FinancialCOLOPL

Consolidated Financial Results for the Three Months Ended December 31, 2025 (under Japanese GAAP)

1 Feb 202610 pages~15 min full read

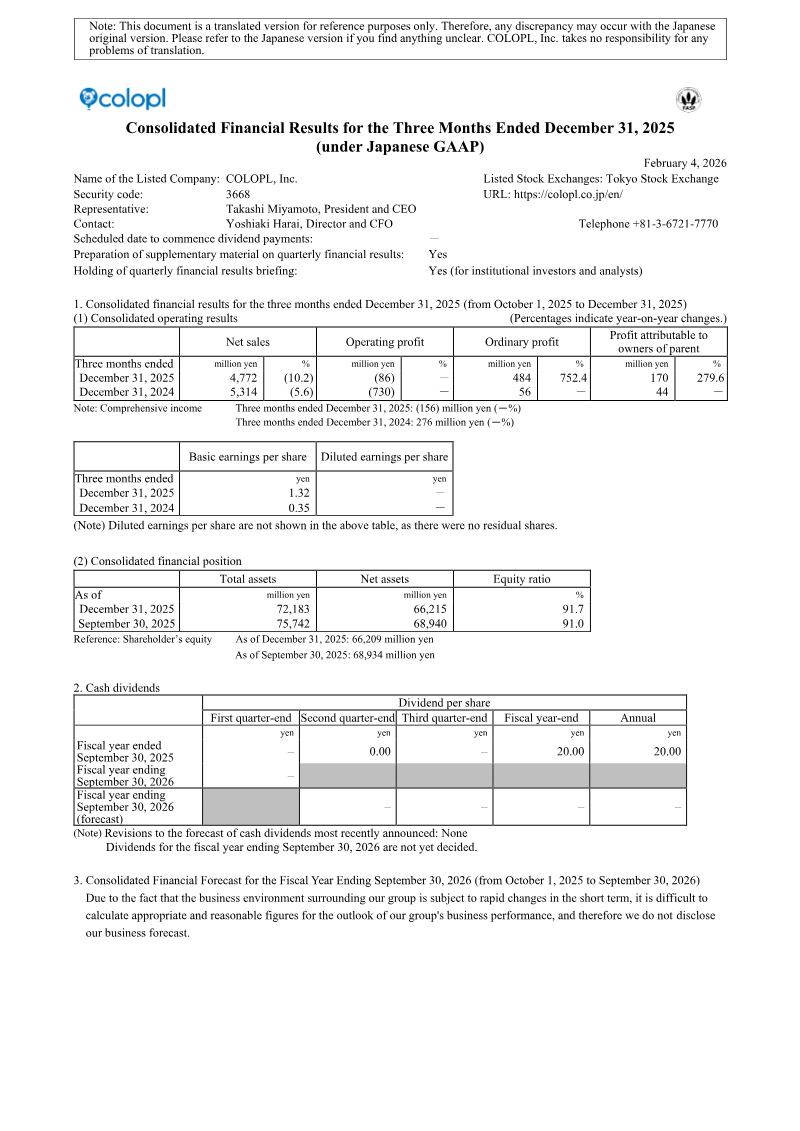

COLOPL reported a 10.2% year-on-year decline in net sales to 4,772 million yen for the quarter ending December 31, 2025, driven by aging smartphone titles in the Entertainment Business.

See it on page 1Operating losses narrowed significantly to 86 million yen from 730 million yen in the prior year, primarily due to a group-wide reduction in advertising and selling expenses.

See it on page 4Ordinary profit surged 752.4% to 484 million yen, heavily supported by 442 million yen in foreign exchange gains.

See it on page 7Profit attributable to owners of the parent rose 279.6% to 170 million yen, despite absorbing a 273 million yen extraordinary loss from a career transition support program.

See it on page 4The Entertainment Business remains the core revenue driver at 4,681 million yen, with 'DRAGON QUEST WALK' continuing to provide steady performance.

See it on page 4The company maintains a strong balance sheet with an equity ratio of 91.7% and total assets of 72,183 million yen.

See it on page 1Due to high market volatility, COLOPL has declined to provide a consolidated financial forecast for the full fiscal year ending September 30, 2026.

See it on page 1COLOPL, Inc. reported its consolidated financial results for the first quarter of the fiscal year ending September 30, 2026, covering the period from October 1, 2025, to December 31, 2025. The data reveals a period of transition characterized by declining top-line revenue but significantly improved bottom-line profitability compared to the previous year. Net sales fell 10.2% year-on-year to 4,772 million yen, primarily due to lower revenue in the Entertainment Business as several existing smartphone titles saw extended distribution periods.

Despite the revenue decline, the group narrowed its operating loss from 730 million yen in the prior year to 86 million yen. This improvement was driven by a group-wide cost review that successfully reduced advertising and selling expenses. Ordinary profit rose sharply by 752.4% to 484 million yen, bolstered by 442 million yen in foreign exchange gains. Profit attributable to owners of the parent increased 279.6% to 170 million yen, even after accounting for a 273 million yen extraordinary loss related to a career transition support program under its business restructuring initiative.

The Entertainment Business remains the primary segment, generating 4,681 million yen in sales, with "DRAGON QUEST WALK" continuing to provide steady contributions. The Investment and Development Business reported 90 million yen in sales and narrowed its segment loss through the sale of operational investment securities. Geographically focused on Japan and IT-related investments, the company maintains a strong financial position with an equity ratio of 91.7% and total assets of 72,183 million yen. Due to the rapid volatility of the entertainment market, the company has opted not to disclose a consolidated financial forecast for the full fiscal year.