Related Documents

Financial

Giant Network 2025 Annual Report: China

Giant Network’s 2025 annual report demonstrates a robust year‑over‑year performance, with total revenue escalating 72.7 % to ¥5.05 billion and net profit attributable to shareholders rising 23.1 % to ¥1.76 billion. Operating cash flow surged by 188.6 %, underscoring strong liquidity generation. The company’s dual‑core strategy—leveraging the MMORPG IP “征途” and the casual title “超自然行动组”—drives growth, supported by AI‑enabled development and cross‑platform expansion. Despite these gains, recent non‑recurring losses have yet to turn positive, creating some uncertainty about long‑term profitability. Regulatory developments in China have accelerated a focus on original IP and digital‑culture products. Government policies encourage embedding traditional culture into game design, boosting AI and cloud R&D, and expanding overseas digital content. Giant Network aligns with these directives through a research‑and‑operations model, heavy IP investment, and compliance tightening under new child‑online‑protection rules. Financially, operating profit rose 54 % to ¥829 million, while net profit increased 93 % to ¥947 million, largely due to higher investment income and lower tax expense. R&D spending more than doubled, reflecting intensified product development. Other comprehensive income swung from a positive ¥219 million to a negative ¥220 million, driven by fair‑value changes and credit impairment losses. The group maintained a conservative asset‑liability ratio, rising from 12.76 % to 18.67 %, and retained over 80 % voting control through founder‑controlled entities. Key findings highlight that core gaming revenue remains strong, investment income is mixed, and non‑recurring items significantly impact overall profitability. The report covers China exclusively, focusing on the 2025 fiscal year and encompassing gaming operations, IP development, regulatory compliance, and financial risk management.

Giant Network GroupApr 2026

Financial

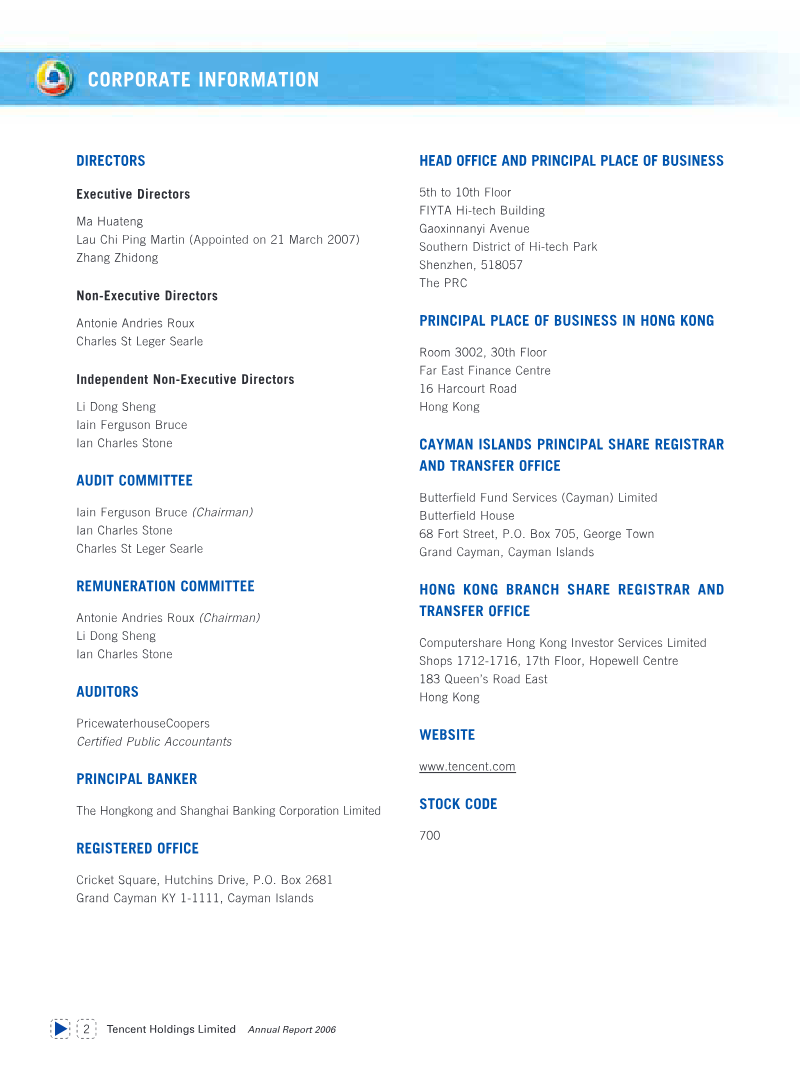

Tencent Holdings Limited Annual Report 2006

Tencent Holdings Limited’s 2006 annual report demonstrates a dramatic expansion of its internet‑based business, with total revenues rising 96.3 % to RMB 2,800 million and net profit increasing 119 % to RMB 1.06 billion. Growth is driven primarily by a 132 % increase in Internet value‑added services and a 136 % jump in online advertising, while mobile/telecom services also contributed significantly. Operating profit surged to RMB 1.16 billion, and the net margin improved from 34 % to 38 %. Cash and investments totaled RMB 3.22 billion, largely in U.S. dollar‑denominated assets that expose the group to Renminbi appreciation risk. The company’s financial health is reinforced by a strong balance sheet: total assets rose to RMB 1.77 billion, and the group maintained no interest‑bearing borrowings as of year‑end. Shareholder value initiatives included a final dividend of HKD 0.12 per share, the repurchase and cancellation of 18.4 million shares during 2006, and a cumulative share buyback of over 32 million shares since its IPO. Governance structures feature a board with executive, non‑executive and independent directors, audit and remuneration committees, and compliance with Hong Kong listing rules. Key executives hold significant share positions through BVI entities, while Naspers‑controlled MIH QQ holds 35.6 % of issued shares. Geographically, operations are concentrated in mainland China (≈70 % of segment assets), with subsidiaries and customers spread across Asia, Africa, and the Mediterranean under Naspers’ umbrella. The report covers fiscal year 2006, detailing revenue streams from internet services, mobile telecoms, and online advertising, and outlines accounting policies such as IAS 39 adoption, fair‑value measurement for available‑for‑sale securities, and share‑based compensation recognition. Overall, Tencent’s 2006 performance reflects rapid scaling of core digital services, robust profitability, and a commitment to shareholder returns within a growing but still low‑penetration Chinese internet market.

Tencent

Financial

2011 Annual Report

Tencent Holdings’ 2011 financial year was marked by a sharp expansion of its core internet platform, with consolidated revenues rising 45 % to RMB 28.5 billion and operating profit increasing 24.6 % to RMB 12.3 billion. The growth was driven primarily by internet value‑added services (IVAS) and mobile telecommunications services, which together accounted for 80 % of sales. Online gaming revenue surged 66 %, propelled by flagship titles such as *Cross Fire* and *League of Legends*, while social networking platforms—QQ.com, Qzone, Pengyou and Tencent Microblog—expanded user bases to 373 million registered users and 68 million daily active users. Total assets doubled from RMB 35.8 billion to RMB 56.8 billion, largely due to a jump in current assets and non‑current investments, including significant equity stakes in eLong, Kingsoft and other associates. Capital expenditures more than doubled to RMB 4.16 billion, reflecting investment in infrastructure and acquisitions such as Riot Games and Gamegoo, which generated goodwill of RMB 3.8 billion. Net profit attributable to equity holders rose 26.7 % to RMB 10.2 billion, with earnings per share reaching RMB 5.61 basic. Governance remained robust: the board met quarterly, retained a majority of non‑executive directors and three independent members, and maintained COSO‑based internal controls with no material deficiencies. Share‑based compensation expanded markedly—over 7 million options exercised and a share award pool of nearly 16 million shares outstanding—while dividend policy remained conservative with a final dividend of HKD 0.75 per share. Geographically, operations were concentrated in China through subsidiaries such as Tencent Computer and Tencent Technology, with the group’s legal domicile in the Cayman Islands and listing on Hong Kong. The period covered 2011, with a focus on internet services, mobile telecommunications, online gaming and advertising within the Chinese market.

Tencent Holdings Limited

Financial

Annual Results Announcement: 2025

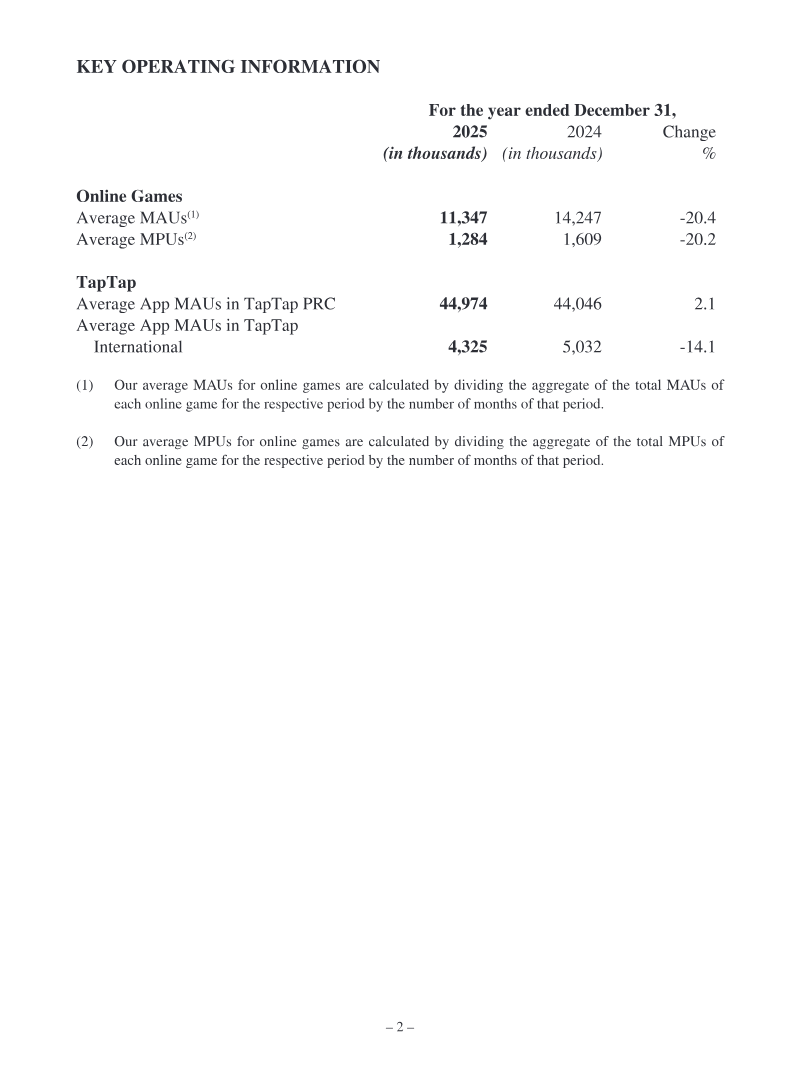

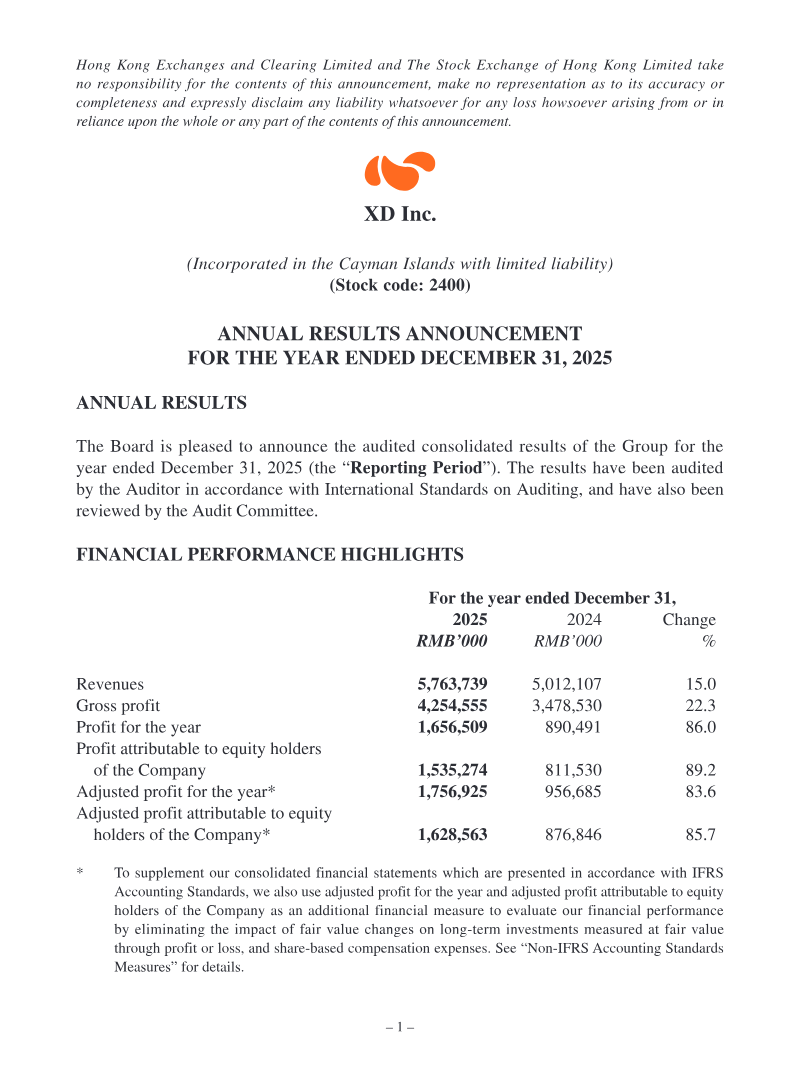

XD Inc. achieved substantial financial growth throughout the 2025 fiscal year, characterized by a 15% increase in total revenue to RMB 5.76 billion and a significant surge in profit attributable to equity holders, which reached RMB 1.54 billion. This performance was underpinned by a 10.5% rise in gaming revenue, bolstered by the success of titles such as Heartopia and Torchlight: Infinite, alongside a 24.7% revenue increase within the TapTap platform. The company’s financial health was further strengthened by an improved gross margin of 73.8% and a robust cash position of RMB 3.77 billion, supported by a strategic reduction in the cost of revenues and a lower gearing ratio of 22.5%. The company’s strategic focus remains centered on cross-platform expansion and the integration of AI-driven development tools to secure long-term competitiveness. While financial metrics showed marked improvement, the company observed a decline in online game user metrics, specifically monthly active users and monthly paying users. To address these shifts, management has prioritized capital optimization through active share repurchases and the maintenance of employee incentive programs. Notably, the board opted against a final dividend for 2025, citing a commitment to capital reinvestment and a need to address corporate governance concerns regarding the consolidation of the chairman and CEO roles. These results reflect a period of operational consolidation and international market penetration for the China-based firm. The financial figures, which have been reviewed by the Audit Committee and aligned with the group’s consolidated statements, demonstrate a transition toward higher profitability and operational efficiency. By leveraging the acquisition of the Torchlight intellectual property and refining advertising algorithms on the TapTap platform, the company aims to sustain its growth trajectory despite the challenges posed by fluctuating user engagement metrics in the broader gaming sector.

XD