FinancialAkatsuki

Consolidated Financial Statements for the Third Quarter of Fiscal Year Ending March 31, 2026 (Japanese GAAP)

1 Feb 202611 pages~25 min full read

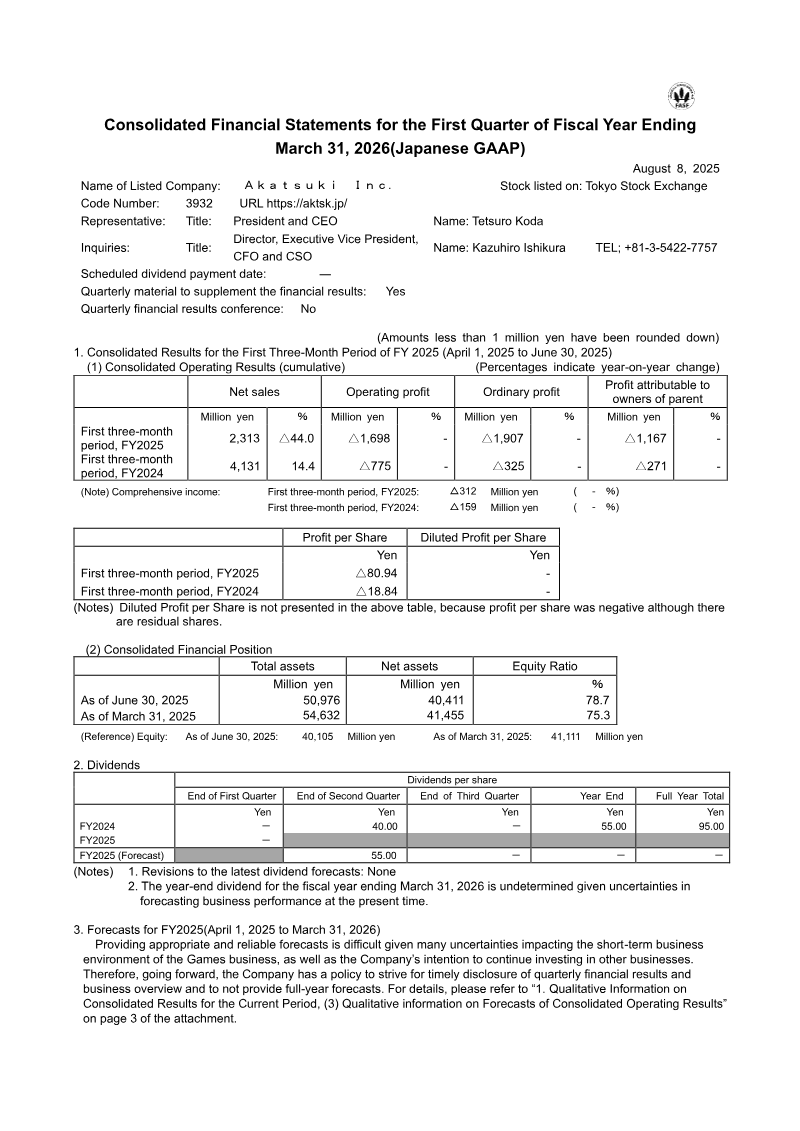

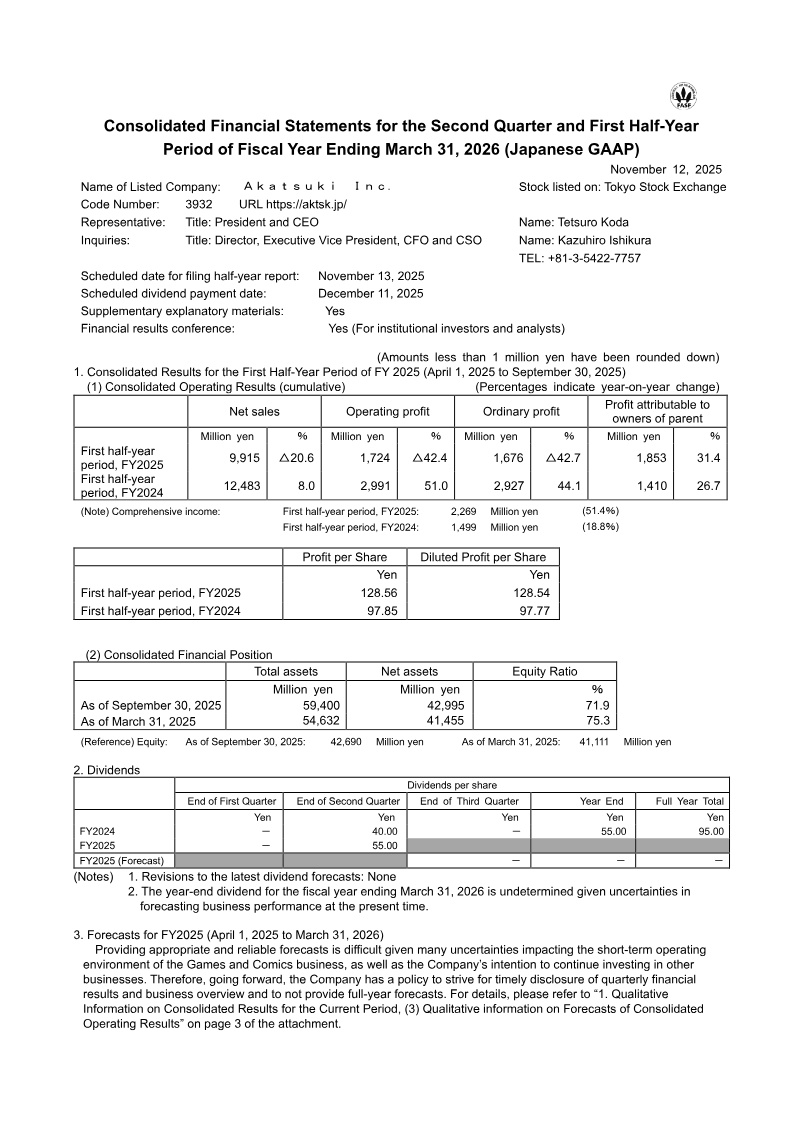

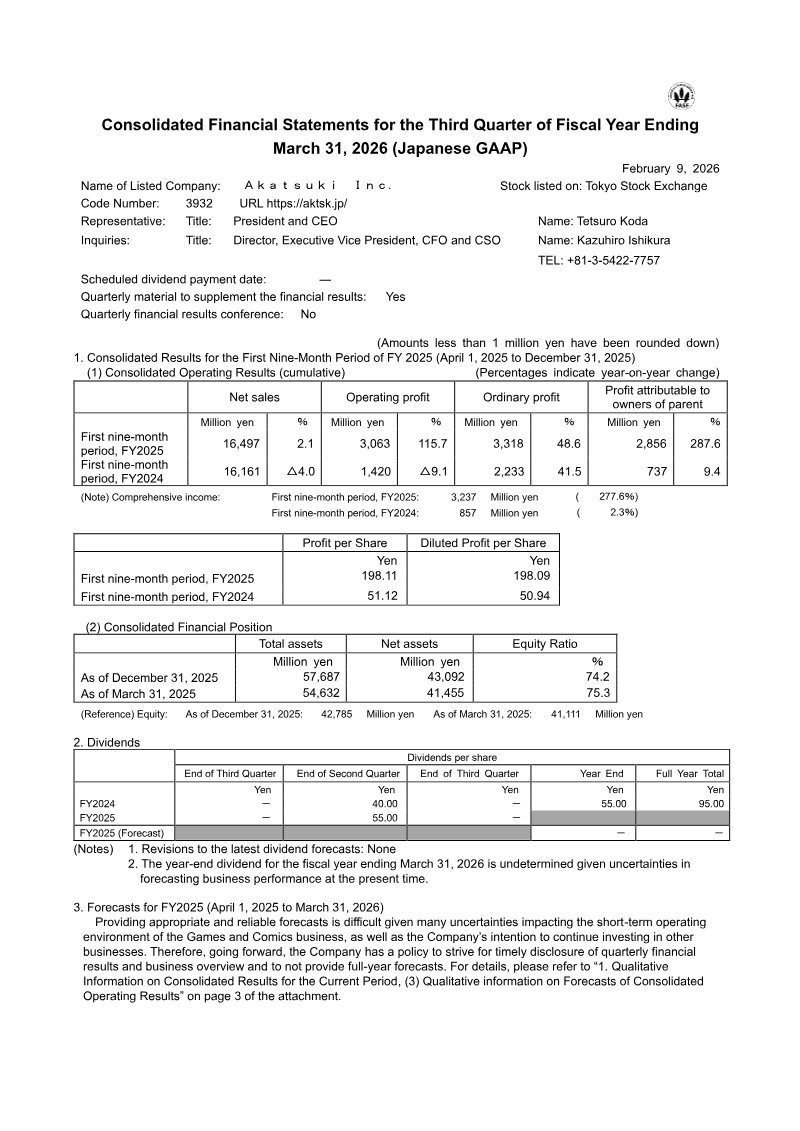

Akatsuki Inc. reported a 287.6% surge in profit attributable to owners to ¥2,856 million for the first nine months of the fiscal year ending March 31, 2026, despite a modest 2.1% increase in net sales to ¥16,497 million.

See it on page 1The Games and Comics segment saw segment profit more than double to ¥3,391 million, driven by operational efficiencies, the liquidation of underperforming subsidiaries, and the August 2025 launch of Kaiju No. 8 The Game.

See it on page 4The company underwent a major restructuring to establish three new reporting segments: Games and Comics, Entertainment and Lifestyle, and AI/DX Solutions.

See it on page 11Strategic acquisitions including CRAYON, Inc., PAPABUBBLE, Inc., and Natee Inc. contributed to a ¥3,880 million increase in goodwill as part of a diversification strategy into lifestyle brands and technology integration.

See it on page 9Management has declined to provide a full-year earnings forecast for the fiscal year ending March 31, 2026, citing gaming sector volatility and the impact of ongoing heavy investment activities.

See it on page 1Revenue diversification efforts include the growth of the Slash Gift online lottery service, which is contributing to the company's broader financial stability within the Japanese market.

See it on page 4Akatsuki Inc. demonstrated significant financial growth during the first nine months of the fiscal year ending March 31, 2026, characterized by a substantial increase in profitability despite modest revenue gains. Net sales rose 2.1% to ¥16,497 million, while profit attributable to owners surged by 287.6% to reach ¥2,856 million. This performance was primarily driven by enhanced operational efficiencies within the core Games and Comics segment and the successful market entry of new intellectual properties, most notably the August 2025 launch of Kaiju No. 8 The Game. Although the gaming division experienced a slight decline in top-line revenue, its segment profit more than doubled to ¥3,391 million, reflecting a strategic shift toward high-margin operations and the liquidation of underperforming subsidiaries.

The company expanded its operational scope through aggressive diversification and restructuring, establishing a new reporting framework consisting of Games and Comics, Entertainment and Lifestyle, and AI/DX Solutions. Strategic acquisitions played a pivotal role in this evolution, with the consolidation of entities such as CRAYON, Inc., PAPABUBBLE, Inc., and Natee Inc. contributing to a ¥3,880 million increase in goodwill. These investments bolstered the Entertainment and Lifestyle portfolio and provided the foundation for the new AI/DX Solutions segment, signaling a long-term commitment to integrating technology and lifestyle brands into the broader entertainment ecosystem.

Geographically focused on the Japanese market for the period ending December 31, 2025, the financial results indicate a robust balance sheet bolstered by diversified revenue streams, including the growth of the Slash Gift online lottery service. However, management has opted not to provide a full-year earnings forecast, citing inherent volatility in the gaming sector and the ongoing impact of heavy investment activities. This cautious outlook underscores a focus on long-term structural growth and IP development over short-term predictability.