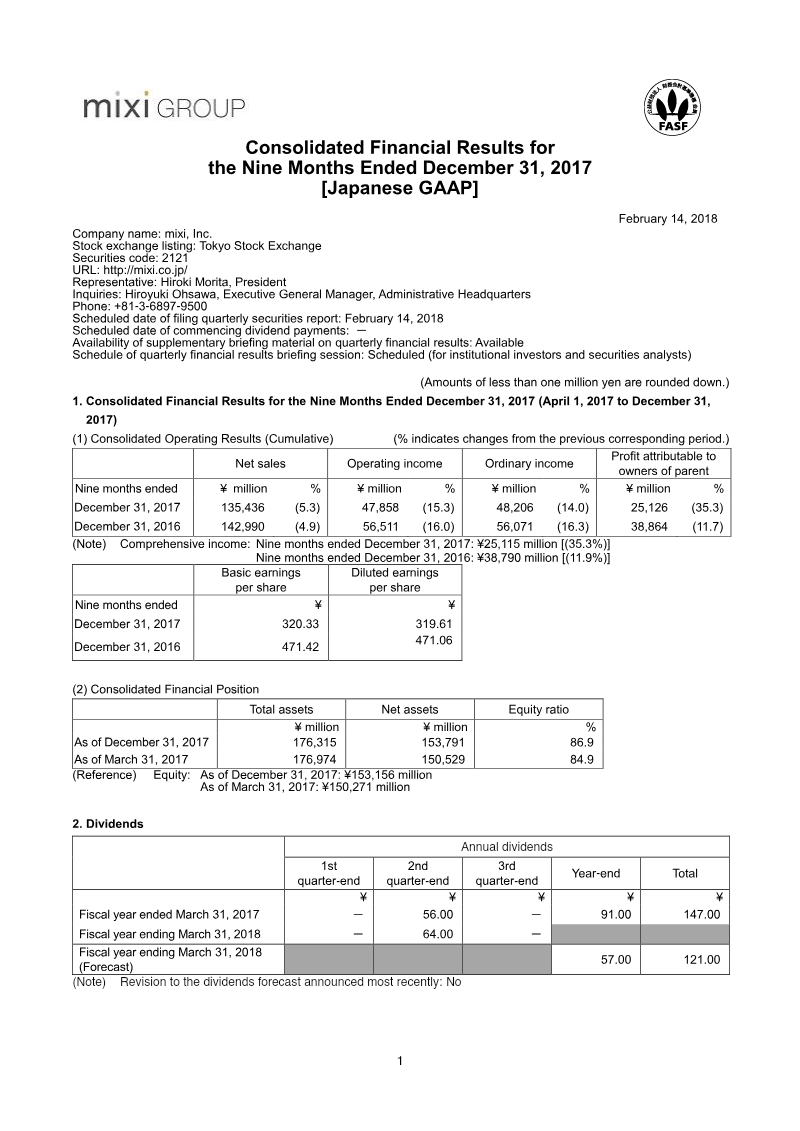

Mixi, Inc. reported a 35.3% decline in profit attributable to owners of the parent to ¥25.1 billion for the nine months ended December 31, 2017, largely due to a ¥7.59 billion extraordinary loss from the full amortization of goodwill for Ticket Camp.

Consolidated net sales fell 5.3% to ¥135.4 billion, while operating income decreased 15.3% to ¥47.8 billion compared to the same period in the previous fiscal year.

The Entertainment Business remains the primary revenue driver, contributing ¥124.5 billion in sales, though this represents a decline from the ¥131.8 billion generated in the prior year.

The company terminated the Ticket Camp service operated by subsidiary Hunza, Inc. during the third quarter, incurring an additional impairment loss of ¥131 million alongside the goodwill amortization.

Despite the profit contraction, Mixi maintains a stable financial position with an equity ratio of 86.9% and cash and cash equivalents totaling ¥136.7 billion.

Management reaffirmed its full-year forecast of ¥200 billion in net sales and ¥40.2 billion in profit, while maintaining a planned annual dividend of ¥121.00 per share.

Mixi, Inc. reported consolidated financial results for the first nine months of the fiscal year ending March 31, 2018, reflecting a period of contraction compared to the previous year. Net sales reached ¥135.4 billion, a 5.3% decrease, while operating income fell 15.3% to ¥47.8 billion. The most significant decline was observed in profit attributable to owners of the parent, which dropped 35.3% to ¥25.1 billion. This sharp decrease in net profit was largely driven by a substantial extraordinary loss of ¥7.59 billion related to the full amortization of goodwill for the Ticket Camp service.

The company’s operations are divided into two primary segments: the Entertainment Business and the Media Platform Business. The Entertainment Business remains the dominant revenue driver, contributing ¥124.5 billion in sales, though this was down from ¥131.8 billion in the prior year. The Media Platform Business saw a slight decline in sales to ¥10.8 billion. A critical development during the third quarter was the decision to terminate the Ticket Camp service operated by subsidiary Hunza, Inc., resulting in the aforementioned goodwill amortization and an additional impairment loss of ¥131 million.

Despite the decline in profitability, the financial position remains stable with an equity ratio of 86.9% and total assets of ¥176.3 billion. Cash and cash equivalents increased to ¥136.7 billion, supported by strong net cash provided by operating activities. The company maintained its full-year forecast, projecting net sales of ¥200 billion and a profit of ¥40.2 billion. Dividend forecasts were also reaffirmed, with a planned total annual dividend of ¥121.00 per share, reflecting a commitment to shareholder returns despite the non-recurring losses associated with the closure of the Ticket Camp platform.