Related Documents

Report

UnitedHealth Group: First Quarter 2025 Results and Revised Guidance

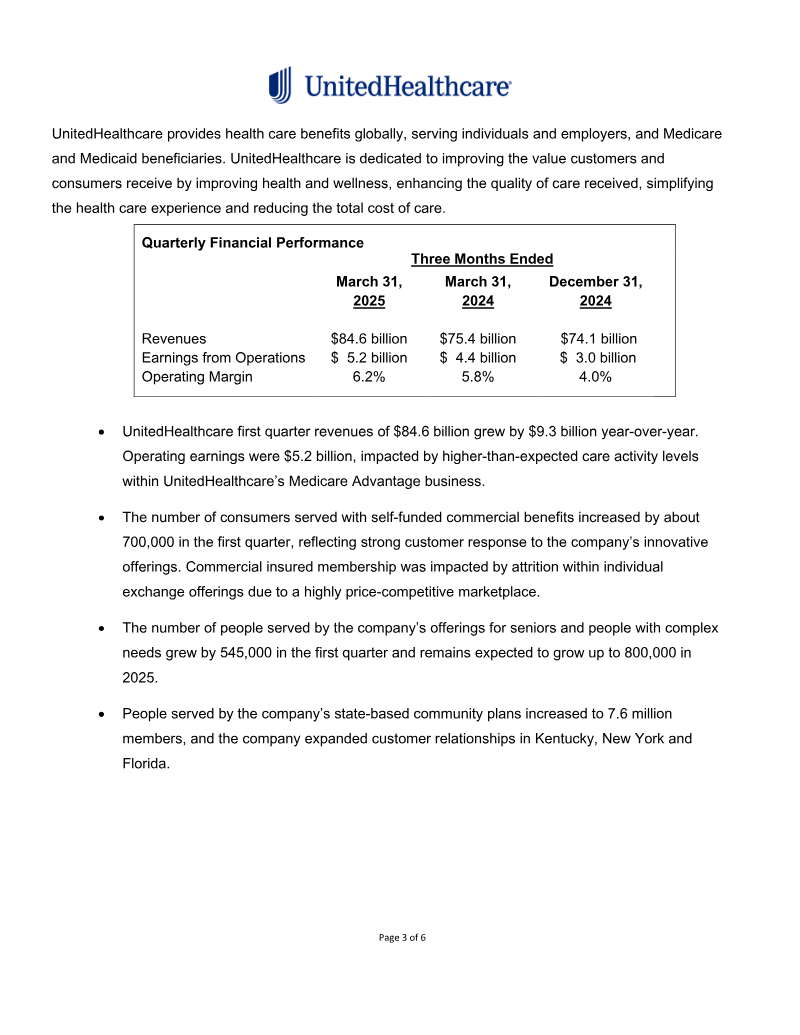

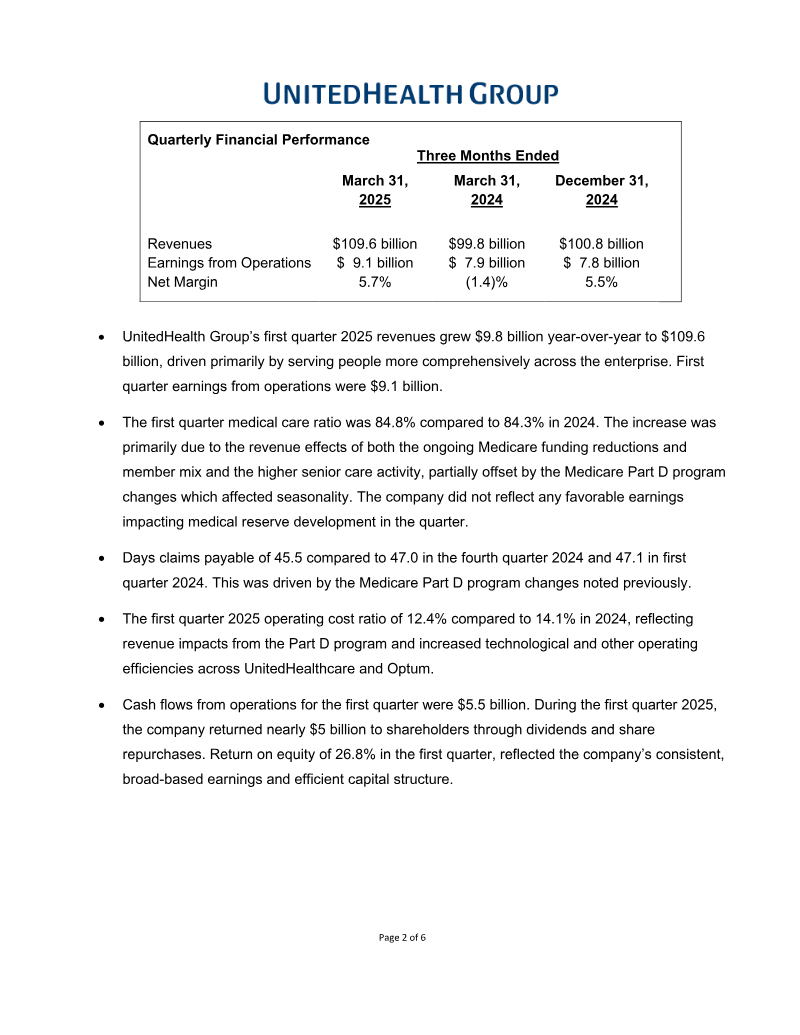

alth Group Reports First Quarter 20a UnitedHealth Group Reports First Quarter 2025 Results and Revises Full Year Guidance • Revised 2025 Earnings Outlook to $24.65 to $25.15 Per Share, Adjusted Earnings • First Quarter Earnings were $6.85 Per Share, Adjusted Earnings $7.20 Per Share • Revenues of $109.6 Billion Grew $9.8 Billion Year-Over-Year • Consumers Served by UnitedHealthcare Increased by 780,000 Year to Date • Optum Health Continues to Expect to Serve 650,000 New Value...

UnitedHealth Group

Report

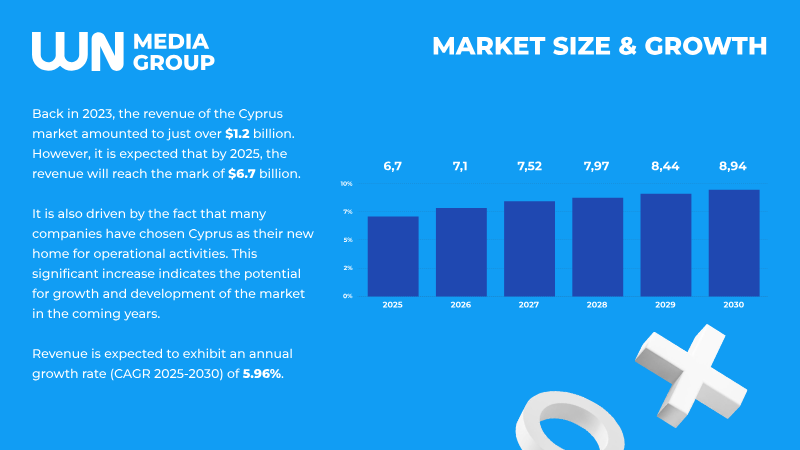

Video Games Ecosystem Report: Cyprus 2025

The report outlines a rapidly expanding video‑games ecosystem in Cyprus, projecting market revenue to surge from $1.2 billion in 2023 to $6.7 billion by 2025, with a compound annual growth rate of 5.96 % through 2030. The growth is driven by a growing number of tech firms relocating to the island, with 282 startups reported in July 2025—39 funded, 15 in Series A rounds, and one unicorn. Over 600 companies of varying sizes now operate locally, benefiting from Cyprus’s favorable tax regime, EU membership, and supportive regulatory framework. Key success stories highlight local studios such as MY.GAMES and Ludus, whose mobile titles have achieved multi‑million downloads and cross‑platform revenue streams exceeding $2 million. The mobile segment dominates, with Playrix, Easybrain, and Outfit7 leading in casual and puzzle games; yet PC and console titles from Wargaming and Digital Vortex Entertainment demonstrate a growing presence in the market. Cross‑platform development and cloud gaming are emerging trends, offering opportunities for developers skilled across mobile and PC. The island’s advantages include competitive corporate tax rates, strategic positioning between Europe and the Middle East, a growing talent pool enriched by relocation of experienced developers, and increasing investment in esports and blockchain gaming. The report also promotes the WN Conference Cyprus (September 2025) as a networking and market‑entry platform, anticipating attendance of 700+ participants. Overall, the data portray Cyprus as an attractive hub for game development and investment, poised for continued expansion through 2030.

InvestGameMar 2026

Report

Vietnam Innovation and Private Capital Report: 2025

Vietnam’s 2025 Innovation and Private Capital Report positions the country as a rapidly ascending tech‑investment hub in Southeast Asia, underpinned by steady macro growth and decisive policy support. A 6 % annual real GDP expansion, a $36 B digital economy, and the landmark Resolution No. 57‑NQ/TW collectively create a macro‑environment that attracts both domestic and foreign capital. Private‑capital activity in 2024 totaled $2.3 B across 141 deals, with buyouts dominating but early‑stage venture capital rebounding sharply in the second half of the year. High‑tech sectors—particularly AI, AgriTech, Green Tech, semiconductors, and data centers—experienced multi‑fold funding surges, reflecting a shift toward technology‑driven value creation. The labor market fuels consumer and industrial demand: Vietnam ranks second in Southeast Asia for workforce size, with a growing middle‑affluent class projected to exceed 45 % of the population by 2030. Strong education outcomes and a youthful, tech‑savvy demographic drive growth in retail, e‑commerce, digital health, and edtech. Tier‑2 cities such as Bac Ninh, Can Tho, and Da Nang emerge as new growth poles, supported by government investment in transportation, renewable energy, and digital infrastructure. Resolution No. 57 sets ambitious 2030–2045 targets—30–50 % GDP share from digital and high‑tech exports, 80 % cashless transactions, and 2 % of GDP allocated to R&D (60 % private). It outlines strategic actions in AI, 6G, talent development, and digital governance to attract at least five global tech giants for R&D and manufacturing. Projected economic gains from AI alone could reach $120 B by 2040, while renewable energy and climate‑tech investments are already reshaping the power sector through flexible PPAs and green‑credit programs. Overall, Vietnam’s coordinated policy framework, expanding talent pool, and maturing private‑capital ecosystem converge to make the country a compelling destination for long‑term value creation across high‑growth technology, green infrastructure, and consumer markets within Southeast Asia.

Boston Consulting GroupFeb 2026

Financial

1Q FY Sep. 2026 Financial Results Presentation

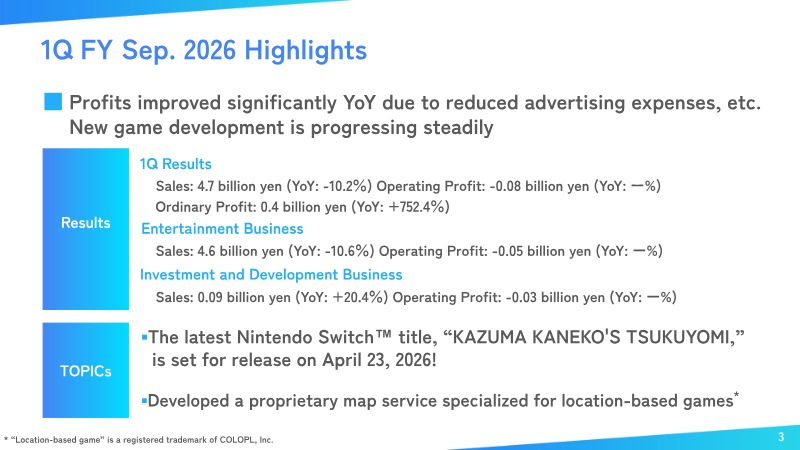

COLOPL’s financial performance for the first quarter of the fiscal year ending September 2026 reflects a strategic pivot toward profitability through rigorous cost management despite a shrinking core user base. While net sales declined 10.2% year-on-year to 4.7 billion yen, the company successfully reversed previous losses to achieve an ordinary profit of 0.4 billion yen. This recovery was primarily facilitated by aggressive reductions in advertising expenditures. The company maintains a highly stable financial foundation, characterized by a 91.7% equity ratio, providing the necessary capital to fund its transition from a mobile-centric developer to a multi-platform entertainment entity. Operational data indicates significant headwinds in the mobile segment, with Quarterly Active Users dropping to 400,000 from a peak of 575,000 in 2022. This contraction is compounded by a long-term decline in Average Revenue Per User, which has fallen from 862 JPY to 680 JPY over the same period. To counter these trends, the growth strategy emphasizes expansion into the PC and console markets, highlighted by the upcoming April 2026 release of Kazuma Kaneko’s Tsukuyomi for the Nintendo Switch. Furthermore, investments in specialized game server services and location-based map distribution technologies aim to diversify revenue streams beyond traditional mobile gaming. The long-term vision targets a "Global Top 20" market position with ambitious goals of 100 billion yen in sales and 50 billion yen in operating profit. Achieving these benchmarks relies on integrating cutting-edge technology, including AI-powered titles and XR experiences for next-generation mobility. By leveraging strategic investments in firms like CORE, Inc. and focusing on high-value intellectual property, the objective is to stabilize the current user contraction while building a sustainable pipeline of cross-platform content that can compete on a global scale.

COLOPLFeb 2026