FinancialKLab

Summary of Financial Results for Fiscal Year Ending December 31, 2019 (Japanese GAAP) (Consolidated)

1 Feb 202017 pages~25 min full read

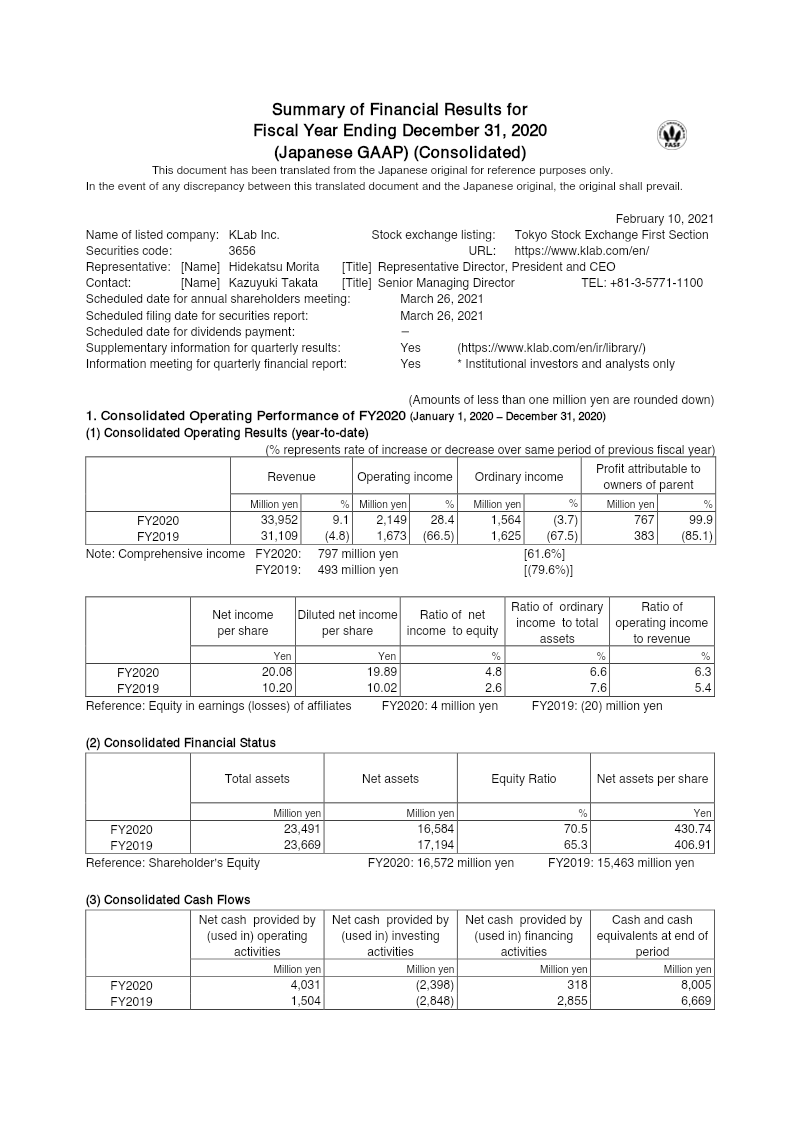

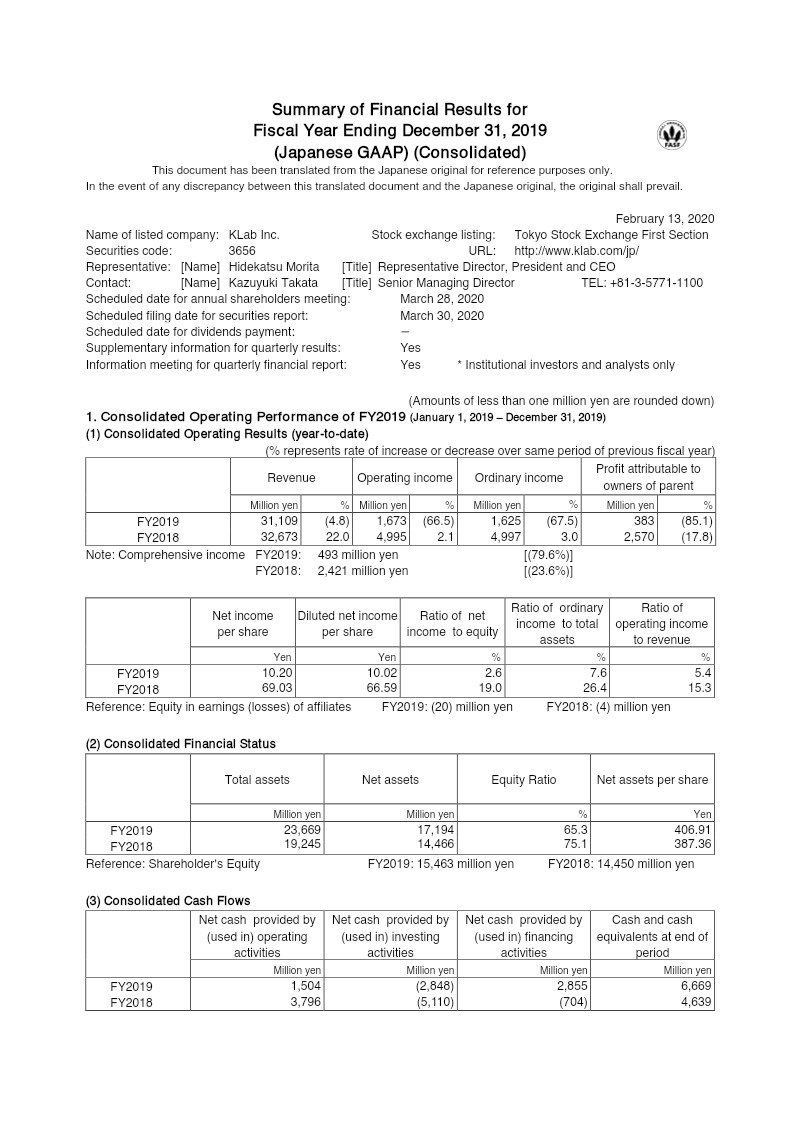

KLab Inc. experienced a significant profitability contraction in fiscal year 2019, with net profit falling 85.1% to 383 million yen and operating income dropping from 5.0 billion yen to 1.7 billion yen.

See it on page 5Total revenue for the year declined by 4.8% to 31.1 billion yen, primarily due to the natural lifecycle decline of older titles and high operational expenses.

See it on page 5A substantial 1.3 billion yen impairment loss related to the title 'Magatsu Wahrheit' significantly impacted the company's bottom line.

See it on page 5The Game Business remains the company's primary revenue driver, accounting for nearly 99% of total revenue, with 'Captain Tsubasa: Dream Team' and 'BLEACH Brave Souls' serving as key international performers.

See it on page 5Despite reduced operating cash flows, the company maintained a resilient balance sheet with total assets growing to 23.6 billion yen and cash and equivalents stabilized at 6.7 billion yen through 2.3 billion yen in new long-term debt.

See it on page 5KLab Inc. projects a revenue recovery for the 2020 fiscal year, forecasting a range between 35 and 40 billion yen based on aggressive growth strategies and new title releases.

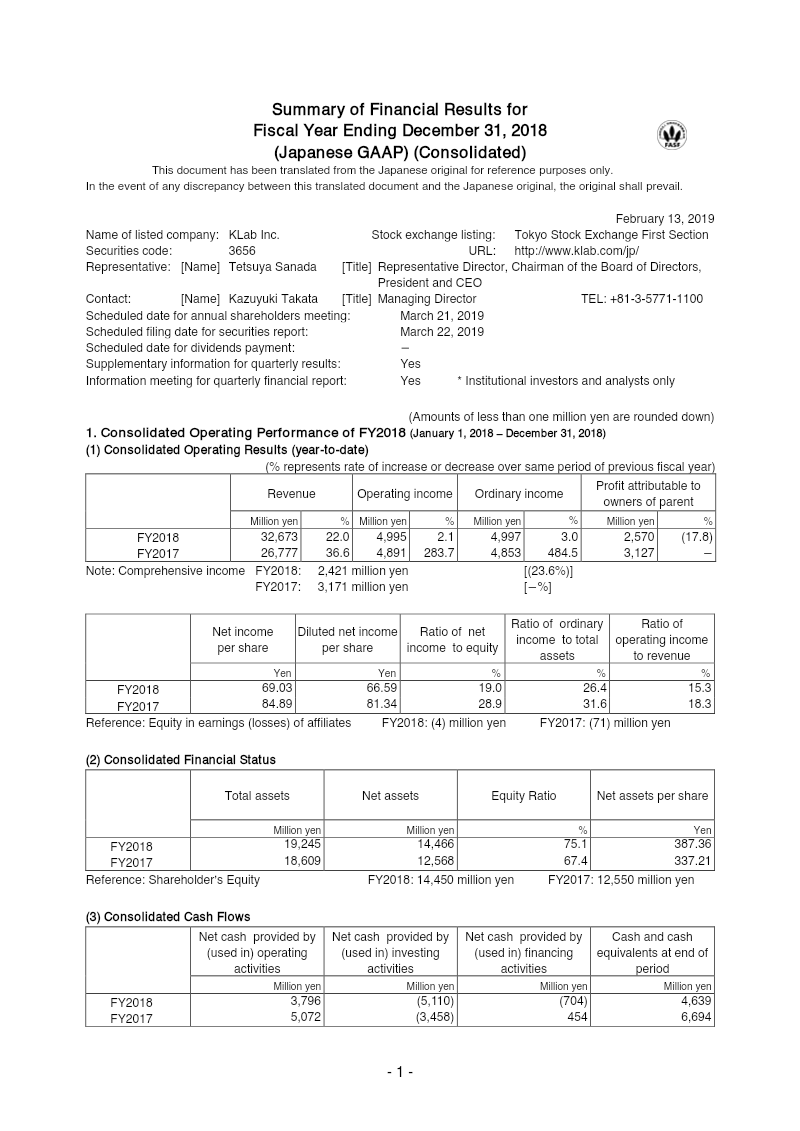

See it on page 6The fiscal year ending December 31, 2019, was characterized by a contraction in profitability for KLab Inc. despite the continued global strength of its core intellectual properties. Total revenue declined by 4.8% to 31.1 billion yen, while net profit experienced a sharp 85.1% drop, falling to 383 million yen. This downturn was primarily driven by rising labor costs, increased depreciation, and a substantial 1.3 billion yen impairment loss associated with the title Magatsu Wahrheit. While established games such as Captain Tsubasa: Dream Team and BLEACH Brave Souls maintained strong international performance, the natural decline of older titles and high operational expenses significantly compressed operating income from 5.0 billion yen to 1.7 billion yen.

The Game Business remains the central pillar of the organization, accounting for nearly 99% of total revenue. Despite the decline in net income per share from 69.03 yen to 10.20 yen, the corporate balance sheet showed resilience. Total assets grew to 23.6 billion yen, and net assets increased to 17.2 billion yen, supported by higher retained earnings and the strategic acquisition of 2.3 billion yen in long-term debt. This influx of capital helped stabilize cash and equivalents at 6.7 billion yen, providing a buffer against the year’s reduced operating cash flows.

Looking toward the 2020 fiscal year, revenue is projected to recover to a range between 35 and 40 billion yen. This forecast reflects an aggressive growth strategy dependent on the successful lifecycle management of existing titles and the performance of new releases. While the 2019 results highlight the volatility inherent in the mobile gaming sector and the impact of high development costs on margins, the expansion of software assets and a strengthened capital base suggest a focus on long-term scaling within the Japanese and global markets.